Decoding Taxation Laws (Amendment) Ordinance, 2019

Decoding Taxation Laws (Amendment) Ordinance, 2019 The Government has brought in the Taxation Laws (Amendment) Ordinance 2019 to make certai

Decoding Taxation Laws (Amendment) Ordinance, 2019

The Government has brought in the Taxation Laws (Amendment) Ordinance 2019 to make certain amendments in the Income-tax Act 1961 and the Finance (No. 2) Act 2019.

Here is an Analysis of some of the important provisions of Taxation Laws (Amendment) Ordinance 2019

Insertion of section 115BAA in Income Tax Act

Currently, domestic companies (who are not eligible to opt for Section 115BA) are chargeable to tax at the rate of 25% if their total turnover or gross receipt do not exceed Rs. 400 crore during the financial year 2017-18 otherwise tax is charged at the rate of 30% plus applicable surcharge and cess.

In order to promote growth and investment, a new provision has been inserted in the Income-tax Act with effect from FY 2019-20 which allows any domestic company an option to pay income-tax at the rate of 22% subject to condition that they will not avail any exemption/incentive. The effective tax rate for these companies shall be 25.17% inclusive of surcharge & cess. Also, such companies shall not be required to pay Minimum Alternate Tax.

Further, the option to avail of the benefit of Section 115BAA must be exercised on or before the due date of furnishing return of income under Section 139(1) in the prescribed manner. This option once exercised cannot be subsequently withdrawn.

Insertion of section 115BAB in Income Tax Act

In order to attract fresh investment in manufacturing and thereby provide boost to Make-in-India initiative of the Government, another new provision has been inserted in the Income-tax Act with effect from FY 2019-20 which allows any new domestic company incorporated on or after 1stOctober 2019 making fresh investment in manufacturing, an option to pay income-tax at the rate of 15%.

This benefit is available to companies which do not avail any exemption/incentive and commences their production on or before 31st March, 2023.

The effective tax rate for these companies shall be 17.01% inclusive of surcharge & cess.

Also, such companies shall not be required to pay Minimum Alternate Tax.

Further, the option to avail of the benefit of Section 115BAB must be exercised on or before the due date of furnishing return of income under Section 139(1) in the prescribed manner. This option once exercised cannot be subsequently withdrawn.

A company which does not opt for the concessional tax regime and avails the tax exemption/incentive shall continue to pay tax at the pre-amended rate. However, these companies can opt for the concessional tax regime after expiry of their tax holiday/exemption period. After the exercise of the option they shall be liable to pay tax at the rate of 22% and option once exercised cannot be subsequently withdrawn. Further, in order to provide relief to companies which continue to avail exemptions/incentives, the rate of Minimum Alternate Tax has been reduced from existing 18.5% to 15%.

Amendment of Part II of First Schedule

- In order to stabilise the flow of funds into the capital market, it is provided that enhanced surcharge introduced by the Finance (No.2) Act, 2019 shall not apply on capital gains arising on sale of equity share in a company or a unit of an equity oriented fund or a unit of a business trust liable for securities transaction tax, in the hands of an individual, HUF, AOP, BOI and AJP.

- The enhanced surcharge shall also not apply to capital gains arising on sale of any security including derivatives, in the hands of Foreign Portfolio Investors (FPIs).

Amendment of section 115QA

In order to provide relief to listed companies which have already made a public announcement of buy-back before 5thJuly 2019, it is provided that tax on buy-back of shares in case of such companies shall not be charged.

Tax rates for Assessment Year 2020-21

After the Taxation Laws (Amendment) Ordinance, 2019, the revised tax rates for the Assessment Year 2020-21 shall be as follows:

IN CASE OF INDIVIDUAL, HUF, AOP, BOI OR AJP

Individuals being Super Senior Citizens (Age 80 years or more at any time during the financial year)

|

Slabs |

Tax Rates |

|

Up to Rs. 5,00,000 |

- |

|

Rs. 5,00,001 to Rs. 10,00,000 |

20% |

|

More than Rs. 10,00,000 |

30% |

Individuals being Senior Citizens (Age 60 years or more but less than 80 years at any time during the financial year)

|

Slabs |

Tax Rates |

|

Up to Rs. 3,00,000 |

- |

|

Rs. 3,00,001 to Rs. 5,00,000 |

5% |

|

Rs. 5,00,001 to Rs. 10,00,000 |

20% |

|

More than Rs. 10,00,000 |

30% |

Others Individuals, HUFs, AOP, BOI OR AJP

|

Slabs |

Tax Rates |

|

Up to Rs. 2,50,000 |

- |

|

Rs. 2,50,001 to Rs. 5,00,000 |

5% |

|

Rs. 5,00,001 to Rs. 10,00,000 |

20% |

|

More than Rs. 10,00,000 |

30% |

Rebate under Section 87A

For the Assessment Year 2020-21, in case of a resident individual, rebate up to Rs. 12,500 is allowed from the amount of tax if his total income does not exceed Rs. 500,000. Where his total income includes long-term capital gains arising from transfer of equity shares, units of equity oriented mutual fund or units of business trust as covered under Section 112A, such rebate shall not allowed from tax payable on such capital gains.

Surcharge

For the Assessment Year 2020-21, the rate of surcharge shall be as under:

|

Nature of Income |

Range of Total Income |

||||

|

Up to Rs. 50 lakh |

More than Rs. 50 lakh but up to Rs. 1 crore |

More than Rs. 1 crore but up to Rs. 2 crore |

More than Rs. 2 crore but up to Rs. 5 crore |

More than Rs. 5 crore |

|

|

Short-term capital gain covered under Section 111A |

Nil |

10% |

15% |

15% |

15% |

|

Long-term capital gain covered under Section 112A |

Nil |

10% |

15% |

15% |

15% |

|

Unexplained income chargeable to tax under Section 115BBE |

25% |

25% |

25% |

25% |

25% |

|

Any other income |

Nil |

10% |

15% |

25% |

37% |

Health and Education Cess

The health and education cess is levied at the rate of 4% on the amount of income tax plus surcharge

IN CASE OF FIRM OR LLP

Tax Rates

A firm (including LLP) is liable to pay tax at the flat rate of 30% of taxable income.

Surcharge

If total income of a firm or LLP exceeds Rs. 1 crore, the surcharge is levied at the rate of 12% on the amount of tax payable on total income.

Health and Education Cess

The health and education cess is levied at the rate of 4% on the amount of income tax plus surcharge

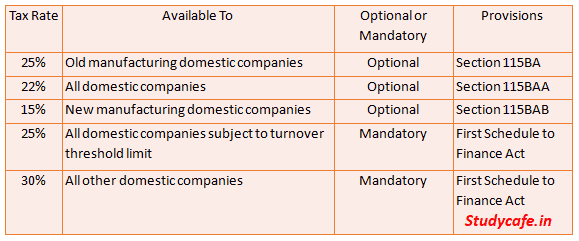

IN CASE OF DOMESTIC COMPANY

Tax Rates

The tax rates for the domestic company for the Assessment Year 2020-21 shall be as follows:

|

Section |

Conditions |

In any other case |

|

Section 115BA |

1. The co. is set up and registered on or after 01.03.2016 2. It is engaged in manufacture or production of any article or thing 3. It does not claim specified exemption, incentive or deduction |

25% |

|

Section 115BAB |

1. The co. is set up and registered on or after 01.10.2019 2. It is engaged in manufacture or production of any article or thing 3. It commences manufacturing on or after 01-10-2019 but on or before 31-03-2023 4. It does not claim specified exemption, incentive or deduction |

15% |

|

Section 115BAA |

If co. does not claim specified exemption, incentive or deduction |

22% |

|

First Schedule to Finance Act |

If total turnover or gross receipts during the financial year 2017-18 does not exceed Rs. 400 crore |

25% |

|

First Schedule to Finance Act |

Any other domestic company |

30% |

Surcharge

|

Company |

Range of Total Income |

||

|

Rs. 1 crore or less |

Above Rs. 1 crore but up to Rs. 10 crore |

Above Rs. 10 crore |

|

|

Domestic Company opting for section 115BA |

Nil |

7% |

12% |

|

Domestic Company opting for section 115BAA* |

10% |

10% |

10% |

|

Domestic Company opting for section 115BAB* |

10% |

10% |

10% |

|

Any other company |

Nil |

7% |

12% |

* Surcharge shall be levied at a flat rate of 10% only on income offered to tax under section 115BAA or Section 115BAB. Surcharge on all other incomes, which are chargeable to tax at special rate, shall be levied as per the existing provisions, i.e., at the rate of 7% or 12%, as the case may be.

Health and Education Cess

The health and education cess is levied at the rate of 4% on the amount of income tax plus surcharge

IN CASE OF FOREIGN COMPANY

Tax Rates

A foreign company is liable to pay tax at the rate of 40% of taxable income.

Surcharge

The rate of surcharge in case of a foreign company shall be 2% and 5% if its total income exceeds Rs. 1 crores and 10 crores, respectively.

Health and Education Cess

The health and education cess is levied at the rate of 4% on the amount of income tax plus surcharge

IN CASE OF LOCAL AUTHORITY

Tax Rate

A local authority is liable to pay tax at the rate of 30% of taxable income.

Surcharge

If total income of local authority exceeds Rs. 1 crore, the surcharge is levied at the rate of 12% on the amount of tax payable on total income.

Health and Education Cess

The health and education cess is levied at the rate of 4% on the amount of income tax plus surcharge

IN CASE OF CO-OP. SOCIETY OR CO-OP. BANK

Tax rates

|

Income range |

Tax rates |

|

Up to Rs. 10,000 |

10% |

|

Rs. 10,000 to Rs. 20,000 |

20% |

|

Above Rs. 20,000 |

30% |

Surcharge

If total income of co-op. society exceeds Rs. 1 crore, the surcharge is levied at the rate of 12% on the amount of tax payable on total income.

Health and Education Cess

The health and education cess is levied at the rate of 4% on the amount of income tax plus surcharge

MAT

|

Nature of assessee |

Rate |

|

Domestic Company located in IFSC |

9% |

|

Other Companies |

15% |

However, the provisions of MAT shall not be applicable in case of following:

- Foreign companies which do not have permanent establishment (PE) in India or who are opting for presumptive taxation scheme of Section 44B, Section 44BB, Section 44BBA or Section 44BBB;

- Income accruing or arising to a company from life insurance business as referred to in Section 115B;

- A domestic company which has opted for the tax regime of Section 115BAA or Section 115BAB

I hope you enjoyed the article. You can Follow us on our twitter channel for regular updates https://twitter.com/castudycafe

About Author

CA Pratibha Goyal

Co Founder

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.