Meetu Kumari | Jun 24, 2026 |

HC Upholds GST Demand Based on Seigniorage Fee Data, Allows Assessee to Pursue Statutory Appeal

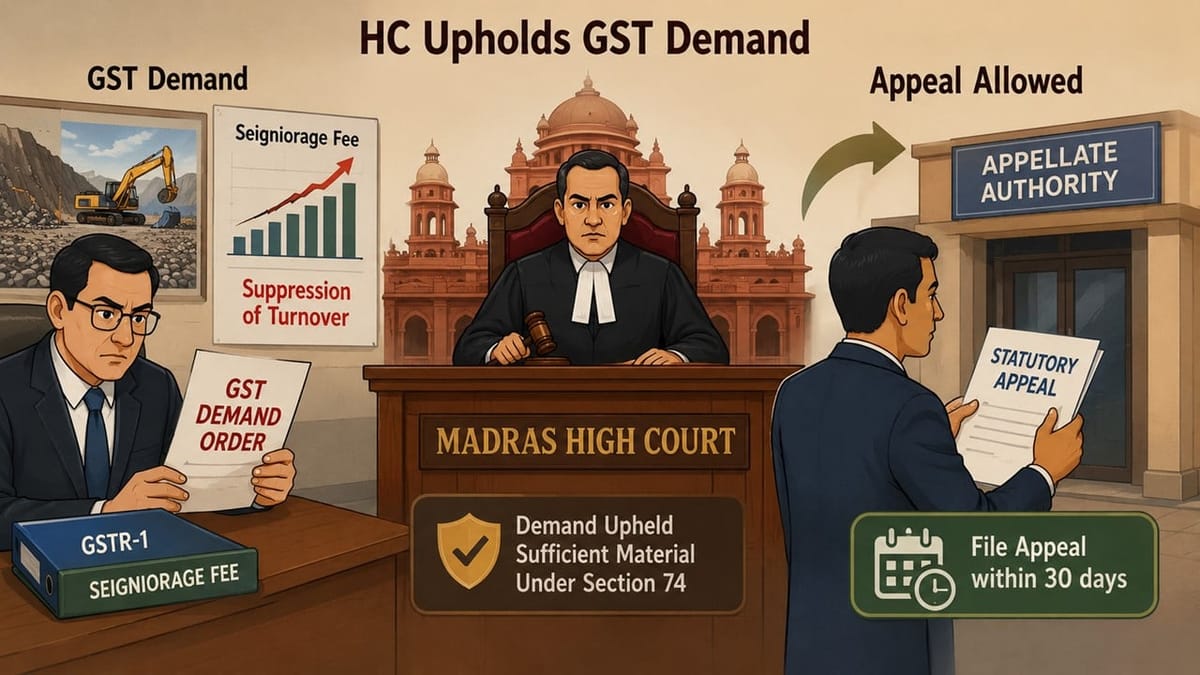

The Madras High Court dismissed writ petitions filed by KPR Enterprises challenging GST demand orders for AYs 2018-19, 2019-20 and 2020-21, holding that the tax department had sufficient material to invoke the extended limitation period under Section 74 of the GST Acts on allegations of suppression of turnover.

The dispute arose after the department conducted an inspection and issued notices in Forms GST DRC-01A and DRC-01 alleging that the petitioner had under-reported the value of outward supplies. The department compared the seigniorage fee paid by the petitioner for quarrying operations with the turnover disclosed in GSTR-1 returns and concluded that there was substantial suppression of taxable supplies. Based on this analysis, demands were confirmed through orders dated 15.07.2024.

The petitioner contended that no incriminating material had been unearthed during inspection and that the findings relating to fraud, wilful misstatement and suppression were unsupported. It was further argued that the petitioner merely sold rock boulders and that the contractor extracting and selling the minerals had already discharged the tax liability, resulting in no loss to the revenue. The petitioner also alleged violation of natural justice on the ground that no proper opportunity of hearing was granted.

Rejecting these contentions, Justice C. Saravanan noted that the department had estimated escaped turnover using the National Standard Method after examining the seigniorage fees paid and the quantity of minerals extracted. The Court observed that it was highly improbable for the petitioner to have paid substantial seigniorage fees while reporting significantly lower outward supplies in GST returns. The material available on record prima facie established suppression of turnover and justified invocation of Section 74.

The Court held that both Sections 73 and 74 operate where it “appears” that tax has escaped assessment and, in the present case, the department possessed adequate foundational facts to initiate proceedings under Section 74. It also found no procedural irregularity in the adjudication process warranting interference under Article 226.

Consequently, the writ petitions were dismissed. However, the Court granted liberty to the petitioner to file statutory appeals within 30 days and directed that, if such appeals are filed within that period, the appellate authority should entertain them on merits without raising limitation objections and after providing an opportunity of hearing.

To Read Full Judgment, Download PDF Given Below

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"