DECODING MCA SCHEME FOR RELAXATION OF CHARGES

DECODING MCA SCHEME FOR RELAXATION OF CHARGES MCA SCHEME FOR RELAXATION RELATED TO CREATION OR MODIFICATION OF CHARGES MCA vide General Circ

DECODING MCA SCHEME FOR RELAXATION OF CHARGES

Disclaimer:

IN NO EVENT THE AUTHOR SHALL BE LIABLE FOR ANY DIRECT, INDIRECT, SPECIAL OR INCIDENTAL DAMAGE RESULTING FROM OR ARISING OUT OF OR IN CONNECTION WITH THE USE OF THIS INFORMATION.

THIS HAS BEEN SHARED FOR KNOWLEDGE PURPOSES ONLY.

Disclaimer:

IN NO EVENT THE AUTHOR SHALL BE LIABLE FOR ANY DIRECT, INDIRECT, SPECIAL OR INCIDENTAL DAMAGE RESULTING FROM OR ARISING OUT OF OR IN CONNECTION WITH THE USE OF THIS INFORMATION.

THIS HAS BEEN SHARED FOR KNOWLEDGE PURPOSES ONLY.

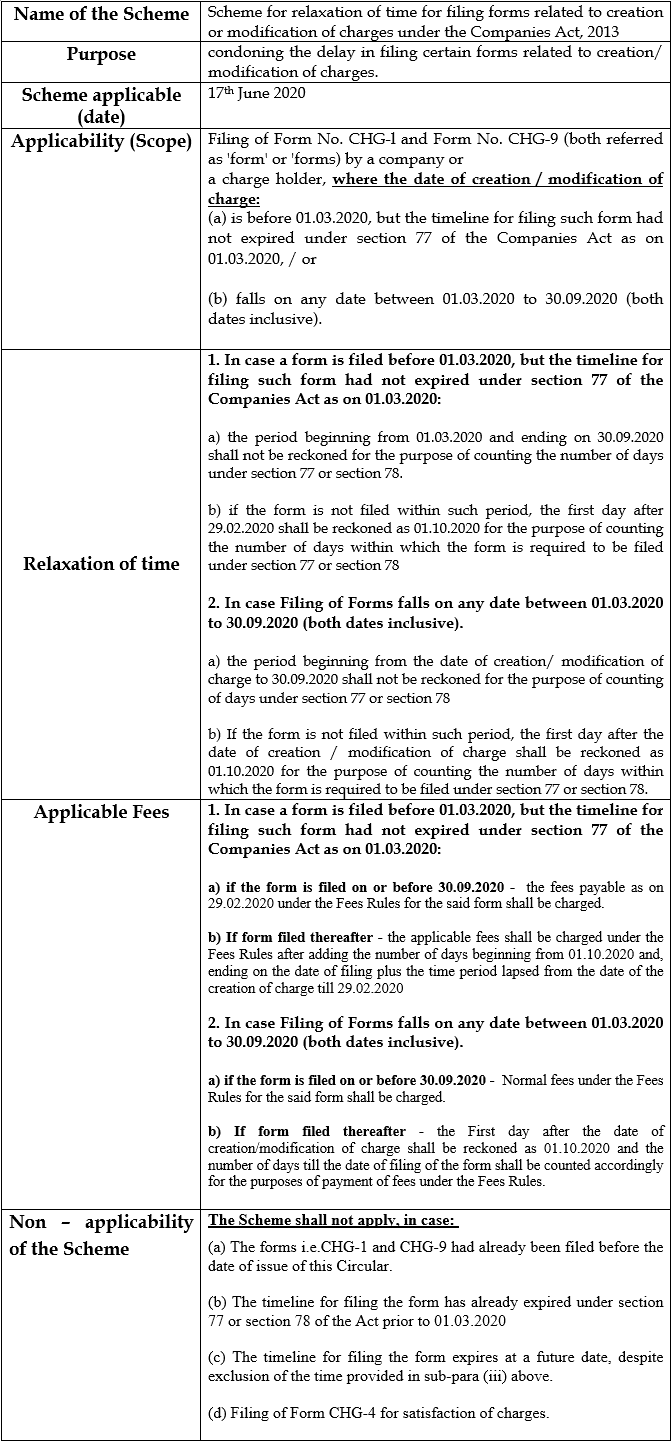

MCA SCHEME FOR RELAXATION RELATED TO CREATION OR MODIFICATION OF CHARGES

MCA vide General Circular no. 23/ 2020 dated 17th June, 2020 has issued Scheme for relaxation of time for filing forms related to creation or modification of charges under the Companies Act, 2013 for all Companies Registered with ROC.- Provisions Related to Filings

- Representation & COVID-19

- MCA Relaxations on Charge related filings

- Decoding Scheme related to Charge Matters

Disclaimer:

IN NO EVENT THE AUTHOR SHALL BE LIABLE FOR ANY DIRECT, INDIRECT, SPECIAL OR INCIDENTAL DAMAGE RESULTING FROM OR ARISING OUT OF OR IN CONNECTION WITH THE USE OF THIS INFORMATION.

THIS HAS BEEN SHARED FOR KNOWLEDGE PURPOSES ONLY.About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.