ECO cannot avail ITC on specified services u/s 9(5) of GST Act: CBIC Clarification:

CBIC has made an important clarification in respect of ITC availed by electronic commerce operators where services specified under Section 9(5) of CGST, 2017.

CBIC clarifies ECO cannot avail ITC on specified services u/s 9(5)

ECO cannot avail ITC on specified services u/s 9(5) of GST Act: CBIC Clarification

Circular Number 240/34/2024-GST dated 31-Dec-2024

CBIC has made an important clarification in respect of input tax credit availed by electronic commerce operators where services specified under Section 9(5) of the Central Goods and Services Tax Act, 2017 are supplied through their platform.

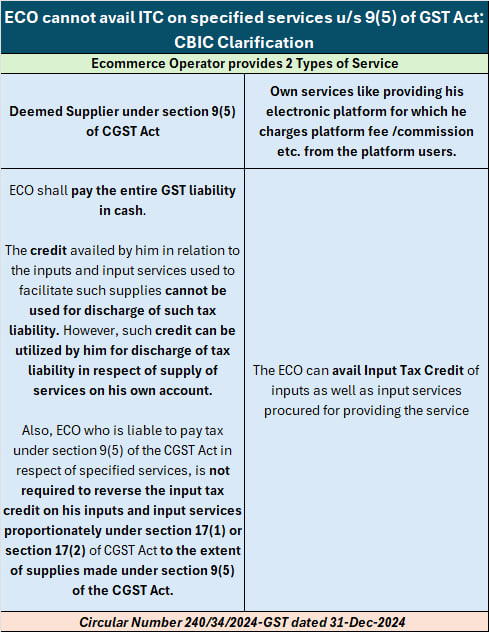

Issue: Whether an electronic commerce operator, required to pay tax under section 9(5) of the CGST Act, is liable to reverse the proportionate input tax credit on his inputs and input services to the extent of supplies made under section 9(5) of the CGST Act?

It is clarified that an Electronic Commerce Operator, who is liable to pay tax under section 9(5) of the CGST Act in respect of specified services, is not required to reverse the input tax credit on his inputs and input services proportionately under section 17(1) or section 17(2) of the CGST Act to the extent of supplies made under section 9(5) of the CGST Act.

Issue: Whether an electronic commerce operator, required to pay tax under section 9(5) of the CGST Act, is liable to reverse the proportionate input tax credit on his inputs and input services to the extent of supplies made under section 9(5) of the CGST Act?

It is clarified that an Electronic Commerce Operator, who is liable to pay tax under section 9(5) of the CGST Act in respect of specified services, is not required to reverse the input tax credit on his inputs and input services proportionately under section 17(1) or section 17(2) of the CGST Act to the extent of supplies made under section 9(5) of the CGST Act.

Issue: Whether an electronic commerce operator, required to pay tax under section 9(5) of the CGST Act, is liable to reverse the proportionate input tax credit on his inputs and input services to the extent of supplies made under section 9(5) of the CGST Act?

It is clarified that an Electronic Commerce Operator, who is liable to pay tax under section 9(5) of the CGST Act in respect of specified services, is not required to reverse the input tax credit on his inputs and input services proportionately under section 17(1) or section 17(2) of the CGST Act to the extent of supplies made under section 9(5) of the CGST Act.

It is further clarified that ECO will be required to pay the full tax liability on account of supplies under section 9(5) of the CGST Act only through an electronic cash ledger. The credit availed by him in relation to the inputs and input services used to facilitate such supplies cannot be used for the discharge of such tax liability under section 9(5) of the CGST Act. However, such credit can be utilized by him for the discharge of tax liability in respect of the supply of services on his own account.

For Official Circular Download PDF Given Below:

About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.