Tribunal deletes addition after finding no evidence supporting alleged machinery rental income claim.

Meetu Kumari | Jun 23, 2026 |

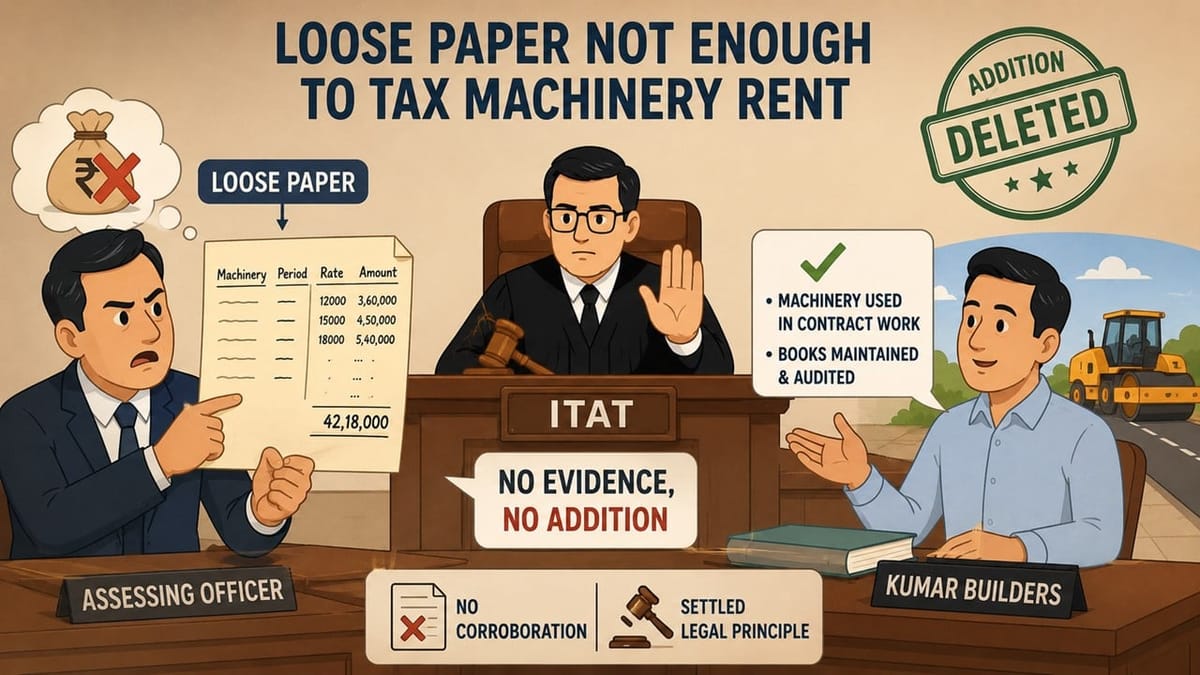

ITAT: Loose Paper Not Enough to Tax Alleged Machinery Rent Without Supporting Evidence

Kumar Builders, a partnership firm engaged in road construction and maintenance contracts, filed its return for AY 2021-22 declaring income of Rs.62.92 lakh. Following a search and survey action conducted in the Triconnect Group cases, the assessment was reopened under Section 147.

During the proceedings, the Assessing Officer relied on a loose paper found during the search containing details of machinery, periods, rates and amounts. The department treated these entries as rental income allegedly earned by the assessee from hiring out machinery and made an addition of Rs 42.18 lakh under the head “Income from Other Sources”.

The assessee explained that the document was merely an internal worksheet prepared by its accountant to monitor machinery utilisation and estimate operating costs for contract work. It contended that no machinery had been given on rent and no such income had been received.

The Tribunal observed that the assessee maintained regular audited books of account which had neither been rejected nor found defective. The machinery reflected in the loose paper was already recorded in the books and was being used in execution of contract works generating turnover of about Rs.11.94 crore during the year.

The Bench noted that the Assessing Officer had not identified any person to whom the machinery was allegedly hired, nor produced any evidence showing actual receipt of rent. The loose sheet itself did not establish receipt of money or disclose the identity of any payer.

According to the Tribunal, the addition was based entirely on assumptions drawn from uncorroborated notings on a loose paper. It reiterated the settled legal principle that loose papers, without supporting evidence, cannot by themselves constitute reliable evidence for making additions under the Income-tax Act.

Relying on judicial precedents, including the Bombay High Court’s ruling in CIT v. Supreme Industries Ltd., the Tribunal held that entries in seized documents cannot be relied upon unless supported by independent evidence demonstrating that the alleged transactions actually took place.

The ITAT held that in the absence of any corroborative material, proof of actual receipt of rent, or identification of any hirer, there was no basis for treating the figures noted on the loose paper as taxable income. Consequently, the addition of Rs.42.18 lakh was deleted and the assessee’s appeal was allowed.

To Read Full Order, Download PDF Given Below

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"