GST rate of 18% Applicable on baby Wipes: AAR

GST rate of 18% Applicable on baby Wipes: AAR The Applicant is a Private Limited Company, registered under the provisions of Central Goods and Servic…

Table of Contents

GST rate of 18% Applicable on baby Wipes: AAR

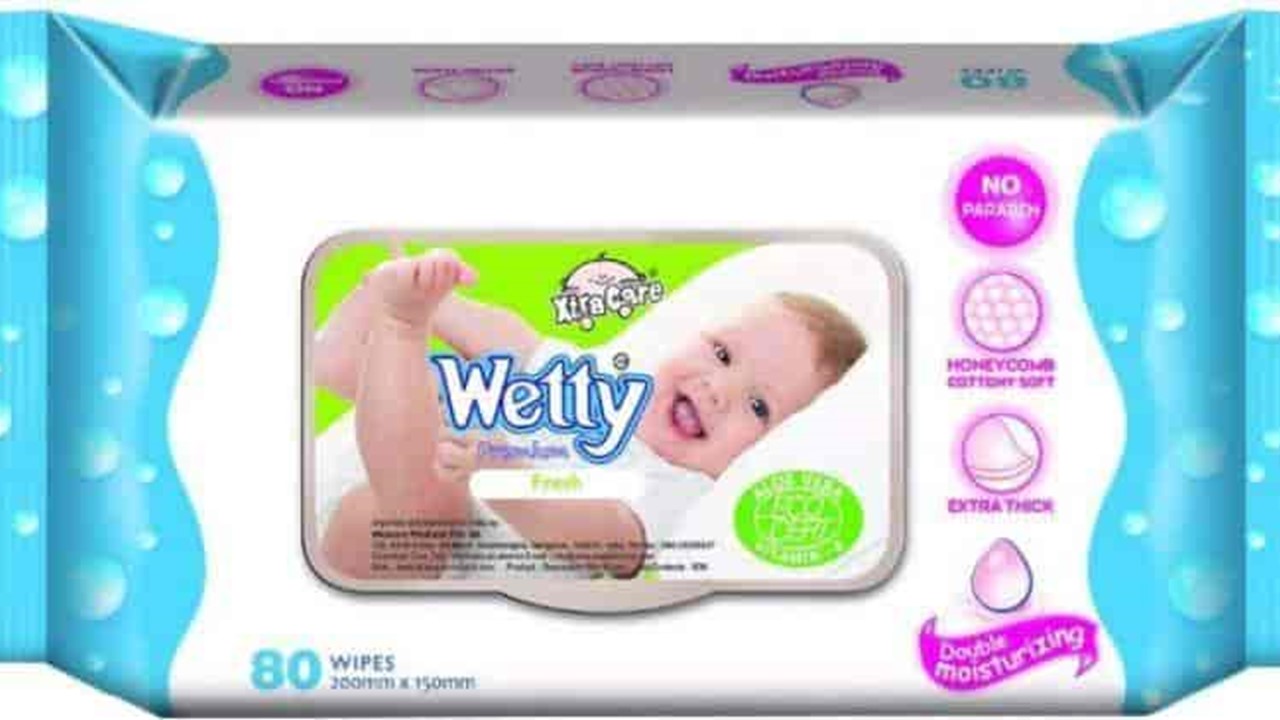

The Applicant is a Private Limited Company, registered under the provisions of Central Goods and Services Tax Act, 2017 as well as Karnataka Goods and Services Tax Act, 2017 (hereinafter referred to as the CGST Act and KGST Act respectively), engaged in Import and trading of baby wipes. A dispute on the classification of baby wipes has been settled by the order of Commissioner of Customs (Appeals-II), Chennai as per which the classification of baby wipes is 96190010. The applicant has been classifying the baby wipes under the heading 9619 0010 and discharging the duty accordingly. Meanwhile, a Circular bearing No. 52/26/2018-GST dated 09.08.2018 was issued by CBIC, which dealt with the classification of wipes manufactured using spun lace non-woven fabric and also dealt with HSN codes 3307, 3401, and 5603 and the applicant, on the basis of the said circular & taking cautious view is charging 18% GST from August 2018.

Clarification Sought

a. What is the HSN Code of baby wipes/ classification? b. What is the rate of tax to be levied on baby wipes? c. If Circular No. 52/ 26/ 2018 GST-dated 9th August 2018, is not applicable to the applicant, whether the applicant can go back and charge GST @12% since there exists ambiguity in this regard.Ruling

a. The "baby wipes" merits classification under heading 3307 b. The applicable rate of tax (GST) on baby wipes is 18% c. The Circular No. 52/26/2018 GST-dated 9th August 2018, is applicable to the applicant.About Author

CA Deepak Gupta

Co Founder

CA Deepak Gupta,is Co-founder of Studycafe. He is Microsoft Office Specialist and Corporate Trainer of AI Tools, Microsoft Excel.

He is Finance Influencer having more than 250K followers on Social Media. CA Deepak Gupta, is Having more than 14 plus years of experience, and he has Worked with best brands Like, Hero, Wipro, Ericsson before Starting Studycafe. He has Trained more than 20000 Persons in Microsoft Excel, PowerPoint, Power BI, Google Sheet, Google Forms and Other Tools.

CA Deepak Gupta,is Co-founder of Studycafe. He is Microsoft Office Specialist and Corporate Trainer of AI Tools, Microsoft Excel.

He is Finance Influencer having more than 250K followers on Social Media. CA Deepak Gupta, is Having more than 14 plus years of experience, and he has Worked with best brands Like, Hero, Wipro, Ericsson before Starting Studycafe. He has Trained more than 20000 Persons in Microsoft Excel, PowerPoint, Power BI, Google Sheet, Google Forms and Other Tools.

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 3423

3423My Recent Articles

- UltraTech Cement slapped with Rs. 808.78 Cr Income Tax Demand

- GST: High Court upheld constitutional validity of Section 16(2)(c), asks government to address ITC issues of genuine purchasers

- Old vs New Tax Regime for Tax Year 2026-27

- High court criticizes Income Tax Department for not releasing ITR Utilities despite 11 years of directions

- Fino Payments Bank CEO Rishi Gupta Gets Bail in GST Case, Bank Clarifies No Direct Link

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts