FAQs on Income Tax Reforms introduced in Budget 2025:

The Finance Minister presented Union Budget 2025 in the parliament today that brought major changes. Personal Income-tax reforms introduced with special focus on middle class.

FAQs on Personal Income Tax Reforms

Table of Contents

FAQs on Income Tax Reforms introduced in Budget 2025

The Finance Minister Nirmala Sitharaman presented Union Budget 2025 in the parliament today that brought major changes. Personal Income-tax reforms introduced with special focus on middle class.

Here are frequently asked questions given related to personal income-tax reforms focused on middle class.

*For income above 12 lac, in the case of resident individuals, marginal relief shall be allowable .

*For income above 12 lac, in the case of resident individuals, marginal relief shall be allowable .

To Read More Download PDF Given Below:

To Read More Download PDF Given Below:

Q.1. What is ‘New Regime’?

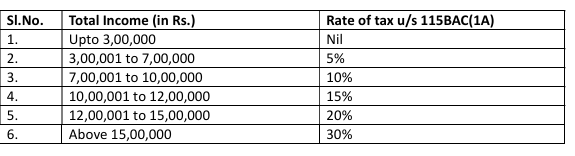

Ans. New regime provides for concessional tax rates and liberal slabs. However, no deductions are allowed in the new regime (other than those specified for e.g. 80JJAA, 80M, standard deduction).Q.2. What are the tax slabs in earlier new regime?

Ans. The Finance (No.2) Act, 2024 had the following slabs in the new tax regime for person, being an individual or Hindu undivided family or association of persons [other than a cooperative society], or body of individuals, whether incorporated or not, or an artificial juridical person referred to in sub-clause (vii) of clause (31) of sec on 2: -

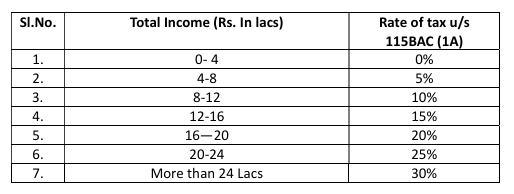

Q.3. What are the new slabs in the proposed new regime introduced by Finance Bill, 2025?

Ans. The new slabs proposed are as under:

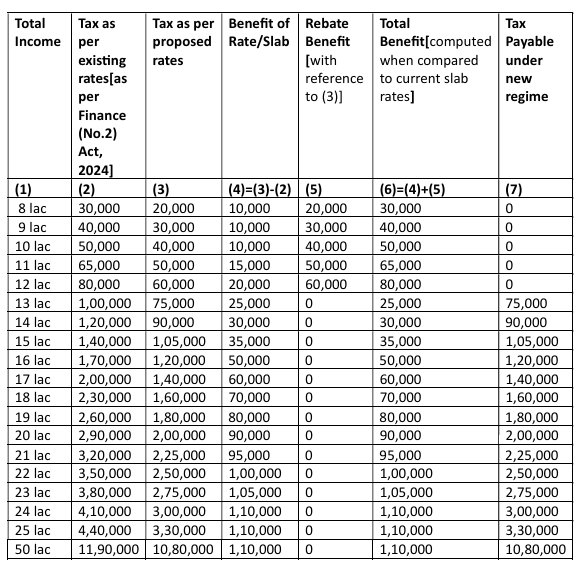

Q.4. What is the tax benefit for different category of taxpayers (0-24 lacs)?

*For income above 12 lac, in the case of resident individuals, marginal relief shall be allowable .

Q.5. What is the maximum total income for which tax liability for individual taxpayers is NIL.

Ans. In the proposed new tax regime, the maximum total income for which tax liability for individual taxpayers is NIL is Rs.12 lakhs.Q.6. To claim benefit of NIL tax liability mentioned above, what are the steps required to be taken?

Ans. The benefit of such Nil tax liability mentioned above is available only in the new tax regime. This New tax regime is the default regime. To avail the benefit of rebate allowable under proposed provisions of new tax regime, only return is to be filed otherwise no other step is required to be taken.Q.7. The change in tax slabs is beneficial for which category of persons?

Ans. New tax regime is applicable to person, being an individual or Hindu undivided family or association of persons [other than a co-operative society], or body of individuals, whether incorporated or not, or an artificial juridical person referred to in sub-clause (vii) of clause (31) of section 2. Accordingly, change in tax slabs will benefit all these persons.Q.8. How will a person who has an income Rs.12 lac benefit from new rates?

Ans. Any individual earlier was required to pay a tax of Rs.80,000 (in the new regime) for an income of Rs.12 lacs. Now he will be required to pay nil tax on such income.Q.9. Whether the limit of total income for NIL tax payments has increased in this budget?

Ans. Yes, the limit of total income for NIL tax payments in the new tax regime has been increased to Rs.12 lakhs in this budget provided the taxpayer files ITR to avail the rebate.Q.10. What was the earlier limit of income for nil tax payment?

Ans. Earlier the limit of income for nil tax payment was Rs.7 lac. By increasing this limit to Rs.12 lakh around one crore assessees who were earlier required to pay tax varying from Rs.20,000 to Rs.80,000 will be now paying nil tax.Q.11. Is the standard deduction on salary available in the new regime?

Ans Yes, a standard deduction of Rs.75,000 is available to a tax payer in the new regime. Therefore, a salaried tax payer will not be required to pay any tax where his income before standard deduction is less than or equal to Rs.12,75,000.Q.12. Whether standard deduction is available in old regime?

Ans. Standard deduction of Rs.50,000 is available in old regime.Q.13. How many tax payers will benefit from the new rates and slabs?

Ans. Presently, for AY 2024-25, about 8.75 crore persons have filed their ITRs. All such assessees who were paying tax in the new tax regime will benefit from the change in rates and slabs.Q.14. What is the extra amount available to the taxpayers as a result of this change?

Ans. Approximately Rs.1 lakh crore will be made available in the hands of the taxpayers by virtue of changes in slab, rates and rebate.Q.15. How is the marginal relief available to individuals?

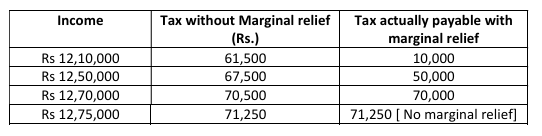

Ans. In the new regime under sec on 115BAC(1A), marginal relief is available to only resident individuals who have income marginally above Rs.12 lacs. For example, for a person having income of Rs.12, 10,000, in the absence of marginal relief, the tax, works out to be Rs.61,500 (5% of Rs.4 lacs+10% of 4 lac and 15% of Rs.10 thousand). However, due to marginal relief, the amount of tax to be actually paid is Rs.10,000.Q.16. How much tax will be paid by a tax payer having income of Rs.12,10,000? What is marginal relief?

Ans. The tax liability on such tax payer by way of slabs only is Rs.61,500. How ever a person having Rs.12 lac income pays nil tax. By providing marginal relief it has been ensured that the tax payable by a person having income marginally above Rs.12 lacs is required to pay only marginal amount of tax equal to the amount of income above Rs.12 lacs so that his carry home is also Rs.12 lacs. In this case he will be required to pay a tax of Rs.10,000.

To Read More Download PDF Given Below:About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.