Studycafe | Jan 8, 2016 |

Comparison of IFRS, Indian GAAP and IND AS -Simplified

“Ind-AS refers to converged standards notified by NACAS. In all 35 standards has been notified till date, however, the implementation date is yet to be notified. Alternatively you may describe Ind-AS in an mathematical equation; Ind- AS = IFRS as issued by IASB Less carve outs Add IFRS pronouncement being adopted in Ind-AS”

Introduction:

The term IFRS refers to International Financial Reporting Standards issued by International Accounting Standards Board (IASB). There are many jurisdictions which have adopted IFRS with very few modifications and thus described accordingly e.g. IFRS as adopted by EU, IFRS as adopted by Australia. However, in international parlance, the term IFRS refers to pronouncements issued by International Accounting Standards Board (IASB).

Until Ind-AS is mandatory, the present framework of Accounting Standards, Interpretations, Guidance notes and various Industry practices are collectively referred as Indian GAAP.

Ind-AS refers to converged standards notified by NACAS. In all 35 standards has been notified till date, however, the implementation date is yet to be notified. Alternatively you may describe Ind-AS in an mathematical equation; Ind- AS = IFRS as issued by IASB Less carve outs Add IFRS pronouncement being adopted in Ind-AS

This article intends to cover in a simplified way:

1.) High level more common differences between IFRS and Indian GAAP

2.) High level carve outs between IFRS and Ind-AS with commentary

3.) Summarizing /analysing accounting adjustments from Indian GAAP to IFRS from published financial statements of Indian Companies

4.) Commenting where are we in terms of convergence

5.) Description of common online implementation tools

1. High level more common differences between IFRS and Indian GAAP:

a) Property, plant and equipment (PPE):

i) Measurement

IFRS- PPE are measured at an amount paid or fair value of other consideration given to acquire an asset at the time of acquisition or construction.

Indian GAAP – Similar to IFRS except in certain cases where there is no specific guidance available. Such situations are accounting of site restoration obligations, asset acquired on deferred term basis, etc.

ii) Component accounting:

IFRS – requires component accounting of fixed assets where each major part of item of property, plant and equipment is depreciated separately. This depreciation is allocated on systematic basis over its useful life, reflecting the pattern in which entity consumes the assets benefits.

Indian GAAP – No specific concept of component accounting and in practice, entire asset is depreciated at a flat rate of depreciation based on the useful life determined by the Management and in many cases based on rates given in Schedule XIV of the Companies Act, 1956 which provide minimum rate of depreciation for companies.

iii) Changes in method of depreciation and estimation of useful life

IFRS- change in method of depreciation and estimation of useful life of assets are treated as changes in estimation and accounted prospectively in the financial statement.

Indian GAAP – Change in method of depreciation is accounted by retrospectively computing depreciation under new method and impact is recorded in the period of change i.e. it is treated as change in accounting policy. Accounting of changes in estimation of useful life is similar to IFRS i.e. prospectively.

b) Business combination:

i) Guidance on accounting for business combination

IFRS – provides extensive guidance on accounting for business combination and requires looking beyond the legal form of the transaction. All business combinations, within the standards, are considered as acquisitions and accounted using the purchase method.

Indian GAAP – there is no comprehensive accounting standard and the accounting is driven by legal form and often the court order in case of merger. Business combinations can be accounted using the pooling-of-interests method, if it meets certain criteria (the most common method seen in practice) or the purchase method.

ii) Contingent consideration

IFRS- contingent consideration which depends upon future event, such as achieving certain sales target, profit levels, etc. is required estimated and is included as a part of the acquisition cost if it is probable and is recognised initially at fair value as either financial liability or equity.

Indian GAAP – contingent consideration is considered at the date of acquisition if the payment is probable and a reasonable estimate of amount can be made.

iii) Acquisition date

IFRS- Acquisition date would be the date on which the acquirer effectively obtains control of the acquiree.

Indian GAAP – Acquisition date has not been specifically defined. In case of amalgamation or acquisition of business, it is the date prescribed in the court scheme (a practice widely seen is April 1, of earlier financial year).

c) Financial instruments:

i) Guidance on identification, classification, recognition and measurement

IFRS – provides extensive guidance on identification, classification, recognition and measurement of financial instruments. Under IFRS financial assets are classified in four categories: a) Financial asset at fair value through profit or loss b) Held to maturity c) Loans and receivables and d) Available for sale financial assets. Financial liabilities are classified in two categories those that are recognised at fair value through profit or loss (includes trading), and all others.

Indian GAAP – there is no comprehensive guidance on accounting of financial instrument. However, ICAI has approved standards on financial instruments similar to IFRS from April 1, 2011 which are recommendatory in nature.

ii) Basis of classification:

IFRS – classification of financial instrument as financial liability or equity would depend mainly upon substance of the contractual agreement

Indian GAAP – classification is based on the form rather than substance of the agreement. For e.g. under Indian GAAP preference share capital is consider as equity which may not hold true under IFRS where it may be treated as financial liability or equity depending upon the contractual arrangement. Further, under IFRS, if an instrument has both a liability component and an equity component, the issuer is required to separately account for each component. Under Indian GAAP there is no specific guidance but accounting follows the form rather than substance.

iii) Repurchase of own share

IFRS- if an entity repurchase its own shares, such shares are considered as treasury share and are shown as deduction from shareholders equity.

Indian GAAP – there is no specific standard for accounting of such transactions under Indian GAAP. When the share is repurchased they are cancelled and cannot be kept as treasury stock.

d) Foreign currency translation:

i) Functional currency and presentation currency

IFRS – All the entities are required to identify and determine its functional currency and presentation currency. Selection of functional currency has a direct impact on the treatment of exchange gains on the financial results of the entity.

Indian GAAP – does not have the concept of functional currency and presentation currency. It assumes an entitys reporting currency would be the currency in which it is domiciled.

ii) Accounting of exchange gains and losses arising from translation

IFRS- exchange gains and losses arising from translation of all monetary assets or liability are recognized immediately in profit and loss account except to the extent meets the definition of borrowing cost.

Indian GAAP – if the long term foreign currency item relates to other than an acquisition of depreciable capital assets, entity has an option to accumulate such difference Foreign currency monetary reserve and if the long term foreign currency item relates to acquisition of depreciable capital assets, exchange difference can be added or deducted from such capital asset.

e) Share based payment transactions:

i) Recognition:

IFRS – requires an entity to recognise share-based payment transactions in its financial statements, including transactions with employees or other parties to be settled in cash, other assets or equity instruments of the entity. Fair value method is required in almost all circumstances.

Indian GAAP- there is no specific standard which explain the accounting of share based payment transaction. Mostly accounting is done based on guidance note issued by ICAI and SEBI guidelines for listed entities which is applicable to employees. Intrinsic value method is widely applied practice and considering the nature of ESOP scheme, in most cases, it does not result in any charge in the statement of profit & loss account.

ii) Stock options issued by foreign parent company:

IFRS- stock options issued by parent company to the employee of the subsidiary needs to assess in the books of subsidiary i.e. whether it would be equity settled or cash settled share based payment transactions.

Indian GAAP most of the equity settled arrangements (not routed through subsidiaries) are yet to be brought in specific framework of accounting.

f) Segment reporting:

i) Identification of segment:

IFRS- operating segments are identified based on the financial information that is evaluated regularly by the Chief Operating Decision Maker (CODM) in deciding how to allocate resources and in assessing performance.

Indian GAAP- entity has to identify two sets of segments (business and geographical), using a risks and rewards approach.

ii) Aggregation of segments:

IFRS- Two or more operating segments may be aggregated into a single operating segment if aggregation is consistent with the core principle of IFRS.

Indian GAAP- there is no specific guidance in this regard.

iii) Revenue from external customer/foreign countries

IFRS – requires disclosures of revenues from external customers for each product and service. With regard to geographical information, it requires the disclosure of revenues from customers in the country of domicile and in all foreign countries, non-current assets in the country of domicile and all foreign countries.

Indian GAAP- disclosures are based upon the classification of primary or secondary segment. Primary segment disclosures are much elaborate in comparison to secondary segment disclosures.

g) Related party disclosure:

i) Coverage of related party

IFRS- related party covers close members of the family of an individual referred to as key management personnel or a party who exercise control or significant influence.

Indian GAAP- covers only relatives of key management personnel.

ii) Coverage of Post-employee benefit

IFRS- Post-employment benefit plan for the benefit of employees of the entity, or of any entity that is a related party of the entity is a related party under IFRS

Indian GAAP – does not specifically identify employee benefit trusts as related parties.

iii) Coverage under Key Management Personnel

IFRS- covers executive as well as non-executive directors in the definition of Key Management personnel (KMP). Also, it covers Key Management Personnel (KMP) of the entity as well as its parent.

Indian GAAP- the term Key Management Personnel as defined under AS 18, does not include nonexecutive directors, unless they have the authority and responsibility for planning, directing and controlling the activities of the reporting enterprise.

h) Consolidated financial statements:

i) Special Purpose Entities (SPE)

IFRS- SPE should be consolidated when the substance of the relationship between entity and SPE indicates that the SPE is controlled by that entity.

Indian GAAP – no specific guidance

ii) Presentation of non-controlling/minority interest

IFRS – non-controlling interests are presented as component of equity

Indian GAAP- minority interests represented separately from liabilities and equity.

iii) Allocation of losses by subsidiary

IFRS- losses incurred by subsidiary have to be allocated to non-controlling interests, even if this results in deficit balance of non-controlling interest.

Indian GAAP- losses exceeding minority interest in the equity of the subsidiary have to be adjusted the minority interest, except to the extent that the minority interest has a binding obligation to, and are able to make good the losses.

iv) Interest in Joint Venture:

IFRS- interest in joint venture is accounted either by using proportionate consolidation method or equity method.

Indian GAAP- only allows proportionate consolidation method.

2. High level carve outs between IFRS and Ind-AS with commentary

IND-AS has been notified with few carve outs from IFRS. Broadly, these can be categorised as IFRS deferred by MCA, Carve outs- Unavoidable (some of these are for specific industry) and Carve outs Avoidable.

Comparison of IFRS, Indian GAAP and IND AS -Simplified

Carve Out-UnavoidableInd AS 21, The Effects of Changesin Foreign Exchange Rates:

Background:

IAS 21 requires recognition of exchangedifferences arising on translation of monetary items from foreign currency tofunctional currency directly in profit or loss.

Carve out:

Ind AS 21 permits an option to recogniseexchange differences arising on translation of certain long-term monetary itemsfrom foreign currency to functional currency directly in equity. In thissituation, Ind AS 21 requires the accumulated exchange differences to beamortised to profit or loss in an appropriate manner. IAS 21 does notpermit such a treatment.

Our Comment:

Welcome move from India Inc. Reduces volatility in Statement of Net Income. Moreover if acompany wants to prepare IFRS it can easily identify the adjustment.

Ind AS 28, Investment inAssociates:

Background:

1.) IAS 28 requires that difference between the reporting period of an associate and that of the investor should not be more than three months, in any case.

2.) IAS 28 requires that for the purpose of applying equity method of accounting in the preparation of investors financial statements, uniform accounting policies should beused. In other words, if the associates accounting policies are different fromthose of the investor, the investor should change the financial statements ofthe associate by using same accounting policies.

Carve out:

1.) The phrase unless it isimpracticable has been added in the relevant requirement i.e., paragraph25 of Ind AS 28.

2.) The phrase, unless impracticable to do so has been added in the relevant requirements i.e., paragraph 26 of Ind AS 28.

Comment:

Point 1 Not material as anyway adjustments for periods gap is made.

Point 2 In few cases, there would not beconsolidation of associate under Ind-AS

Ind AS 32, Financial Instruments:Presentation:

Background:

Introduction of exception to thedefinition of financial liability with respect to the treatment of equityconversion option in case of foreign currency bond. IAS 32 does not containsuch exception.

Carve out:

An exception has been included to thedefinition of financial liability in paragraph 11 (b) (ii), Ind AS 32 toconsider the equity conversion option embedded in a convertible bonddenominated in foreign currency to acquire a fixed number of entitys ownequity instruments as an equity instrument if the exercise price is fixed inany currency. This exception is not provided in IAS 32.

Comment:

Welcome Move. Has a strong rationale forcarve out. This situation is widely applicable e.g. FCCBs.

Ind AS 39, Financial Instruments:Recognition and Measurement:

Background:

As per IFRS – IAS 39 requires all changesin fair values in case of financial liabilities designated at fair valuethrough Profit and Loss at initial recognition shall be recognised in profit orloss. IFRS 9 which will replace IAS 39requires these to be recognised in other comprehensive income

Carve out:

A proviso has been added to paragraph 48of Ind AS 39 that in determining the fair value of the financial liabilitieswhich upon initial recognition are designated at fair value through profit orloss, any change in fair value consequent to changes in the entitys own creditrisk shall be ignored.

Comment:

Has a strong rationale. Quite anumber of advanced countries have adopted this provision.

Ind AS 103, Business Combinations:

Background:

As per IFRS – IFRS 3 requires bargainpurchase gain arising on business combination to be recognised in profit orloss.

Carve out:

Ind AS 103 requires the same to berecognised in other comprehensive income and accumulated in equity as capitalreserve, unless there is no clear evidence for the underlying reason forclassification of the business combination as a bargain purchase, in whichcase, it shall be recognised directly in equity as capital reserve.

Impact:

Situation generally applicable in very limitedcircumstances.

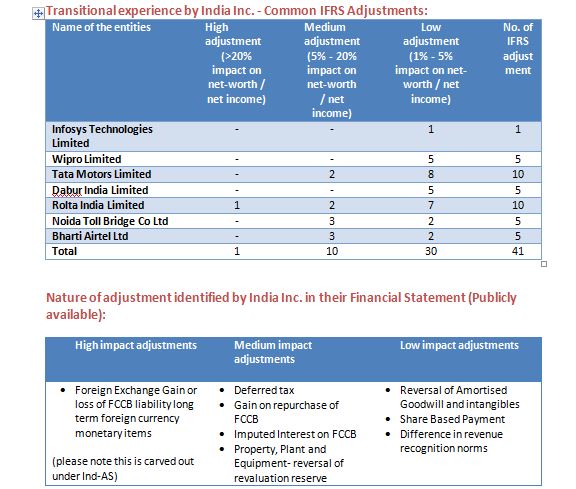

“On conversion of financial statementfrom Indian GAAP to IFRS, typically there is a tendency the see the Nature andQuantum of adjustments using some materiality threshold and classify theseadjustment into High Impact, Medium Impact and Low Impact on Networth &/orNet Income. The experience shows there are few adjustments of which the impactis very high.”

3.) Summarizing /analysing accounting adjustments from Indian GAAP to IFRS from published financial statements of Indian Companies

Thereare number of India Incs who have adopted the IFRS largely to comply withlisting requirement of foreign jurisdiction where they are listed. Based ontheir financial statement filed with relevant regulatory authorities in thatcountry, we have noted that on conversion of financial statement from IndianGAAP to IFRS, typically there is a tendency the see the Nature and Quantum ofadjustments using some materiality threshold and classify these adjustment intoHigh Impact, Medium Impact and Low Impact on Networth &/or Net Income. Theexperience shows there are few adjustments of which the impact is very high andthe same is analysed below;

4. Where are we today

Since NACAS issued 35 standards, IASB has issued further standards. ICAI has issued exposure draft/ standards on most of new pronouncement issues by IASB. However, all these are yet to be notified by NACAS.

With introduction of revised schedule VI, the look and feel of the financial statements resembles to those prepared under IFRS.

The road-map for Ind-AS is yet to be notified and we continue to believe it will be notified.

5. Online Implementation Tools

Various online tools can be downloaded, free of cost, from website of various prominent accounting firms. These include;

a. Model Financial Statements

b. IFRS measurement Checklist

c. IFRS disclosure Checklist

d. Comparison between Local GAAP and IFRS

e. Publications focusing on few standards/industries

Additionally, most of the firms, allows you to subscribe to their accounting library/ online research material for a price.

(The author is a member of the Institute. He can be reached at [email protected])

Disclaimer: The views and opinions expressed or implied in this Article are of the Authors personal views and opinions.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"