All about GST ITC Reversal on Account of Rule 37A:

The Input Tax Credit (ITC) reversal is necessary in a variety of situations, including the acquisition of goods and services for non-business purposes, blocked ITC, and so on.

Reversal of ITC

Table of Contents

All about GST ITC Reversal on Account of Rule 37A

The Input Tax Credit (ITC) reversal is necessary in a variety of situations, including the acquisition of goods and services for non-business purposes, blocked ITC, and so on.

In the case of ITC reversal, the credit for previously used input is added to the output tax liability to invalidate the ITC claimed previously.

To Download in PPT Form - Click Here

To Download in PPT Form - Click Here

Rule 37A of CGST Rules, 2017

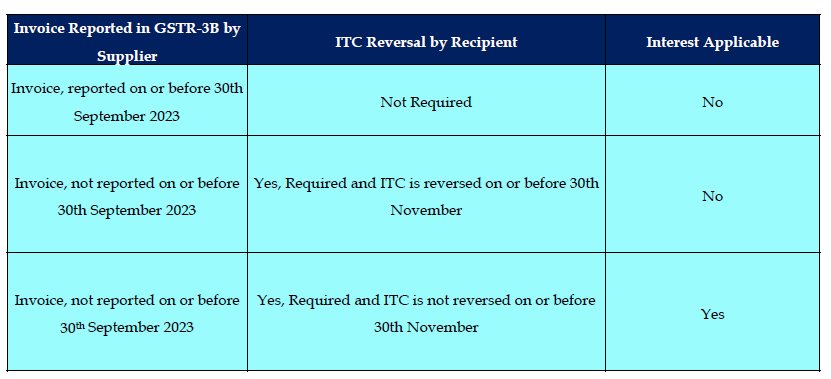

Vide Rule 37A of CGST Rules, 2017 the taxpayers have to reverse the Input Tax Credit (ITC) availed on such invoice or debit note, the details of which have been furnished by their supplier in their GSTR-1/IFF but the return in FORM GSTR-3B for the said period has not been furnished by their supplier till the 30th day of September following the end of financial year in which the Input Tax Credit in respect of such invoice or debit note had been availed. The said amount of ITC is required to be reversed by such taxpayers, while furnishing a return in FORM GSTR-3B on or before the 30th day of November following the end of such financial year, as part of this legal obligation.Facility to Tax-Payers

Currently GSTN provides no facility to check if tax has been paid by supplier on invoice or debit note reflecting in GSTR-2B for which ITC has been claimed. To facilitate the taxpayers, such amount of ITC required to be reversed on account of Rule 37A of CGST Rules for the financial year 2022-23 has been computed from system and has been communicated to the concerned recipient. The email communication to this effect has been sent on the registered email id of the taxpayer. The taxpayers are advised to take note of it and to ensure that such ITC, if availed by them, is reversed as per rule 37A of CGST Rules before 30th of November, 2023 in Table 4(B)(2) of GSTR-3B while filing the concerned GSTR-3B.Failure To Comply with Rule 37A of GST

Where the said amount of ITC is not reversed by the registered person in a return in FORM GSTR-3B on or before the 30th day of November following the end of such financial year during which such input tax credit has been availed, such amount shall be payable by the said person along with interest @ 24% thereon under section 50.Re-Claiming ITC Reversed

Where the supplier subsequently furnishes the return in FORM GSTR-3B for the said tax period, the said registered person may re-avail the amount of such credit in the return in FORM GSTR-3B for a tax period thereafter.

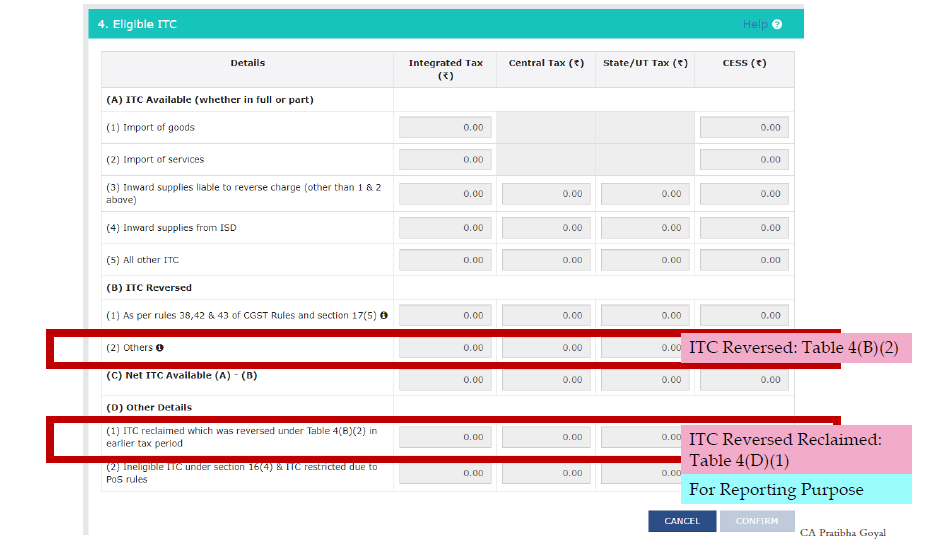

- The recipient in case of ITC reversal are required to ensure that such ITC, if availed by them, is reversed as per rule 37A of CGST Rules in Table 4(B)(2) of GSTR-3B while filing the concerned GSTR-3B.

- The recipient can re-claim or re-avail the ITC in Table 4(D)(1) of Form GSTR-3B of any subsequent return periods. Note that such re-claims are allowed despite the restriction put under Section 16(4) of the CGST Act.

To Download in PPT Form - Click HereAbout Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts