Filing Reply or Taking Actions during General Penalty Proceedings u/s 125

Filing Reply or Taking Actions during General Penalty Proceedings u/s 125 1. When can a General Penalty be imposed on a taxable person Gener

Filing Reply or Taking Actions during General Penalty Proceedings u/s 125

1. When can a General Penalty be imposed on a taxable person

General Penalty can be imposed on a taxable person when he/she contravenes any of provisions of Section 125 of CGST/ SGST Act or any rules made there under, for which no penalty is separately provided for in this Act. Normally, penalties not related to tax deficiency can be covered under General Penalty.

2. Can General Penalty be imposed on a person not registered under the GST Act

Yes, under Section 125, General penalty can be imposed on any personRegistered or Unregisteredwho had committed offence/contravened provisions of the CGST/SGST Act, for which no penalty is provided under any other section specifically.

3. Can General Penalty be imposed on a person on whom a penalty is already levied under some other section for the same default

No. In case penalty is levied under any other section for some default, then no penalty can be imposed u/s 125 for the same default on the same person.

4. What is the procedure of the General Penalty Assessment Proceedings u/s 125

Following is the procedure of the General Penalty Assessment Proceedings u/s 125:

1.Adjudicating or Assessing Authority(A/A)issues a "Show Cause Notice" to the taxpayerand, if personal hearing is required, also schedules a date/time and venue. In case of no reply from the taxpayer, A/A issues a Reminder. Maximum three reminders can be issued.

2.Taxpayer can reply to the issued notice on the GST Portal and also request for a personal hearing in case A/A has not called for a personal hearing in the issued notice. Additionally, if required, he/she can also file for application of extension offline. If A/A approves application of extension, A/A will issue an adjournment with the new date/time and venue of Personal hearing, if required. Adjournment can be allowed maximum 3 times.

3. If Personal hearing is not required, A/A, on the basis of taxpayer's reply, issuesGENERAL PENALTYor DROP PROCEEDING Order.If Personal hearing is required, A/A conducts the personal hearing and on that basis issue the Order. If taxpayer does not reply, even after the issue of three reminders, A/A issues theOrderas per his/her discretion.

5. How much time is given to the taxpayer for replying to the Show Cause Notice (SCN)

15 days of time is given for furnishing a reply to the SCN.

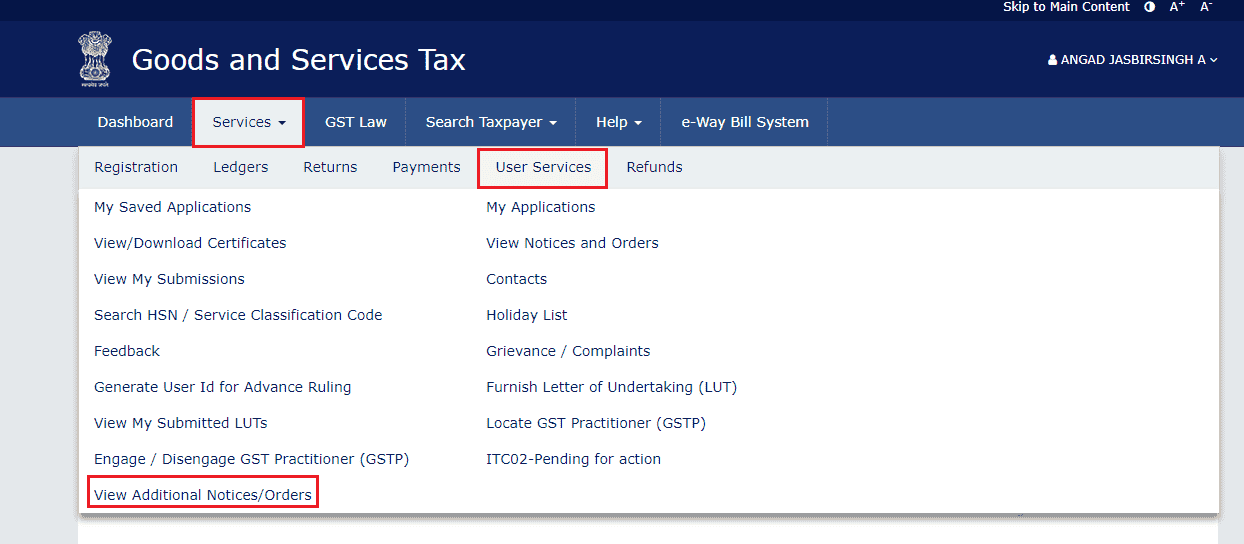

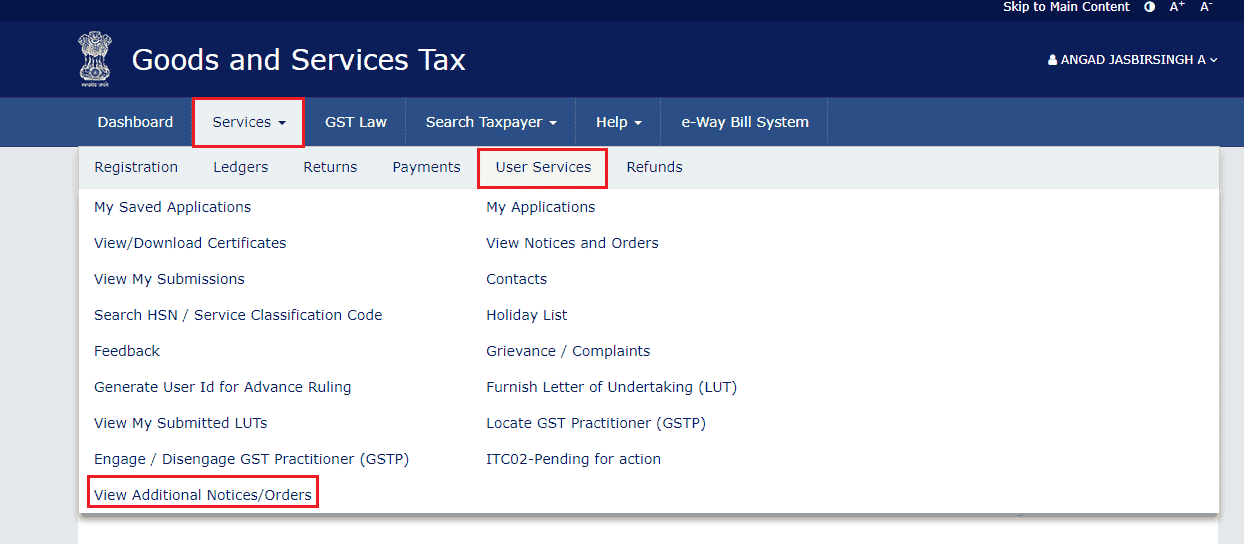

6. Where can the taxpayers view the SCN issued to them

After logging in to the GST portal, the taxpayers can navigate toServices>User Services>View Additional Notices and Ordersoption.

7. What are the next steps after a taxpayer has replied to the notice

If reply to notice furnished by taxable person within 15 days or extended period is satisfactory, then proceedings can be dropped by the officer by issuing an order to that effect and no further action will be taken in this regard.

If reply to notice furnished by taxable person within 15 days or extended period is not satisfactory, then officer may issue the order for imposing penalty.

8. What is the next step if a taxpayer neither replies to notice within time specified in notice nor attends personal hearing

In such a case, the tax official can issue a reminder to the taxpayer. Maximum three reminders can be given. If the taxpayer neither replies to notice within time specified in notice nor attends personal hearing even after issue of reminder(s), the tax official will issue the Order.

9. In case notice/order etc. is issued by post/special messenger, then what will be the Date of issue

Date of delivery will be considered as "Date of issue".

10. During General Penalty proceedings, at what different stages will a taxpayer receive an intimation via SMS or email

During General Penalty proceedings, a taxpayer will receive an intimation via SMS or email at the following stages:

1. Issue of SCN

2. Submission of each Reply filed by the taxpayer

3. Issue of each Adjournment notice

4. Issue of each Reminder

5. Issue of Penalty Order or Drop Proceeding Order

11. How many reminders can be issued to a taxpayer after the issue of SCN

After the issue of SCN, maximum 3 Reminders can be issued on the Portal.

12. How much time is given to the taxpayers for responding and attending the Personal Hearing

Taxpayer in general are given a time of 15 days to attend personal hearing. They can also seek extension (offline). However, the tax officer can accept the application of extension and grant Adjournments up to maximum of three times on the Portal.

13. During the General PenaltyAssessment/Adjudication proceedings, what all Status changes does the case undergo

During the General PenaltyAssessment/Adjudication proceedings, the case may undergo following Status changes:

Pending for reply by taxpayer:When A/A issues a"Show Cause Notice" to the taxpayer

Reply furnished, pending for Order by tax officer:When taxpayer replies to the Notice issued by A/A

Reminder No. 1 issued:When A/A issues firstReminder to the taxpayer in case the taxpayer has not responded to the Show Cause Notice within the time specified therein

Reminder No. 2 issued:When A/A issues secondReminder to the taxpayer in case the taxpayer has not responded to the Show Cause Notice within the time specified therein

Reminder No. 3 issued:When A/A issues thirdReminder to the taxpayer in case the taxpayer has not responded to the Show Cause Notice within the time specified therein

Reply not furnished, pending for order:When taxpayer does not reply to the issued Notice even after 3 reminders

Order for creation of demand issued:WhenGENERAL PENALTY Orderis issued by A/A to the taxpayer

Order for dropping proceedings issued:WhenDROP PROCEEDING Orderis issued by A/A to the taxpayer

About Author

CA Deepak Gupta

Co Founder

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 3423

3423My Recent Articles

- UltraTech Cement slapped with Rs. 808.78 Cr Income Tax Demand

- GST: High Court upheld constitutional validity of Section 16(2)(c), asks government to address ITC issues of genuine purchasers

- Old vs New Tax Regime for Tax Year 2026-27

- High court criticizes Income Tax Department for not releasing ITR Utilities despite 11 years of directions

- Fino Payments Bank CEO Rishi Gupta Gets Bail in GST Case, Bank Clarifies No Direct Link

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts