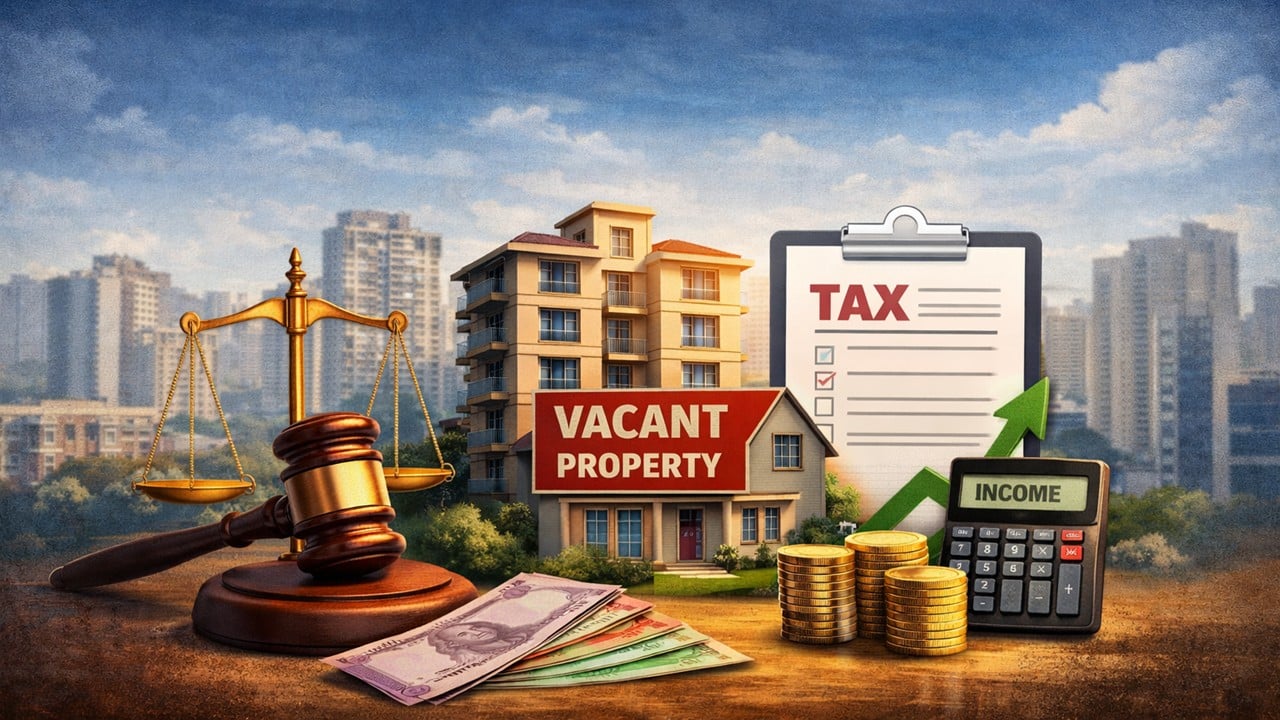

HC Rules Rental Income from Unsold Inventory Taxable as 'Income from House Property':

HC ruled that real estate developers must tax rental income from unsold stock as House Property income, not Business Income.

Letting of unsold property treated as ownership income, not business activity

The appellant, Ambalal Sarabhai Enterprises Limited, challenged the judgment of the ITAT which had classified its rental income as "Business Income" instead of "Income from House Property" for the Assessment Year 2013-14. The appellant, engaged in real estate development, had leased out certain portions of its unsold inventory (commercial space) while awaiting sale. The appellant argued that as the owner of the property, the income derived from letting it out should be taxed under the head "Income from House Property," regardless of its business objectives.

The Revenue, however, contended that since the company's main object was real estate business and the property was held as "stock-in-trade," the rental income was incidental to its business and should be taxed as "Profits and Gains of Business or Profession."Issue Raised: Whether the rental income derived from leasing out unsold commercial space held as stock-in-trade by a real estate developer is taxable under the head "Income from House Property" or "Profits and Gains of Business or Profession."

HC Ruling: The High Court, Bench allowed the appeal in favor of the assessee. Relying on the Supreme Court precedents in Raj Dadarkar & Associates and Rayala Corporation (P) Ltd., the Court held that the character of the income is determined by the nature of the activity.The Court observed that unless the property is used as a "tool of the business" (like a hotel or warehouse), the mere fact that the owner is a company or holds the property as stock-in-trade does not change the head of income. Since the appellant was simply earning rent from the ownership of the premises, the Court ruled the income must be assessed under "Income from House Property," allowing the statutory deductions associated with that head.

To Read Full Judgment, Download PDF Given BelowAbout Author

Meetu Kumari

Content Manager

Studycafe

Studycafe Jodhpur, Rajasthan, India

Jodhpur, Rajasthan, India 2264

2264My Recent Articles

- ITAT Condones 302-Day Delay, Restores Salary Assessment for Fresh VerificationPremium

- ITAT Condones Delay After Tax Consultant's Death, Restores Appeals for Fresh HearingPremium

- ITAT Remands Salary Addition, Says Taxability Depends on Salary Becoming Due, Not Mere ReceiptPremium

- ITAT Deletes TP Royalty Adjustment, Orders Fresh Review of Commission BenchmarkingPremium

- ITAT Quashes Reassessment Over Unsigned Section 148 Notice Issued to AssesseePremium

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts