GST Impact in case of death of Proprietor

GST Impact in case of death of Proprietor In the case of Death of Proprietor, what are the two options available with Legal Heir? Legal Heir may choo…

Table of Contents

GST Impact in case of death of Proprietor

In the case of Death of Proprietor, what are the two options available with Legal Heir?

- Legal Heir may choose to close the business,

- Or Run the Bussiness in his name

Actions to be taken in case of Closure of Bussiness

- First, you need to check that all GST Returns should be filed by Legal Heir

- In case GST Log-in credential is not available, then the legal heir needs to visit www.gst.gov.in and go to the tab Search as a taxpayer. There you would need to key in the GSTIN and you will get the details of the jurisdiction and also the filing status.

Arrange for the following Documents:

1. Death Certificate / Succession Certificate 2. Identity Proof of the deceased 3. Identity Proof of the legal heir which will prove the relationship status with the deceased 4. GST Certificate of the deceased 5. Return filing status ( as presented above)- Once the above documents are arranged the legal heir can visit the Proper Officer for the change of the authorized signatory.

- On verification of the same, the Proper Officer will change the authorized signatory and send a temporary link for updation of details.

- Once the signatory has been changed then the process of cancellation of registration can be initiated.

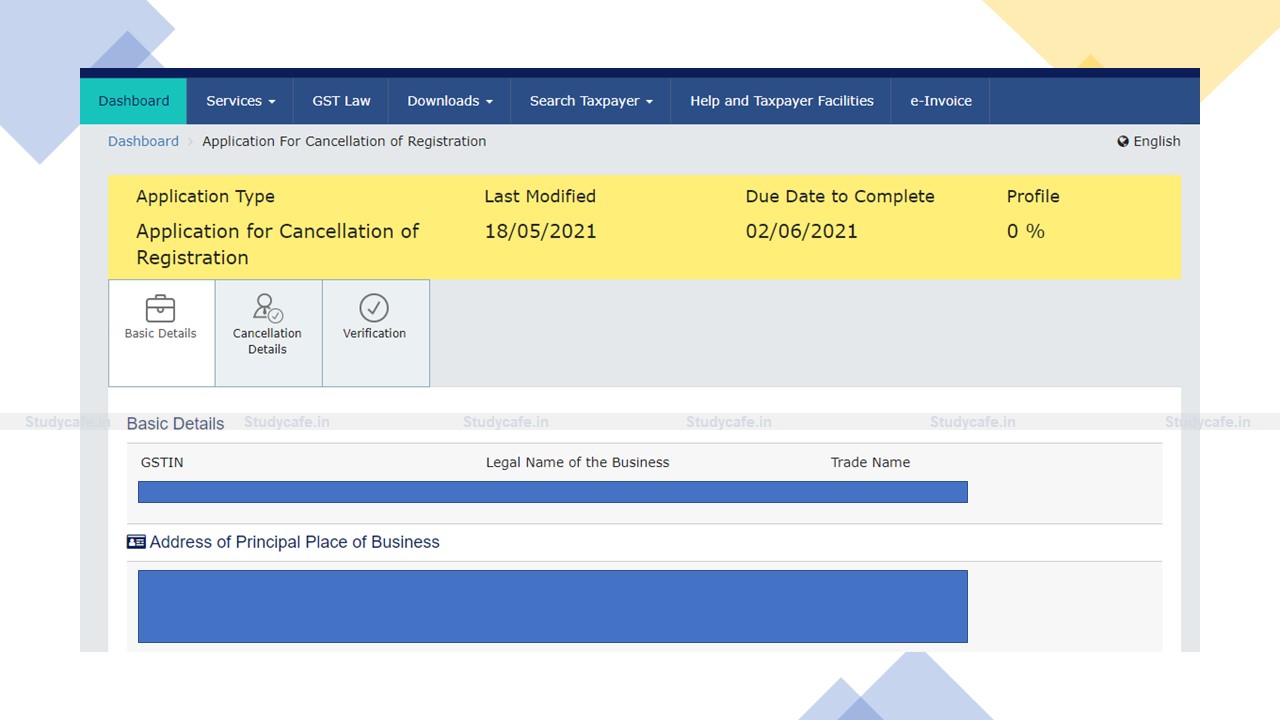

Filling Cancellation Application

- First you need to file all the pending returns

- The legal heir is required to apply for cancellation, citing reasons for cancellation

Procedure for cancellation

Section 29

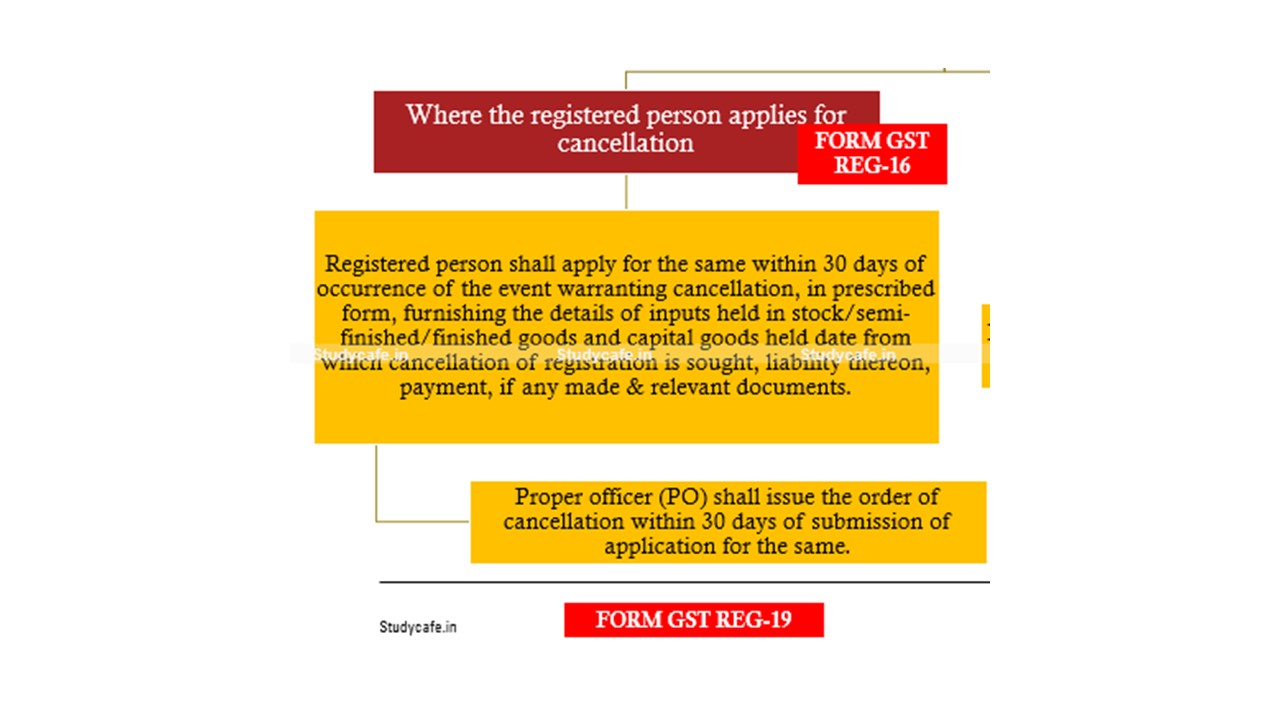

The proper officer on an application filed by the registered person or by his legal heirs, in case of death of such person, cancel the registration.Rule 20

The Application will be made in Form GST REG-16 within a period of thirty days of the occurrence of the event warranting the cancellation.

Rule 22

Proper officer (PO) shall issue the order of cancellation within 30 days of submission of application for the same in GST REG-19What are the Documents to be attached with the application?

1. Death Certificate 2. Identity Proof of the deceased 3. Details of Stock held of the date of death 4. GST Certificate of the deceased 5. Return filing status ( as presented above) 6. Address proof of deceased 7. Bank Account Closure Certificate 8. Indemnity CertificateHow to reverse ITC in case of Cancellation of Registration?

Rule 44- Manner of reversal of credit under special circumstances

The amount of input tax credit [ITC] relating to inputs held in stock, inputs contained in semi-finished and finished goods held in stock, and capital goods held in stock shall be reversed. (a) for inputs [stock, semi-finished and finished goods] the ITC [input tax credit] shall be calculated proportionately on the basis of the corresponding invoices on which credit had been availed by the registered taxable person on such inputs; (b) for capital goods held in stock, Reversal of the input tax credit involved in the remaining useful life in months shall be computed on a pro-rata basis, taking the useful life as five years or Tax on Sale Value whichever is high Illustration: Capital goods have been in use for 4 years, 6 month and 15 days. Purchase cost Rs. 10,00,000. GST availed 180,000. Sale value at time of disposal, 100,000. GST 18000 The useful remaining life in months = 5 months ignoring a part of the month The input tax credit is taken on such capital goods = 180,000. Input tax credit attributable to remaining useful life = 180,000*5/60 = 15000 In this case Tax of Rs. 18000 to be paid. Illustration: Suppose, sale value at the time of disposal, 50,000. GST 9000 In this case Tax of Rs. 15000 to be paid.How to make payment of GST in case of death of Proprietor?

Where a person, liable to pay tax, interest or penalty under this Act, dies, then the legal representative shall be liable to pay, out of the estate of the deceased, to the extent to which the estate is capable of meeting the charge, the tax, interest or penalty due from such person under this Act, whether such tax, interest or penalty has been determined before his death but has remained unpaid or is determined after his death.Whether refund of remaining ITC after making payment of all the liabilities of Deceased can be claimed?

Refund of ITC as per section 54 cannot be claimed.Whether refund of remaining cash balance after making payment of all the liabilities of Deceased can be claimed?

Refund of remaining cash balance after making payment can be claimed.Can I make a taxable supply after making a cancellation application?

Where an application for cancellation of registration has been made, the registration shall be deemed to be suspended from the date of submission of the application or the date from which the cancellation is sought, whichever is later, pending the completion of proceedings for cancellation of registration under rule 22. During that time:- you don't need to file GST Returns

- you cannot make taxable supply

Do I need to file any return once the cancellation order is received?

Once the cancellation order is received, the legal heir is required to file the final return which is GSTR 10 electronically through the common portal.What if Final Return is not filed within the Stipulated time?

Assessment of non-filers of returns under section 62 can take place when Final Return is not filed within Stipulated time.What if Legal Heir receives Show cause notice on behalf of Deceased Person?

Where SCN has received by Legal Heir on behalf of Deceased Person- u/s 73 [Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized for any reason other than fraud or any wilful misstatement or suppression of facts] or

- or u/s 74 [Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized by reason of fraud or any wilful-misstatement or suppression of facts.]

Actions to be taken in case Legal heir decides to continue with the business

Where a business carried on by a taxable person registered under this Act is transferred on account of death, the transferee or the successor, as the case may be, shall be liable to be registered with effect from the date of such transfer or succession. The Registration should be obtained within 30 days of the event in GST-REG-1 Documents required for applying for Registration as sole proprietor:- Owner’s PAN Card

- Owner’s Aadhar Card

- Owner’s Photograph

- Proof of Address

- Bank Account Details

Transfer of ITC in case of death of the sole proprietor

In terms of Section 18 of the CGST Act, the input tax credit which remains unutilized in the electronic credit ledger of a deceased person can be transferred by filing on the common portal Form GST ITC-02. As soon as the legal heir file the ITC 02 electronically with a request to transfer the unutilized ITC lying in the electronic credit ledger of the deceased along with the CA certificate, it will be transferred to the registration number of the legal heir. The transferee being the same person , the legal heir needs to log in to his GSTIN and accept the details so furnished from the transferor’s GSTIN and upon such acceptance the unutilised ITC transferred through ITC 02 will be credited in the credit ledger of the new registered personWhether refund of remaining cash balance after making payment of all the liabilities of Deceased can be claimed?

Refund of remaining cash balance after making payment can be claimed.Procedure for cancellation

Section 29

The proper officer on an application filed by the registered person or by his legal heirs, in case of death of such person, cancel the registration.Rule 20

The Application will be made in Form GST REG-16 within a period of thirty days of the occurrence of the event warranting the cancellation.Rule 22

Proper officer (PO) shall issue the order of cancellation within 30 days of submission of application for the same in GST REG-19Can I make a taxable supply after making a cancellation application?

Where an application for cancellation of registration has been made, the registration shall be deemed to be suspended from the date of submission of the application or the date from which the cancellation is sought, whichever is later, pending the completion of proceedings for cancellation of registration under rule 22. During that time:- you don't need to file GST Returns

- you cannot make taxable supply

Do I need to file any return once the cancellation order is received?

Once the cancellation order is received, the legal heir is required to file the final return which is GSTR 10 electronically through the common portal.What if Final Return is not filed within the Stipulated time?

Assessment of non-filers of returns under section 62 can take place when Final Return is not filed within Stipulated time.What if Legal Heir receives Show cause notice on behalf of Deceased Person?

Where SCN has received by Legal Heir on behalf of Deceased Person- u/s 73 [Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized for any reason other than fraud or any wilful misstatement or suppression of facts] or

- or u/s 74 [Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized by reason of fraud or any wilful-misstatement or suppression of facts.]

About Author

ARUP DASGUPTA

PRINCIPAL CONSULTANT

Arup is a hardcore Compliance professional with deep interest in tax litigations and advisories to foreign companies from ( Germany, Italy, China, etc) setting up their business in India and is based in City of Joy, India.

He is qualified Chartered Accountant from ICAI in the year 2000, Company Secretary from ICSI in the same year and CISA from ISACA, US in the year 2010. He has also earned a Diploma in IFRS from ACCA, Uk.

Arup is a hardcore Compliance professional with deep interest in tax litigations and advisories to foreign companies from ( Germany, Italy, China, etc) setting up their business in India and is based in City of Joy, India.

He is qualified Chartered Accountant from ICAI in the year 2000, Company Secretary from ICSI in the same year and CISA from ISACA, US in the year 2010. He has also earned a Diploma in IFRS from ACCA, Uk.

ARUP DASGUPTA

ARUP DASGUPTA KOLKATA, West Bengal, India

KOLKATA, West Bengal, India 1

1Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.