CBIC Clarification on applicability of demand and penalty provisions under CGST ACT in respect of transactions involving fake invoices

CBIC Clarification on applicability of demand and penalty provisions under CGST ACT in respect of transactions involving fake invoices The Central Bo…

CBIC Clarification on applicability of demand and penalty provisions under CGST ACT in respect of transactions involving fake invoices

The Central Board of Indirect Taxes & Custom (CBIC) vide Circular No. 171/03/2022-GST dated 06th July 2022 issued Clarification on various issues relating to the applicability of demand and penalty provisions under CGST ACT 2017 in respect of transactions involving fake invoices.

The Circular is Given Below:

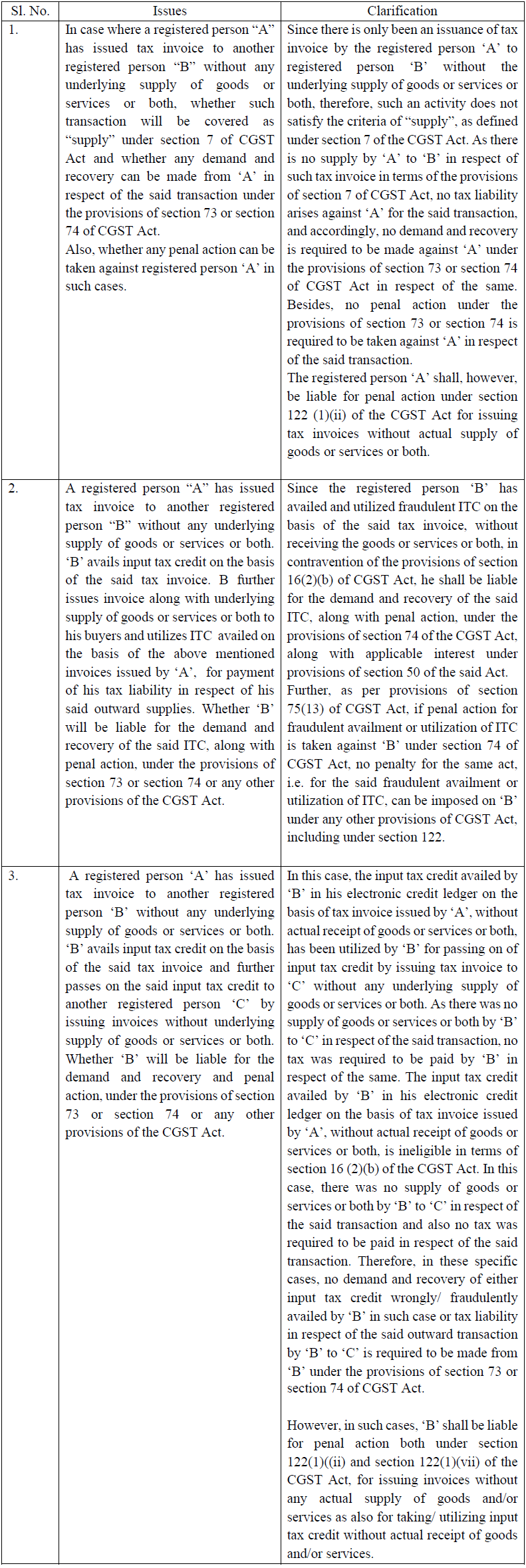

A number of cases have come to notice where the registered persons are found to be involved in issuing tax invoice, without actual supply of goods or services or both(hereinafter referred to as “fake invoices”), in order to enable the recipients of such invoices to avail and utilize input tax credit (hereinafter referred to as “ITC”) fraudulently. Representations are being received from the trade as well as the field formations seeking clarification on the issues relating to the applicability of demand and penalty provisions under the Central Goods and Services Tax Act, 2017 (hereinafter referred to as “CGST Act”), in respect of such transactions involving fake invoices. In order to clarify these issues and to ensure uniformity in the implementation of the provisions of law across the field formations, the Board, in exercise of its powers conferred by section 168 (1) of the CGST Act, hereby clarifies the issues detailed hereunder.

2. The fundamental principles that have been delineated in the above scenarios may be adopted to decide the nature of demand and penal action to be taken against a person for such unscrupulous activity. Actual action to be taken against a person will depend upon the specific facts and circumstances of the case which may involve a complex mixture of above scenarios or even may not be covered by any of the above scenarios. Any person who has retained the benefit of transactions specified under sub-section (1A) of section 122 of CGST Act, and at whose instance such transactions are conducted, shall also be liable for penal action under the provisions of the said sub-section. It may also be noted that in such cases of wrongful/ fraudulent availment or utilization of input tax credit, or in cases of issuance of invoices without supply of goods or services or both, leading to wrongful availment or utilization of input tax credit or refund of tax, provisions of section 132 of the CGST Act may also be invokable, subject to conditions specified therein, based on facts and circumstances of each case.

3. It is requested that suitable trade notices may be issued to publicize the contents of this Circular.

4. Difficulty, if any, in implementation of the above instructions may please be brought to the notice of the Board. Hindi version would follow.

For Official Circular Download PDF Given Below:

2. The fundamental principles that have been delineated in the above scenarios may be adopted to decide the nature of demand and penal action to be taken against a person for such unscrupulous activity. Actual action to be taken against a person will depend upon the specific facts and circumstances of the case which may involve a complex mixture of above scenarios or even may not be covered by any of the above scenarios. Any person who has retained the benefit of transactions specified under sub-section (1A) of section 122 of CGST Act, and at whose instance such transactions are conducted, shall also be liable for penal action under the provisions of the said sub-section. It may also be noted that in such cases of wrongful/ fraudulent availment or utilization of input tax credit, or in cases of issuance of invoices without supply of goods or services or both, leading to wrongful availment or utilization of input tax credit or refund of tax, provisions of section 132 of the CGST Act may also be invokable, subject to conditions specified therein, based on facts and circumstances of each case.

3. It is requested that suitable trade notices may be issued to publicize the contents of this Circular.

4. Difficulty, if any, in implementation of the above instructions may please be brought to the notice of the Board. Hindi version would follow.

For Official Circular Download PDF Given Below:

2. The fundamental principles that have been delineated in the above scenarios may be adopted to decide the nature of demand and penal action to be taken against a person for such unscrupulous activity. Actual action to be taken against a person will depend upon the specific facts and circumstances of the case which may involve a complex mixture of above scenarios or even may not be covered by any of the above scenarios. Any person who has retained the benefit of transactions specified under sub-section (1A) of section 122 of CGST Act, and at whose instance such transactions are conducted, shall also be liable for penal action under the provisions of the said sub-section. It may also be noted that in such cases of wrongful/ fraudulent availment or utilization of input tax credit, or in cases of issuance of invoices without supply of goods or services or both, leading to wrongful availment or utilization of input tax credit or refund of tax, provisions of section 132 of the CGST Act may also be invokable, subject to conditions specified therein, based on facts and circumstances of each case.

3. It is requested that suitable trade notices may be issued to publicize the contents of this Circular.

4. Difficulty, if any, in implementation of the above instructions may please be brought to the notice of the Board. Hindi version would follow.

For Official Circular Download PDF Given Below:About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts