Directorate General of Systems and Data Management Launched New GST Reports in ADVAIT:

The Directorate General of Systems and Data Management has issued an regarding the launch of New GST Reports in the Advanced Analytics in Indirect Taxation (ADVAIT).

Launched New GST Reports in ADVAIT

Table of Contents

Directorate General of Systems and Data Management Launched New GST Reports in ADVAIT

The Directorate General of Systems and Data Management has issued an regarding the launch of New GST Reports in the Advanced Analytics in Indirect Taxation (ADVAIT).

ADVAIT has a variety of reports, dashboards and data science models that offer deep insights into taxpayer behaviour and compliance. Continuing with its endeavour to promote data-driven action, ADVAIT team is happy to announce the launch of five new GST reports on the portal. The reports are summarised below:

The report is based on broad aggregation only to highlight notable cases, and not on invoice data. There may be cases where the ineligible credit availed may not be captured by the report due to GSTIN specific last date of filing of return being earlier than the generalised date. Due caution may be exercised by officers in checking the eligibility of ITC being availed by the taxpayers, as per law.

To Read More Download PDF Given Below:

The report is based on broad aggregation only to highlight notable cases, and not on invoice data. There may be cases where the ineligible credit availed may not be captured by the report due to GSTIN specific last date of filing of return being earlier than the generalised date. Due caution may be exercised by officers in checking the eligibility of ITC being availed by the taxpayers, as per law.

To Read More Download PDF Given Below:

I. Performance of top taxpayers as per returns (GST_RPTPDR_185):

This report provides the top taxpayers’ revenue, cash and ITC trends for the selected jurisdiction as per returns for the selected financial year, along with the percent change over last two years. (total three-year trend). The report will assist officers in monitoring the performance of top taxpayers in their jurisdiction. It may be noted that there are already six other reports in ADVAIT to individually monitor the trends in tax payments, cash, ITC etc. The details are as under: a) GST ITC Vs TURNOVER COMPARISION: This report helps in identifying the taxpayers with disproportionate growth in ITC as compared to taxable turnover. b) ITC AVAILMENT AND UTILIZATION TREND: The report provides the list of taxpayers whose ITC utilization as compared to ITC availed for a month falls in the selected range. c) ITC UTILIZATION GROWTH RATE MONITORING-GST: This report is to monitor the increase or decrease in the ITC utilization by taxpayers. With the help of this report, jurisdictional officers can identify the taxpayers having huge growth or decline in ITC utilization. d) GST 90:10 ANALYSIS OF TAX PAYMENT: This report provides the list of top taxpayers who are contributing to 90% revenue (tax paid through cash) of the selected Commissionerate for a financial year. e) JURISIDICTION WISE GST REVENUE: This report provides details of tax paid in cash and tax paid using ITC during selected period and for selected jurisdiction, along with comparative values for same period of previous financial year. f) TOP 1000 PAN BASED ON TAX PAYMENT: The report provides the list of top 1000 taxpayers basis their pan India tax payment during the selected financial year.II. Amount of ITC availed after the time limit prescribed under Section 16(4) – V1 (GST_RPTPDR_155):

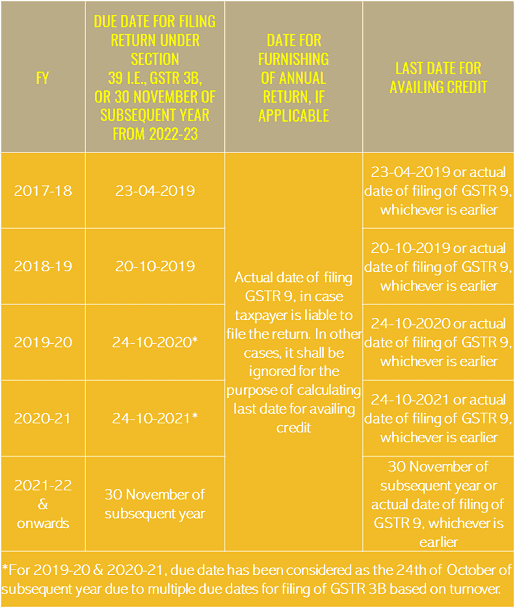

Section 16(4) of CGST Act, 2017 provides that “A registered person shall not be entitled to take input tax credit in respect of any invoice or debit note for supply of goods or services or both after the thirtieth day of November following the end of financial year to which such invoice or debit note pertains or furnishing of the relevant annual return, whichever is earlier”. The said section was amended by Finance Act 2022, which earlier provided that the time limit to avail ITC shall be earlier of ‘Due date of furnishing the return under section 39 for the month of September following the end of the financial year to which such invoice/debit note pertains, or Furnishing of the relevant Annual Return’. For 2017-18, the last date was the due date of furnishing of the return for March 2019. This report provides details of ITC availed after the prescribed time limit under Section 16(4) of CGST Act, 2017 for selected GSTIN for a financial year. The ITC availed will be bifurcated into IGST, CGST, SGST and Cess. The details of due dates for availment as per Section 16 (4) are detailed below:

The report is based on broad aggregation only to highlight notable cases, and not on invoice data. There may be cases where the ineligible credit availed may not be captured by the report due to GSTIN specific last date of filing of return being earlier than the generalised date. Due caution may be exercised by officers in checking the eligibility of ITC being availed by the taxpayers, as per law.

To Read More Download PDF Given Below:

About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts