Due Date of TAR stands extended to 15th October as a result of ITR Due Date Extension:

As with the Audited ITR Extension, the due date for filing the Tax Audit Report has now been automatically extended to 15th October.

TAR Due Dated Extended

Due Date of TAR stands extended to 15th October as a result of ITR Due Date Extension

Recently, the Central Board of Direct Taxes (CBDT) has extended the due date of Income Tax Returns for taxpayers who have their accounts audited till 15th November 2024.

This Audited ITR Extension brought positive outcomes for taxpayers and tax professionals.

As with the Audited ITR Extension, the due date for filing the Tax Audit Report has now been automatically extended to 15th October. This extension is due to the TAR deadline being directly related to the ITR filing deadline.

It is provided in Section 44AB that -

Audit of accounts of certain persons carrying on business or profession.

44AB. Every person,-

(a) carrying on business shall, if his total sales, turnover or gross receipts, as the case may be, in business exceed or exceeds one crore rupees in any previous year:

Provided that in the case of a person whose-

(a) an aggregate of all amounts received including the amount received for sales, turnover or gross receipts during the previous year, in cash, does not exceed five percent of the said amount; and

(b) an aggregate of all payments made including the amount incurred for expenditure, in cash, during the previous year does not exceed five percent of the said payment,

this clause shall have effect as if for the words "one crore rupees", the words "ten crore rupees" had been substituted:

Provided further that for the. purposes of this clause, the payment or receipt, as the case may be, by a cheque drawn on a bank or by a bank draft, which is not account payee, shall be deemed to be the payment or receipt, as the case may be, in cash; or

(b) carrying on profession shall if his gross receipts in profession exceed fifty lakh rupees in any previous year; or

(c) carrying on the business shall, if the profits and gains from the business are deemed to be the profits and gains of such person under section 44AE or section 44BB or section 44BBB, as the case may be, and he has claimed his income to be lower than the profits or gains so deemed to be the profits and gains of his business, as the case may be, in any previous year; or

(d) carrying on the profession shall, if the profits and gains from the profession are deemed to be the profits and gains of such person under section 44ADA and he has claimed such income to be lower than the profits and gains so deemed to be the profits and gains of his profession and his income exceeds the maximum amount which is not chargeable to income-tax in any previous year; or

(e) carrying on the business shall if the provisions of sub-section (4) of section 44AD are applicable in his case and his income exceeds the maximum amount which is not chargeable to income tax in any previous year,

get his accounts of such previous year audited by an accountant before the specified date and furnish by that date the report of such audit in the prescribed form duly signed and verified by such accountant and setting forth such particulars as may be prescribed

[Provided that this section shall not apply to a person. who declares profits and gains for the previous year in accordance with the provisions of sub-section (1) of section 44AD or sub-sec1ion (I) of section 44ADA:]

Provided further that this section shall not apply to the person, who derives income of the nature referred to in section 44B or section 44BBA, on and from the 1st day of April 1985 or, as the case may be, the date on which the relevant section came into force, whichever is later:

Provided also that in a case where such person is required by or under any other law to get his accounts audited, it shall be sufficient compliance with the provisions of this section if such person gets the accounts of such business or profession audited under such law before the specified date and furnishes by that date the report of the audit as required under such other law and a further report by an accountant in the form prescribed under this section.

Explanation.- For the purposes of this section,-

(i) "accountant" shall have the same meaning as in the Explanation below sub-section (2) of section 288;

(ii) "specified date", in relation to the accounts of the assessee of the previous year relevant to an assessment year, means date one month prior to the due date for furnishing the return of income under sub-section (I) of section 139.

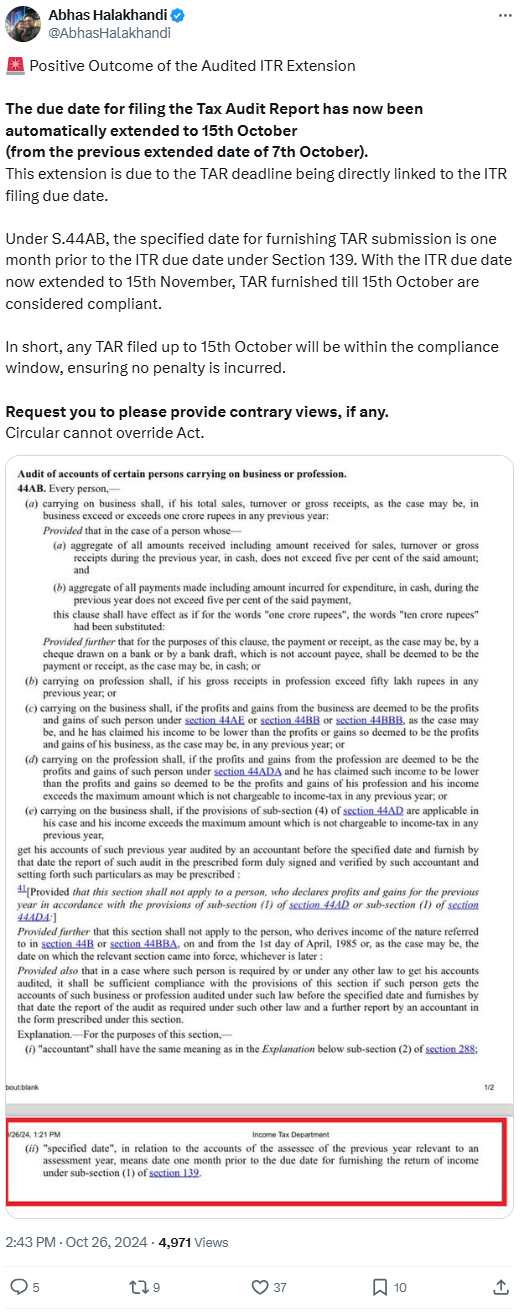

Abhas Halakhandi also shared this news on his Twitter account.

He wrote, "🚨 Positive Outcome of the Audited ITR Extension. The due date for filing the Tax Audit Report has now been automatically extended to 15th October (from the previous extended date of 7th October). This extension is due to the TAR deadline being directly linked to the ITR filing due date.

Under S.44AB, the specified date for furnishing TAR submission is one month prior to the ITR due date under Section 139. With the ITR due date now extended to 15th November, TAR furnished till 15th October is considered compliant.

In short, any TAR filed up to 15th October will be within the compliance window, ensuring no penalty is incurred.

Request you to please provide contrary views, if any. Circular cannot override Act."

About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.