Decline in GST Revenues from West Bengal:

The State Finance Minister, Shri Pankaj Chaudhary in a written reply to a question raised in Lok Sabha said, “There is decline in GST Revenues from West Bengal.”

GST Revenues declined in the State of West Bengal

Decline in GST Revenues from West Bengal

The Minister of State in the Ministry of Finance, Shri Pankaj Chaudhary in a written reply to a question raised in Lok Sabha said, “There is decline in GST Revenues from West Bengal.”

Shri Saumitra Khan asked these questions in Lok Sabha:

Will the Minister of FINANCE be pleased to state:

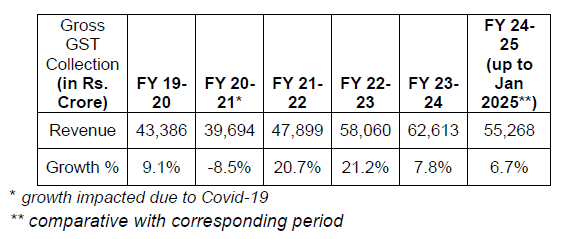

(a) whether the Government is aware that share of West Bengal in national GST collections has decreased from 4.6% in 2019-20 to 4% in 2024-25;

(b) the factors that have contributed to this decline in West Bengal;

(c) the measures are being implemented to address the decline in GST collections from West Bengal and to enhance the State's revenue performance;

(d) whether the Government has conducted any assessments to understand the impact of this revenue decline on West Bengal's fiscal health and public expenditure and if so, the details thereof;

and

(e) the manner in which the Government plans to support West Bengal in improving GST compliance and expanding its tax base to reverse the downward trend in revenue collections?

The Minister of State in the Ministry of Finance, Shri Pankaj Chaudhary replied:

(a) and (b): Yes Sir. However, the GST collections in the State of West Bengal from 2019-20 to 2024-25 has been increasing, as detailed below:

GST revenues are dependent on various factors including the general conditions of the economy and the pattern of consumption in the State. However, no specific study for West Bengal has been undertaken in this regard.

(c): The Government, on the recommendations of the GST Council, undertakes several measures for reforms in GST from time to time, as detailed in reply to part (e) below.

(d): This does not arise in light of the afore-mentioned data.

(e): The Government, on the recommendations of the GST Council, has taken several measures for reforms in GST. These, inter-alia, include measures for improving tax compliance such as mandating e-way bill, ITC matching, e-invoice for B2C suppliers, deployment of artificial intelligence and machine-based analytics, Aadhaar authentication for registration, calibrated action on non-filers, stop filers, targeted assessment-based action on risky tax payer, etc.

Further, regular action is taken to detect fake firms through data analytics and other intelligence by the Central and State authorities. Till now, 2 National Conference of Enforcement Chiefs of State and Central GST Formations have been held in respect of activities being undertaken by the enforcement formations and the importance of maintaining ease of doing business. As a measure to track down and take action against masterminds, there are sufficient legal provisions in the CGST Act which are as under: -

i. Punishment for tax evaded or the amount of ITC wrongly availed or utilised or the amount of refunds wrongly taken;

ii. Suspension / Cancellation of registration of taxpayers involved in fake ITC cases;

iii. Blocking of ITC in electronic credit ledger;

iv. Provisional attachment of property / bank accounts, etc. for the recovery of Government dues.

GST revenues are dependent on various factors including the general conditions of the economy and the pattern of consumption in the State. However, no specific study for West Bengal has been undertaken in this regard.

(c): The Government, on the recommendations of the GST Council, undertakes several measures for reforms in GST from time to time, as detailed in reply to part (e) below.

(d): This does not arise in light of the afore-mentioned data.

(e): The Government, on the recommendations of the GST Council, has taken several measures for reforms in GST. These, inter-alia, include measures for improving tax compliance such as mandating e-way bill, ITC matching, e-invoice for B2C suppliers, deployment of artificial intelligence and machine-based analytics, Aadhaar authentication for registration, calibrated action on non-filers, stop filers, targeted assessment-based action on risky tax payer, etc.

Further, regular action is taken to detect fake firms through data analytics and other intelligence by the Central and State authorities. Till now, 2 National Conference of Enforcement Chiefs of State and Central GST Formations have been held in respect of activities being undertaken by the enforcement formations and the importance of maintaining ease of doing business. As a measure to track down and take action against masterminds, there are sufficient legal provisions in the CGST Act which are as under: -

i. Punishment for tax evaded or the amount of ITC wrongly availed or utilised or the amount of refunds wrongly taken;

ii. Suspension / Cancellation of registration of taxpayers involved in fake ITC cases;

iii. Blocking of ITC in electronic credit ledger;

iv. Provisional attachment of property / bank accounts, etc. for the recovery of Government dues.

GST revenues are dependent on various factors including the general conditions of the economy and the pattern of consumption in the State. However, no specific study for West Bengal has been undertaken in this regard.

(c): The Government, on the recommendations of the GST Council, undertakes several measures for reforms in GST from time to time, as detailed in reply to part (e) below.

(d): This does not arise in light of the afore-mentioned data.

(e): The Government, on the recommendations of the GST Council, has taken several measures for reforms in GST. These, inter-alia, include measures for improving tax compliance such as mandating e-way bill, ITC matching, e-invoice for B2C suppliers, deployment of artificial intelligence and machine-based analytics, Aadhaar authentication for registration, calibrated action on non-filers, stop filers, targeted assessment-based action on risky tax payer, etc.

Further, regular action is taken to detect fake firms through data analytics and other intelligence by the Central and State authorities. Till now, 2 National Conference of Enforcement Chiefs of State and Central GST Formations have been held in respect of activities being undertaken by the enforcement formations and the importance of maintaining ease of doing business. As a measure to track down and take action against masterminds, there are sufficient legal provisions in the CGST Act which are as under: -

i. Punishment for tax evaded or the amount of ITC wrongly availed or utilised or the amount of refunds wrongly taken;

ii. Suspension / Cancellation of registration of taxpayers involved in fake ITC cases;

iii. Blocking of ITC in electronic credit ledger;

iv. Provisional attachment of property / bank accounts, etc. for the recovery of Government dues.About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.