Food Delivery App required to report supplies under sec 9(5) in Table 3.1(a) of GSTR-3B: clarifies GSTN

Food Delivery App required to report supplies under sec 9(5) in Table 3.1(a) of GSTR-3B: clarifies GSTN 1. Notification No. 17/2021-Central Tax (Rate…

Food Delivery App required to report supplies under sec 9(5) in Table 3.1(a) of GSTR-3B: clarifies GSTN

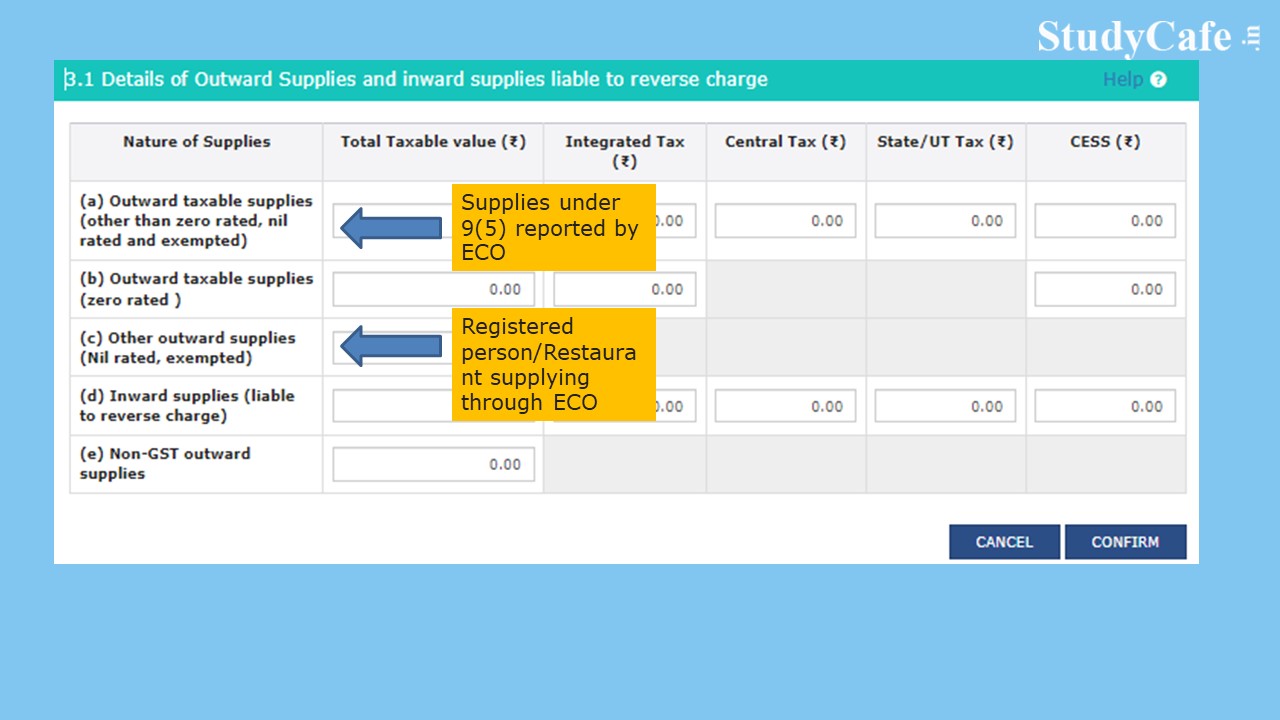

1. Notification No. 17/2021-Central Tax (Rate) and 17/2021-Integrated Tax (Rate) dated 18.11.2021 were issued in response to the GST Council's decision to notify "Restaurant Service" under section 9(5) of the CGST Act, 2017, along with other services notified previously such as motor cabs, accommodation, and housekeeping services, where the tax on such supplies would be paid by the electronic commerce operator if such supplies were made through it. As a result, beginning January 1, 2022, the e-commerce operator will be responsible for paying the tax on supplies of restaurant services provided through e-commerce operators.

[caption id="attachment_113137" align="aligncenter" width="1280"] Food Delivery App required to report supplies under sec 9(5) in Table 3.1(a) of GSTR-3B: clarifies GSTN[/caption]

2. In light of the foregoing, E-commerce operators and registered persons should report taxable supply notified under section 9(5) of the CGST Act, 2017 and corresponding provisions in the IGST/SGST/UTGST Act as follows.

Food Delivery App required to report supplies under sec 9(5) in Table 3.1(a) of GSTR-3B: clarifies GSTN[/caption]

2. In light of the foregoing, E-commerce operators and registered persons should report taxable supply notified under section 9(5) of the CGST Act, 2017 and corresponding provisions in the IGST/SGST/UTGST Act as follows.

Please see CBIC Circular No. 167/23/2021, dated 17.12.2021, for further information.

Please see CBIC Circular No. 167/23/2021, dated 17.12.2021, for further information.

Food Delivery App required to report supplies under sec 9(5) in Table 3.1(a) of GSTR-3B: clarifies GSTN[/caption]

2. In light of the foregoing, E-commerce operators and registered persons should report taxable supply notified under section 9(5) of the CGST Act, 2017 and corresponding provisions in the IGST/SGST/UTGST Act as follows.

Please see CBIC Circular No. 167/23/2021, dated 17.12.2021, for further information.About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts