Foreign Salary of Non-Resident Not Taxable in India Merely Due to NRE Account Credit: ITAT:

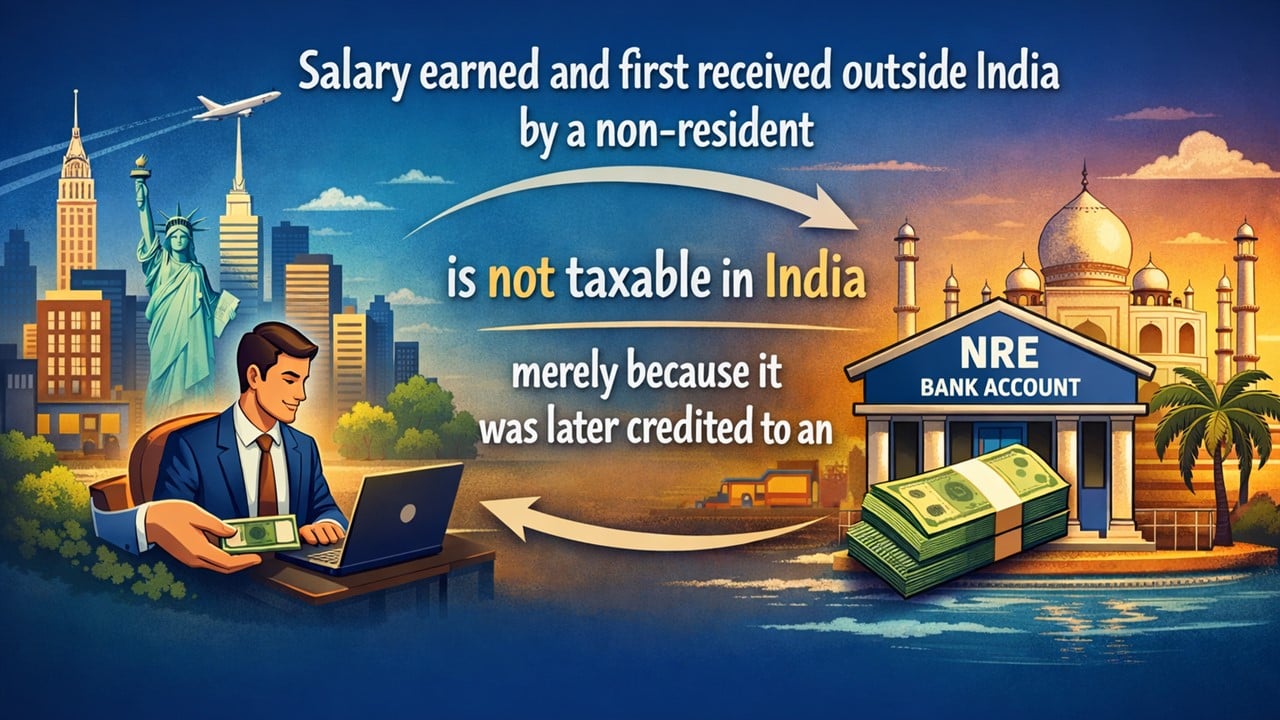

ITAT held that salary earned and first received outside India by a non-resident is not taxable in India merely because it was later credited to an NRE bank account.

ITAT Deletes Rs. 44.24 Lakh Addition on Foreign Salary

Foreign Salary of Non-Resident Not Taxable in India Merely Due to NRE Account Credit: ITAT

Kaushal Ganpatbhai Patel, a non-resident, has filed the present appeal in the Income Tax Appellate Tribunal (ITAT) Ahmedabad, challenging an order dated December 03, 2024, passed by the Income Tax Authorities, Assessing Officer (AO) under Section 147/144C(13) of the Income Tax Act, 1961, adhering to the directions of the Dispute Resolution Panel (DRP). The case is related to the Assessment Year (AY) 2019-20.

Through the impugned order, an additional amount of Rs. 44.24 lakh was levied on the assessee's income on the ground of alleged undisclosed salary income received by the applicant in his bank account with an Indian branch. The salary income relating to the service rendered outside India is not taxable in India. Further additions were imposed on the grounds of alleged unexplained investment by purchasing foreign currency of Rs. 42.81 lakh and an unexplained money receipt of about Rs. 1 crore.

The key dispute in the present case is whether salary earned outside India by a non-resident becomes taxable in India merely because it was credited to an NRE bank account in India. The assessee argued that he is a non-resident who is employed in a company named Seychelles, from where he earned the salary for services rendered outside India. The assessee further claimed that his income was earned outside of India and was just transferred to the NRE account in India, which was a later movement, not the initial fresh receipt in India. To support his claim, he also cited earlier judgements of the High Court and ITAT concerning a similar issue.

When the tribunal heard the arguments of the assessee, it asserted that “receipt of income” refers to the first time the person gets control over the money. The ITAT agreed with the assessee and ruled that income earned and accrued outside India is considered received outside India when the employee first becomes entitled to it. Just depositing the amount in an NRE account later does not make it liable to be taxed in India under Section 5(2)(a). In conclusion, the tribunal deleted the addition of Rs. 44.24 lakh. Since the other additions were also linked to the disputed key of salary income, the Tribunal also deleted them and allowed the assessee's appeal in full.

About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2490

2490My Recent Articles

- ITAT Remands TDS Appeal After CIT(A) Failed to Decide Actual CAM Charges IssuePremium

- ITAT Rules in Taxpayer's Favour, Holds Delay in Filing Form 67 Cannot Be Sole Ground to Deny Foreign Tax CreditPremium

- ITAT Revives Tax Appeals for Six AYs After Finding Insufficient Hearing Time and Ignored Adjournment RequestPremium

- ITAT Grants Fresh Opportunity to Explain Rs 2.39 Crore Demonetisation Cash Deposit Addition After Main Director’s DeathPremium

- ITAT Grants Taxpayer Fresh Opportunity to Contest Rs 44.16 Lakh Addition After Finding No Decision on MeritsPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts