Budget 2022: Changes Under Customs & Excise

Budget 2022: Changes Under Customs & Excise The Finance Minister has introduced the Finance Bill, 2022 in Lok Sabha today, that is 1st February, …

Table of Contents

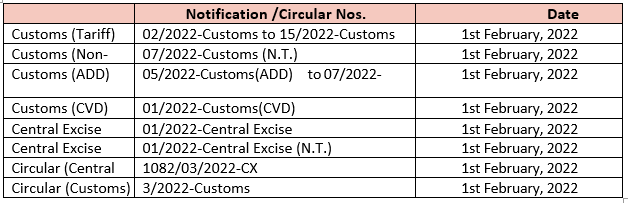

Unless otherwise stated, all changes in rates of duty will take effect from the midnight of 1st February/ 2nd February, 2022. A declaration has been made under the Provisional Collection of Taxes Act, 1931 in respect of clause 97 (a) of the Finance Bill, 2022 so that changes proposed therein take effect from the midnight of 1st February/ 2nd February, 2022. The remaining legislative changes would come into effect only upon the enactment of the Finance Bill, 2022 or from 1st May, 2022.

This document summarises the changes made/ proposed under the Customs and Excise – Section wise in comparative manner for easy digest.

Unless otherwise stated, all changes in rates of duty will take effect from the midnight of 1st February/ 2nd February, 2022. A declaration has been made under the Provisional Collection of Taxes Act, 1931 in respect of clause 97 (a) of the Finance Bill, 2022 so that changes proposed therein take effect from the midnight of 1st February/ 2nd February, 2022. The remaining legislative changes would come into effect only upon the enactment of the Finance Bill, 2022 or from 1st May, 2022.

This document summarises the changes made/ proposed under the Customs and Excise – Section wise in comparative manner for easy digest.

Highlights of Important Changes in Customs

- A comprehensive review of Customs duty exemptions has been undertaken through a process involving crowd sourcing and inputs from various ministries. In this context, about 350 exemptions are being withdrawn. Further, after a detailed review of customs duty exemptions on capital goods and project imports, more than 40 exemptions relating thereto are proposed to be gradually phased out.

- Certain exemptions are being introduced for duty free import of specified goods by bonafide exporter of items like handicraft, apparel, leather goods. The value added export goods shall be exported in six months and exporter shall follow IGCR Rules.

- Custom tariff structure is being simplified by moving the unconditional concessional rates from existing exemption notifications to the First Schedule of Customs Tariff Act. In this process, certain tariff lines and rates have also been rationalised. As a result, applicable BCD rates on sectors such as textiles, chemicals, metals etc. will operate almost entirely through tariff.

- Sunset date is being stipulated as per section 25(4A) of the Customs Act, 1962 in respect of conditional exemption entries in respective notifications. This section, as brought in last year, prescribes validity period of conditional exemptions. Certain exemptions, like international commitments such as FTA, ITA, concessions emanating from FTP like Advance Authorisation, and concessions under Phased Manufacturing Programmes (PMP) have been excluded from the purview of automatic expiry.

- Graded import duty rate structure is being notified to operationalise Phased Manufacturing Plan for wearables, hearables and smart meters.

- Significant legislative changes in the Customs Act are being made, particularly as regards to specifying class of officers and assignment of function and jurisdiction of the proper officers. Certain actions by such officers of Customs, taken in past, are being validated through the Finance Bill, 2022.

- Revised IGCR Rules is being notified to make the entire process digital and transparent.

Important changes in respect of Customs and Central Excise duty (including cesses) are = as detailed below:

(i) Customs duty rate changes: The change in the rates of duty, tariff rates, omission of certain exemption and amendments in certain exemptions, conditions to exemptions, clarifications relating to applicability of SWS etc. (ii) Tarrifisation: An exhaustive exercise has been carried out for simplification of tariff structure. Unconditional concessional rates prescribed through various notifications are being moved to Tariff (First) Schedule in the Customs Tariff Act. These changes in tariff rate shall come into effect from 1st May, 2022. Accordingly, the respective entries in the concerned notifications will be omitted with effect from the 1st May, 2022. The duty rates on such item shall then operate through First Schedule of Customs Tariff Act, 1975. It may however be noted that certain rate changes in the Customs Tariff are coming into effect immediately by virtue of declaration under the Provisional Collection of Taxes Act. (iii) Legislative changes in the Customs Act, Customs Tarff Act and Rules made thereunder:a) Certain significant changes are being made in the Customs Act. The definition of 'proper officer' is being modified; officers of DRI, Audit and Preventive formation are being specifically included in the class of officers of Customs; explicit provision is being made for assigning functions to officer of Customs by the Board or Pr. Commissioner/Commissioner of Customs; concurrent jurisdiction is being provided for in certain circumstance, as the Board may specify; explicit provision is being made to delineate jurisdiction on cases involving short levy/payment of duty or erroneous refund etc. and to provide for concurrent exercise of powers. Further, enabling provisions are being added to tackle the menace of systemic undervaluation. Procedures with respect to Advance Ruling are being rationalised. A section is being added to make unauthorised publication of import or export data, an offence under the Customs Act.

b) In a major trade facilitation measure the Import of Goods Concessional Rate of Duty (IGCR) Rules,2017 have been comprehensively revised. End-to-end automation is being introduced in the entire process; various forms are being standardized and any transaction based permissions or intimations are being done away with. Periodical statement under these rules shall also be submitted on the common portal.

To Read More Details Download PDF Given Below :About Author

A2ZBimal Jain

Chartered Accountant

A2Z Taxcorp LLP

A2Z Taxcorp LLP Delhi, Delhi, India

Delhi, Delhi, India 468

468My Recent Articles

- Actions taken by the department during enquiry need not necessarily be termed as harassment

- Who are liable to generate e-invoice w.e.f October 1, 2022

- Personal penalty cannot be imposed on the Chairman of the Company for failure in ensuring proper accounting of the goods

- Stayed the order of cancellation of GST Registration of the assessee for continuing the trading activities

- Can CA be arrested- Section 69 vs Section 132 of the CGST Act

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts