Alternatives to Traditional Methods of Re-Insurance

Alternatives to Traditional Methods of Re-Insurance As you know an insurance is a means of protection from financial loss. It is a form of risk manag…

Alternatives to Traditional Methods of Re-Insurance

As you know an insurance is a means of protection from financial loss. It is a form of risk management, primarily used to hedge against the risk of a contingent or uncertain loss. Through insurance we analyse , evaluate ,estimate and transfer outcomes of risk/perils to the insurance company. The insurance company generally in lieu of small payment called “ Premium” issue an insurance policy( insurance contract) by insuring specified risks/perils. Please note that insurance company indemnified us in case of financial loss on happening of those insured risks/perils.

An entity which provides insurance is known as an insurer, an insurance company, an insurance carrier or an underwriter.

The insurance companies also have to secure themselves against large claim for its sustainability and make profit. The Re-insurance concept is insurance of insurance companies. In this process the original insurance company share (subject to its retention) a large portion of stake to other insurance company or they contract with another insurance company to underwrite its proposal in case of large sum assured.

In this case if insurers finds that they have entered into a contract of insurance which is an expensive proposition for them or if they wish to minimize the chances of any possible loss , without ,at the same time giving up the contract, resort to have a devise called reinsurance.

Please note that “ Re-insurance Contract” is between the re-insured and the re-insurer, the assured has nothin to do with it, except so far as it guarantees him against default by his own re-insurance. He cannot sue on it. But the re-insurer’s liability would be discharged by the payment to the assured of the amount at the time of loss. The Original Contract of Insurance and Re-insurance Contracts are two distinct contracts and the re-assured remains solely liable on the original insurance and alone has any claim against the re-insurer.

A policy of re-insurance stipulates for payment by the re-insurer “ as may be paid” by the re-insured. This means that the liability of the re-insurer is coextensive with the liability of insurers.

When the loss or the event insured against occurs, the liability of the re-insurer under the policy of re-insurance comes into existence but the re-insurer shall have to be satisfied by evidence or admission before they may called upon to indemnify the reinsured. It means an re-insurer have all rights to ask evidences and asked by the insurer against a claim from the insured to verify genuineness of the claim.

The liability of re-insurer becomes fixed as soon as the amount payable under original policy is admitted and ascertained. Ex-gratia payments do not bind re-insurer and note that under a policy of re-insurance ,if insurer pay any ex-gratia payment to the original insured ,then re-insurer is not liable to pay his share in the Ex-gratia payment.

Please Note That- in case of an re-insurance contract , the insurer is bound to prove the loss against the re-insurer in the same manner as the original insurer must have proved against him irrespective of the fact whether the insurer has paid the insured or not. [Re,London county commercial Re-insurance Office(1922), 2 Ch 67].

LIMITATION OF TRADITIONAL INSURANCE METHODS:

The inefficiencies of traditional insurance have contributed substantially to the development of Alternative Risk Transfer . An analysis of the costs of traditional insurance covers shows that the difference between the premium and the expected value of the loss is comparatively high. This is often explained as a result of the information asymmetry between (re)insurers and policyholders.

Traditional insurance prices are arrived at, on the basis of average risks, and are therefore higher than the risk-adjusted premium rates for good risks. As a result, good risks are becoming increasingly reluctant to cross-subsidise bad risks, and are turning to self- insurance instead. As such there is inequity in rating. With insurance there is a danger that the policyholder has little incentive to prevent or contain a loss, which means the insurer has to demand a higher average premium (moral hazard problem).

In the case of self- financing, the policyholder has a direct incentive to adopt suitable risk management measures to prevent losses to a reasonable level. Moreover as a result of this phenomenon (moral hazard) insurance companies have set high deductibles (first loss amount met by the insured), which have resulted in the diminishing marginal utility of insureds, because intuitively, risk transfer fails.

Various ART solutions eliminate the problem of moral hazard by defining the loss event on the basis of an independent index or a physical event. However there arises a new phenomenon of basis risk.

There is usually capacity constraint in the industry. Some risks are well understood but considered uninsurable due to their sheer size. For example some natural catastrophe scenarios range from USD50 billion to USD100 billion, depending on the location and intensity of the event. Commodity risks and financial risks aggregate exposures of magnitudes that challenge the capital strength of many commercial insurers. Securitization for example can supplement the capacity of the commercial insurance market by tapping directly into the capital markets. Other ART products shift the focus from risk transfer to risk financing and hence increasing the scope of risk management solutions.

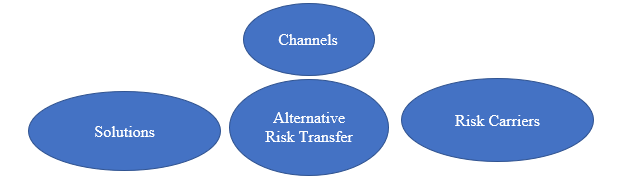

WHAT IS ALTERNATE RISK TRANSFER -LET’S DISCUSS ;

ART is an umbrella term for a range of products, other than conventional annual insurance or reinsurance, which handle financial risk. Generally, these products import techniques, attitudes and language from corporate finance and the capital markets into areas normally dominated by insurers, or vice versa.

Alternative risk transfer (ART) refers to the products and solutions that represent the convergence or integration of capital markets and traditional insurance. The increasingly diverse set of offerings in the ART world has broadened the range of solutions available to corporate risk managers for controlling undesired risks, increased competition amongst providers of risk transfer products and services, and heightened awareness by corporate treasurers about the fundamental relations between corporation finance and risk management. [https://link.springer.com/chapter/10.1007/3-540-26993-2_18].

INVESTOPEDIA- The alternative risk transfer (ART) market is a portion of the insurance market that allows companies to purchase coverage and transfer risk without having to use traditional commercial insurance. The ART market includes risk retention groups (RRGs), insurance pools, and captive insurers, wholly-owned subsidiary companies that provide risk mitigation to its parent company or a group of related companies.

Firstly, alternative distribution channel to specialized direct insurers and reinsurers are for example companies’ own captives, which are potential purchasers of traditional and/or alternative risk transfers products.

Secondly alternative solutions embrace finite risk products whose main aim emphasis is on financing rather than the transfer of risks. Multi-year contracts also play an increasingly important role.

These solutions combine different classes of insurance such as property and casualty risks. Although these products are not essentially new, they are considered to be alternative as they provide the basis for wider ranging covers. These solutions bundle together insurance, finance and in some cases general business risks as well, in the form of multi- year contracts with aggregate retentions.

Other covers that fall into the category of alternative solutions include multi-trigger products, i.e. those which only come into play if insurance and non-insurance loss events occur simultaneously within a specific time frame as well as financing of losses at conditions agreed upon in advance (contingent capital.) Lastly, alternative risk carriers are ultimately capital market investors directly involved in insurance risks. These mainly concern insurance—linked bonds and derivatives.

PLEASE NOTE THAT It is instructive to note that ART techniques have evolved to be used by insurance companies, to satisfy the insured and have also evolved to be used by reinsurance companies to satisfy the requirements of insurance companies. As such there are two forms of ART solutions, one peculiar to the cadent and the other peculiar to the insured, in other words, the two classes are—

Firstly, alternative distribution channel to specialized direct insurers and reinsurers are for example companies’ own captives, which are potential purchasers of traditional and/or alternative risk transfers products.

Secondly alternative solutions embrace finite risk products whose main aim emphasis is on financing rather than the transfer of risks. Multi-year contracts also play an increasingly important role.

These solutions combine different classes of insurance such as property and casualty risks. Although these products are not essentially new, they are considered to be alternative as they provide the basis for wider ranging covers. These solutions bundle together insurance, finance and in some cases general business risks as well, in the form of multi- year contracts with aggregate retentions.

Other covers that fall into the category of alternative solutions include multi-trigger products, i.e. those which only come into play if insurance and non-insurance loss events occur simultaneously within a specific time frame as well as financing of losses at conditions agreed upon in advance (contingent capital.) Lastly, alternative risk carriers are ultimately capital market investors directly involved in insurance risks. These mainly concern insurance—linked bonds and derivatives.

PLEASE NOTE THAT It is instructive to note that ART techniques have evolved to be used by insurance companies, to satisfy the insured and have also evolved to be used by reinsurance companies to satisfy the requirements of insurance companies. As such there are two forms of ART solutions, one peculiar to the cadent and the other peculiar to the insured, in other words, the two classes are—

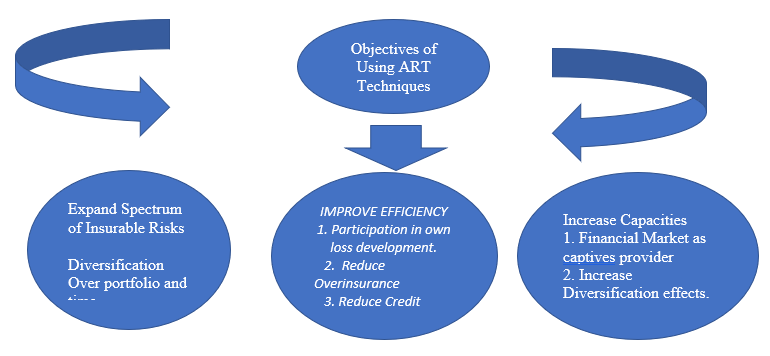

The salient features of Alternative Risk Financing techniques are that the primary objective is that they are developed to complement those already in use in order to improve efficiency of risk transfer. The second goal is to expand the spectrum of insurable risks. The third goal is to generate additional capacity via the capital markets.

Increasingly since the 1960’s larger corporations have created and used their own in house operation, primarily as a means of coordinating insurance buying across the global enterprise. It is found that the earliest forms of ART programmes developed in response to the hard insurance markets. Companies turned to large deductible, loss sensitive rating and retrospective rating insurance programmes to gain independence. This led to the development of wholly owned offshore captives for large corporations and rent-a-captive for small to medium size companies.

Please note that, in the hard insurance, high- interest environment of the early 1990’s finite programmes emerged as another finance tool.

The motives behind finite programme were similar to captives with additional tax and financial benefits.

In the main there are three types of such techniques—

The salient features of Alternative Risk Financing techniques are that the primary objective is that they are developed to complement those already in use in order to improve efficiency of risk transfer. The second goal is to expand the spectrum of insurable risks. The third goal is to generate additional capacity via the capital markets.

Increasingly since the 1960’s larger corporations have created and used their own in house operation, primarily as a means of coordinating insurance buying across the global enterprise. It is found that the earliest forms of ART programmes developed in response to the hard insurance markets. Companies turned to large deductible, loss sensitive rating and retrospective rating insurance programmes to gain independence. This led to the development of wholly owned offshore captives for large corporations and rent-a-captive for small to medium size companies.

Please note that, in the hard insurance, high- interest environment of the early 1990’s finite programmes emerged as another finance tool.

The motives behind finite programme were similar to captives with additional tax and financial benefits.

In the main there are three types of such techniques—

- The alternative risk transfer (ART) market allows companies to purchase coverage and transfer risk without having to use traditional commercial insurance.

- The ART market includes risk retention groups (RRGs), insurance pools, captive insurers, and alternative insurance products.

- Self-insurance is a form of alternative risk transfer when an entity chooses to fund their own losses rather than pay insurance premiums to a third party.

- A number of insurance products are available on the ART market, such as contingent capital, derivatives, and insurance-linked securities.

- Insurance Securitization

- Insuratisation

i. Using insurance capital and skills to price and assume banking risk

ii. Expands the insurable universe of risk towards the inclusion of any surprise which can impact corporate earnings

a. Revenue guarantee

b. Residual value

c. Credit derivatives

d. Enterprise risk.

- Finite

- Captives and protected cells

- Event Risks ( natural disaster etc.) and;

- Financial Risks ( interest rates fluctuation, foreign exchange fluctuation, commodity prices, etc.).

- Self Insurance;

- Risk Retention Groups ;

- Pools ; and

- Captive Insurance Company, rent-a-captive insurance company and protected cell insurance companies;

- Finite or Financial Insurance;

- Multi year, multi line, aggregate or blended or integrated programme.

- SELF INSURANCE- it is a retained level of deductible. This can be through a mutual group or pool within an association o body to share retained risk. This can also be a fund constituted to address a loss if it were to occur. Self-insure is a risk management technique in which a company or individual sets aside a pool of money to be used to remedy an unexpected loss. Theoretically, one can self-insure against any type of damage (like from flood or fire) In practice, however, most people choose to purchase insurance against potentially significant, infrequent losses. Self-insuring against certain losses may be more economical than buying insurance from a third party. The more predictable and smaller the loss is, the more likely it is that an individual or firm will choose to self-insure.

- RISK RETENTION GROUPS It was originated in US Market ,it is a corporation owned and operated by insurance companies , that band together as self-insurers and form an organization that is chartered and licensed as an insurer in at least one state of US to handle liability insurance. In the US it addresses gaps in liability cover for its members such as for medical malpractices.

- Program control

- Long-term rate stability

- Customized Loss control and risk management practices

- Dividends for good loss experience

- Access to reinsurance markets

- Stable source of liability coverage at affordable rates

- Multi-state operations.

- POOLS: A group of insurance companies that pools assets, enabling them to provide an amount of insurance substantially more than can be provided by individual companies to ensure large risks such as nuclear power stations are protected.

- Centralized inventory saves safety stock and average inventory in the system.

- When demands from markets are negatively correlated, the higher the coefficient of variation, the greater the benefit obtained from centralized systems; that is, the greater the benefit from risk pooling.

- The benefits from risk pooling depend directly on relative market behavior. If two markets are competing when demand from both markets are more or less than the average demand, the demands from the market are said to be positively correlated. Thus, the benefits derived from risk pooling decreases as the correlation between demands from both markets becomes more positive.

- CAPTIVES: is an insurer created and wholly owned by its sponsors to provide a facility to aggregate , insure and reinsure only their risks. This process is a legal and adopted in most of countries.

- put their own capital at risk by creating their own insurance company,

- working outside of the commercial insurance marketplace,

- to achieve their risk financing objectives.

- Tailored to specific problems.

- Multi-year, multi-line cover.

- Spread of risk over time and within a policyholder’s portfolio. This is what makes the assumption of traditionally uninsurable risks possible.

- Risk assumption by non- (re)insurers.

Firstly, alternative distribution channel to specialized direct insurers and reinsurers are for example companies’ own captives, which are potential purchasers of traditional and/or alternative risk transfers products.

Secondly alternative solutions embrace finite risk products whose main aim emphasis is on financing rather than the transfer of risks. Multi-year contracts also play an increasingly important role.

These solutions combine different classes of insurance such as property and casualty risks. Although these products are not essentially new, they are considered to be alternative as they provide the basis for wider ranging covers. These solutions bundle together insurance, finance and in some cases general business risks as well, in the form of multi- year contracts with aggregate retentions.

Other covers that fall into the category of alternative solutions include multi-trigger products, i.e. those which only come into play if insurance and non-insurance loss events occur simultaneously within a specific time frame as well as financing of losses at conditions agreed upon in advance (contingent capital.) Lastly, alternative risk carriers are ultimately capital market investors directly involved in insurance risks. These mainly concern insurance—linked bonds and derivatives.

PLEASE NOTE THAT It is instructive to note that ART techniques have evolved to be used by insurance companies, to satisfy the insured and have also evolved to be used by reinsurance companies to satisfy the requirements of insurance companies. As such there are two forms of ART solutions, one peculiar to the cadent and the other peculiar to the insured, in other words, the two classes are—

- insurance alternative risk transfer and

- reinsurance alternative risk transfer.

The salient features of Alternative Risk Financing techniques are that the primary objective is that they are developed to complement those already in use in order to improve efficiency of risk transfer. The second goal is to expand the spectrum of insurable risks. The third goal is to generate additional capacity via the capital markets.

Increasingly since the 1960’s larger corporations have created and used their own in house operation, primarily as a means of coordinating insurance buying across the global enterprise. It is found that the earliest forms of ART programmes developed in response to the hard insurance markets. Companies turned to large deductible, loss sensitive rating and retrospective rating insurance programmes to gain independence. This led to the development of wholly owned offshore captives for large corporations and rent-a-captive for small to medium size companies.

Please note that, in the hard insurance, high- interest environment of the early 1990’s finite programmes emerged as another finance tool.

The motives behind finite programme were similar to captives with additional tax and financial benefits.

In the main there are three types of such techniques—

- finite risk insurance,

- insurance derivatives and

- securitization of insurance risks directly on to the capital markets.

- Firstly there are no suitable indices on which derivatives can be based.

- Secondly derivatives require that the underlying economic variable being tracked is relatively homogeneous.

- http://www.virtusinterpress.org/IMG/pdf/10-22495_rgcv5i4c1art11.pdf

- Re,London county commercial Re-insurance Office(1922), 2 Ch 67.

- https://www.captive.com/captives-101/what-is-captive-insurance.

- https://en.m.wikipedia.org/wiki/Risk_pool

- https://www.insuranceopedia.com/definition/2425/insurance-pool

About Author

FCS DEEPAK P. SINGH

Manager Legal & Compliance

SBI GENERAL INSURANCE COMPANY LIMITED

SBI GENERAL INSURANCE COMPANY LIMITED Mumbai, Maharashtra, India

Mumbai, Maharashtra, India 53

53My Recent Articles

- Surveyor Cannot Apply Deductions Arbitrarily On Amount Of Assessed Loss: Supreme Court Of India

- Insurance Company Cannot Impose Condition That Will Impossible To Comply By Insured

- Mergers & Acquisitions- Under Provisions of ITA,1961

- The Disputes between Landlord & Tenant Governed by Transfer of Property Act 1882 are Arbitrable in Nature

- Damage Caused by the Insurers Taking Possession of Insured Premises & Judicial Opinions

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts