Chartered Accountant can't be prosecuted for Form 15CB based on non-genuine documents submitted by client: HC:

Chartered Accountant can't be prosecuted for Form 15CB based on non-genuine documents submitted by client, says Madras High Court

CA prosecution under PMLA

Table of Contents

"4. It is submitted that the averments contained in the criminal revision petition are not true and denied in toto. It is further submitted that the petitioner as a practising Chartered Accountant, free to practise his profession and render professional services in the matter of filing VAT return to the business entity in the name and style of M/s.Copy Care, which is owned by A-7. Whereas, the Petitioner/A-6, in this case travelled beyond the professional scope, ethics and value and in the process issued the Form - 15CB in the name of M/s.B.K.Electro Tool Products, using the PAN number of A-2 and photo identity of A-1 and ultimately facilitated the money mule, to operate the account in the name of M/s.B.K.Electro Tool Products through seven AD Banks to send foreign exchange to the extent of USD 8,237,007.95 equivalent to INR 59,47,03,760.46, without disclosing the identity of the beneficial owner and end-use. The Petitioner/A-6 is deeply involved in the scam and it is no way connected within the scope of professional services as a chartered accountant and therefore the criminal revision petition is liable to the dismissed as devoid of merit.

5. I submit that the Petitioner/A-6 made an admission that he issued certificate in Form 15CB in favour of the M/s.B.K.Electro Tool Products at the request of A-7. The Petitioner/A-6 made further admission that the certificate in Form- 15CB is one of the supporting documents to make foreign outward remittance. The above submission of the Petitioner/Accused-6 crystallise that he never interacted or looked into financial state of affairs of either A2 or A1 whose PAN number and Photograph were being used in operating the account of M/s.B.K.Electro Tool Product. The only excuse sought by the Petitioner/A-6 that there was a bonafide belief on his part with A-7 that made him to sign the Form 15CB showing the photograph of A1 and PAN number of A2 as an owner of M/s.B.K.Electro Tool Products. Whereas, A-7 was examined u/s.50 of PMLA, 2002, on 12.01.2022, A-7 neither identified the Petitioner/A-6 nor A-1 or A-2, with reference to photograph, in reply to question no.8. The combined reading of submission of the Petitioner/A-6 and the statement given by A7 before the IO is contradictory with one another. The truth can be unravelled only at the time of trial and it is premature at this point of time. Further, the foreign outward remittances are made through the seven AD banks and not only with one bank as projected by the petitioner/A-6."

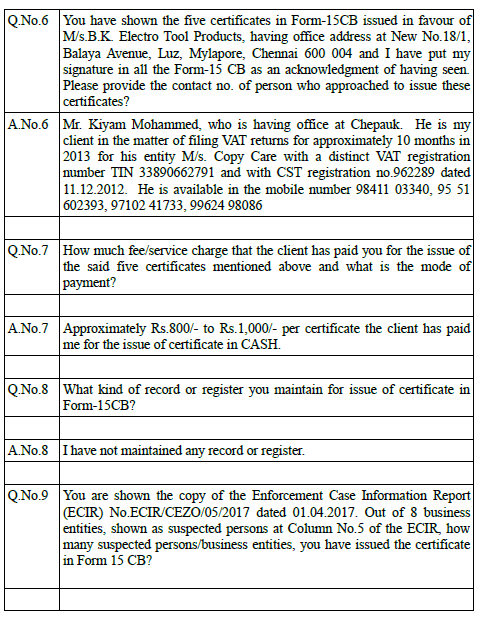

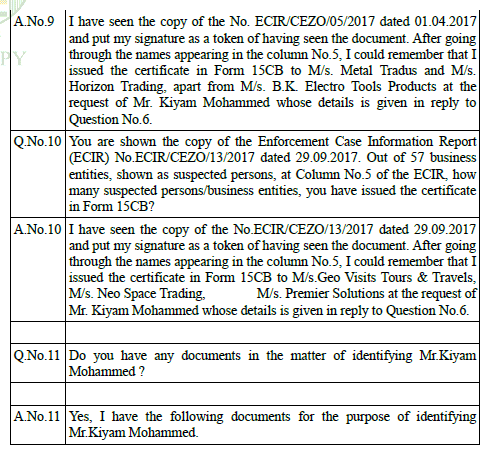

Mr.Nithyaesh Natraj, learned counsel, took us through the statement of Murali Krishna Chakrala that was given by him under Section 50 of the PML Act as well the averments in the complaint and submitted that if not for Murali Krishna Chakrala, the involvement of Kiyam Mohammed (A7) and Abdul Haleem (A8) would have never come to light and that Murali Krishna Chakrala had, in the course of his professional duties, given five numbers of Form 15CB, after scrutinizing the documents that were presented to him by Kiyam Mohammed (A7). Murali Krishna Chakrala did not have any reason to suspect the genuineness of the import documents. Therefore, it is seen that the petitioner has neither directly or indirectly participated in the generation of proceeds of crime in any manner whatsoever. Mr.Nithyaesh Natraj, learned counsel, further contended that Form 15CB for making overseas payment towards import is not required even under the law and that is why, except the State Bank of Travancore, all the other nationalised banks had transferred the funds based on the import documents without insisting upon a Form 15CB from a Chartered Accountant. Had Murali Krishna Chakrala been a part of the conspiracy, he would not have gullibly uploaded the certificates into the Income Tax Department portal on the same day. Mr.Nithyaesh Natraj, learned counsel, took us through the statement of Murali Krishna Chakrala that was given to the Enforcement Directorate, which is in question and answer form and the relevant portion therefrom is extracted ad verbum :

Order of Court:

9. The submission of Mr.Nithyaesh Natraj, learned counsel, that mere issuance of five numbers of Form 15CB at the request of Kiyam Mohammed [A7], would not, by itself, bring Murali Krishna Chakrala into the net of conspiracy to indulge in money laundering, merits acceptance. It is clear that he had merely received Rs.1,000/- for a certificate without anything more. That apart, he had helped the Enforcement Directorate to identify Kiyam Mohammed [A7], who was the mastermind of the whole operation and therefore, Murali Krishna Chakrala would be the best witness for linking A1 to A5 with A7 and A8. 10. As regards the requirements for submission of Form 15CB, we find from the records that only the State Bank of Travancore had insisted upon the said certificates and not the other six banks through which, foreign remittances were made by Kiyam Mohammed [A7] and Abdul Haleem [A8]. The complaint and the accompanying background show that Abdul Haleem [A8] had operated the bank accounts and Kiyam Mohammed [A7] had facilitated the opening of the bank account and preparation of various documents by availing the services of various persons including Murali Krishna Chakrala, an Auditor, for the limited purpose of obtaining Form 15CB for transferring monies from State Bank of Travancore, Mount Road Branch. A reading of paragraph Nos.81 and 143 of the impugned complaint, which have been extracted supra, shows that Murali Krishna Chakrala had issued five numbers of Form 15CB in favour of B.K.Electro Tool Products, which were handed over by him to his client Kiyam Mohammed [A7] for which, a sum of Rs.1,000/- per certificate was given to him as remuneration. 11. Even on a demurrer, on a perusal of Form 15CB, we find that a Chartered Accountant is required to only examine the nature of the remittance and nothing more. The Chartered Accountant is not required to go into the genuineness or otherwise of the documents submitted by his clients. This could be compared with the legal opinion that are normally given by panel lawyers of banks, after scrutinizing title documents without going into their genuinity. A Panel Advocate, who has no means to go into the genuinity of title deeds and who gives an opinion based on such title deeds, cannot be prosecuted along with the principal offender. Applying the same anomaly, we find that the prosecution of Murali Krishna Chakrala, in the facts and circumstances of the case at hand, cannot be sustained. 12. In the result, this Criminal Revision is allowed and the order dated 26.08.2022 passed in Crl.M.P.No.2864 of 2022 in Spl.C.C.No.07 of 2021 on the file of XII Additional Special Court for CBI cases at Chennai, is set aside and the petitioner is discharged from the prosecution. However, we make it clear that, it is open to the prosecution to enlist Murali Krishna Chakrala as a prosecution witness, if they so desire. Consequently, connected miscellaneous petition is closed.About Author

CA Deepak Gupta

Co Founder

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 3423

3423My Recent Articles

- UltraTech Cement slapped with Rs. 808.78 Cr Income Tax Demand

- GST: High Court upheld constitutional validity of Section 16(2)(c), asks government to address ITC issues of genuine purchasers

- Old vs New Tax Regime for Tax Year 2026-27

- High court criticizes Income Tax Department for not releasing ITR Utilities despite 11 years of directions

- Fino Payments Bank CEO Rishi Gupta Gets Bail in GST Case, Bank Clarifies No Direct Link

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts