Capital Loss getting vested with transferee company pursuant to scheme of amalgamation cannot be denied: ITAT

Capital Loss getting vested with transferee company pursuant to scheme of amalgamation cannot be denied: ITAT 2. The only effective issue to be decid…

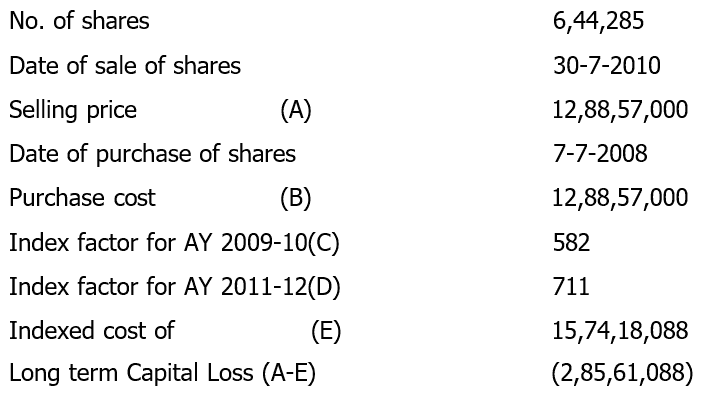

8. The assessee had submitted that the shares of M/s Sparsh BPO Services Pvt Ltd were sold at Rs.200 per share (i.e. the purchase cost) though the market price of the said shares as per Bombay Stock Exchange on the date of sale was only Rs.58 per share. We find that the long term capital loss incurred by the assessee was disallowed by the Ld.AO only on the ground that it was a colourable device as the loss is transferred in the hands of M/s Intelnet Global Services Pvt Ltd on subsequent merger / amalgamation. It is pertinent to note that the scheme of amalgamation had been duly approved by Hon’ble Bombay High Court wherein the treatment of various taxes including indirect taxes had been provided in detail and the Income-tax department being part of Union of India has been given due opportunity before approval of the scheme of amalgamation. Admittedly, the transaction of sale of shares on 30/7/2010 happened much prior to the date of agreement i.e. 7/7/2011. At the time of sale of shares on 30/7/2010, it would not be possible to even pre-empt that a scheme of amalgamation would be filed and the same would get approved by the Hon’ble Bombay High Court. As stated earlier, it is not in dispute that assessee had sold the shares @ Rs.200/- per share being the purchase cost. The sale price of Rs.200 per share has not been disputed by the Revenue at all. In fact, the market price as per the Bombay Stock Exchange on the date of sale was only Rs.58/- per share whereas the assessee has sold the shares at much higher price of Rs.200/- per share. Merely because this transaction had resulted in long term capital loss which had also admittedly arose only due to the benefit of indexation which is statutorily available to the assessee, the Revenue in the instant case is trying to treat the entire transaction as a colourable device and making the assessee act as a conduit to enable the merged entity to have the benefit of carry forward of loss. All these allegations are made by the Ld.AO absolutely without any basis. In fact, this is a classic case where the Ld.AO had denied the benefit which is statutorily available to the assessee as per the Act. In any case, the scheme of merger had already contemplated these transactions of loss on shares by including the same in the scheme and had also considered the loss incurred by the transferor company getting vested with the transferee company pursuant to the scheme of amalgamation. This scheme of amalgamation has been approved by the Hon’ble Bombay High Court vide its order dated 5/3/2013 with effective date of 7/7/2011. Now once the scheme of amalgamation has been approved by the Hon’ble High Court, all the assets and liabilities of the transferor company including the losses would get automatically vested with the transferee company. The same cannot be disturbed or disputed by the Ld.AO at the time of implementation of the scheme of amalgamation. This aspect has been duly appreciated by the Ld.CIT(A) while granting relief to the assessee in para 9.4.1 of his order. In fact, similar issue was adjudicated by the co-ordinate bench of Kolkata Tribunal, which was authored by the undersigned, in the case of Electrocast Sales India Pvt Ltd vs Deputy CIT reported in 64 ITR (Trib) S.N.13 (Kol) dated 9/3/2018 wherein it was held as under:-

8. The assessee had submitted that the shares of M/s Sparsh BPO Services Pvt Ltd were sold at Rs.200 per share (i.e. the purchase cost) though the market price of the said shares as per Bombay Stock Exchange on the date of sale was only Rs.58 per share. We find that the long term capital loss incurred by the assessee was disallowed by the Ld.AO only on the ground that it was a colourable device as the loss is transferred in the hands of M/s Intelnet Global Services Pvt Ltd on subsequent merger / amalgamation. It is pertinent to note that the scheme of amalgamation had been duly approved by Hon’ble Bombay High Court wherein the treatment of various taxes including indirect taxes had been provided in detail and the Income-tax department being part of Union of India has been given due opportunity before approval of the scheme of amalgamation. Admittedly, the transaction of sale of shares on 30/7/2010 happened much prior to the date of agreement i.e. 7/7/2011. At the time of sale of shares on 30/7/2010, it would not be possible to even pre-empt that a scheme of amalgamation would be filed and the same would get approved by the Hon’ble Bombay High Court. As stated earlier, it is not in dispute that assessee had sold the shares @ Rs.200/- per share being the purchase cost. The sale price of Rs.200 per share has not been disputed by the Revenue at all. In fact, the market price as per the Bombay Stock Exchange on the date of sale was only Rs.58/- per share whereas the assessee has sold the shares at much higher price of Rs.200/- per share. Merely because this transaction had resulted in long term capital loss which had also admittedly arose only due to the benefit of indexation which is statutorily available to the assessee, the Revenue in the instant case is trying to treat the entire transaction as a colourable device and making the assessee act as a conduit to enable the merged entity to have the benefit of carry forward of loss. All these allegations are made by the Ld.AO absolutely without any basis. In fact, this is a classic case where the Ld.AO had denied the benefit which is statutorily available to the assessee as per the Act. In any case, the scheme of merger had already contemplated these transactions of loss on shares by including the same in the scheme and had also considered the loss incurred by the transferor company getting vested with the transferee company pursuant to the scheme of amalgamation. This scheme of amalgamation has been approved by the Hon’ble Bombay High Court vide its order dated 5/3/2013 with effective date of 7/7/2011. Now once the scheme of amalgamation has been approved by the Hon’ble High Court, all the assets and liabilities of the transferor company including the losses would get automatically vested with the transferee company. The same cannot be disturbed or disputed by the Ld.AO at the time of implementation of the scheme of amalgamation. This aspect has been duly appreciated by the Ld.CIT(A) while granting relief to the assessee in para 9.4.1 of his order. In fact, similar issue was adjudicated by the co-ordinate bench of Kolkata Tribunal, which was authored by the undersigned, in the case of Electrocast Sales India Pvt Ltd vs Deputy CIT reported in 64 ITR (Trib) S.N.13 (Kol) dated 9/3/2018 wherein it was held as under:-

“Held, that the scheme of amalgamation would be approved by the High Court only after ensuring that the scheme was not prejudicial to the interests of the members of the companies or to public interest. The merger scheme approved by the High Court having in mind the larger public interest could not be disturbed by the Department merely because the assesses was not entitled to the benefits under section 72A, If the Department had any objections it could have raised them prior to sanction of scheme by the court. Once the scheme was approved, it implied that the merger scheme had been done after duly considering the representations from the. Government. The Department had not filed any appeal under section 391(7) of the Companies Act, 1956 against the order of sanction of the amalgamation by the High Court. Therefore it would be clearly barred In/ the doctrine of acquiescence and estoppel. The. accumulated losses of the amalgamating companies, comprising unabsorbed short term capital loss of Rs. 10,26,44,123, unabsorbed long-term capital loss of Rs. 6,34,784 and unabsorbed business loss of Rs. 6,63,574, would belong to the amalgamated company pursuant to paragraph 10(iii) of the scheme of amalgamation which was approved by the High Court. Since the losses belonged to the amalgamated company, i. e... the. assessees, the provisions of section 72 and section 74 would come into play with respect to set off thereof against the respective incomes of the assessee. In view of this, the non-compliance, of section 72A as held bi/ the Commissioner (Appeals) did not hold any water.”

9. Moreover, we further find that the Hon’ble Jurisdictional High Court in the case of Sadanand S Varde & Ors vs State of Maharashtra & Ors reported in 247 ITR 609 (Bom) had categorically held that order of the Company Court sanctioning the scheme of amalgamation would be binding and the same cannot be permitted to be challenged in a collateral proceeding. 10. In view of the above, we do not find any infirmity in the order of Ld.CIT(A) allowing the claim of long term capital loss in the hands of the assessee company. Accordingly, grounds raised by the Revenue are dismissed. 11. Since the relief is granted on merits, we do not deem it fit to adjudicate the grounds raised by the assessee in its Cross Objection challenging the validity of re-assessment. No opinion is rendered herein by us on the same and they are left open. 12. In the result, the appeal of the Revenue is dismissed and the Cross Objection of the assessee is dismissed as infructuous. Click here to DownloadAbout Author

CA Pratibha Goyal

Co Founder

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts