ITAT Holds Amortisation Circular Optional, Not Mandatory for Assessee:

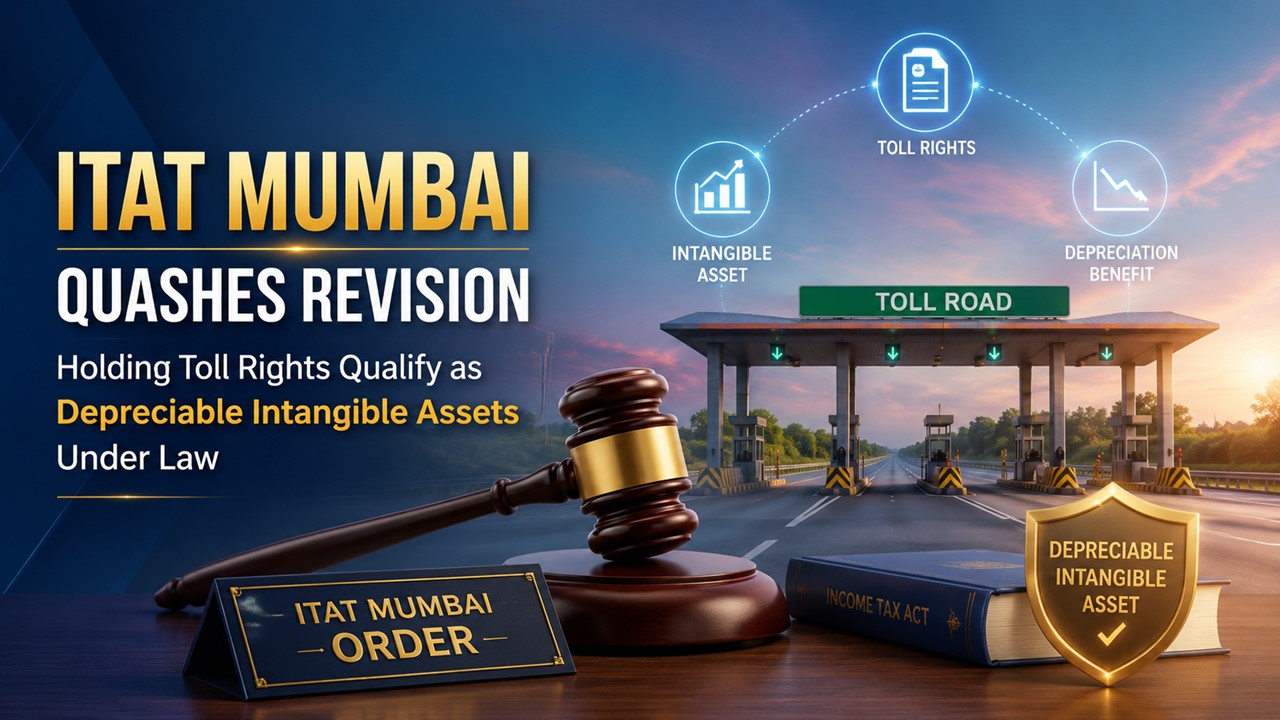

ITAT quashes revision, holding toll rights qualify as depreciable intangible assets under law.

Audit Objection Alone Cannot Justify Revisionary Proceedings Under Law

The Mumbai Bench of the Income Tax Appellate Tribunal (ITAT) held that revisionary proceedings under Section 263 of the Income Tax Act, 1961, cannot be invoked merely because the Principal Commissioner of Income Tax prefers a different view from that adopted by the Assessing Officer, especially where detailed enquiries were conducted during the scrutiny assessment. A Bench comprising Judicial Member Amit Shukla and Accountant Member Girish Agrawal quashed the revision order passed against Hampi Expressways Pvt. Ltd. for AY 2022-23.

The assessee, engaged in developing and operating a national highway project under a concession agreement with the National Highways Authority of India (NHAI), filed its return declaring a loss of Rs 25.76 crore. The case was selected for complete scrutiny on issues including investment in intangible assets and the claim of depreciation. During assessment proceedings, the Assessing Officer called for detailed information, examined the concession agreement, depreciation claim and supporting documents, and ultimately accepted the returned income.

Before the Tribunal, the assessee contended that the Assessing Officer had examined the issue in detail during scrutiny and consciously accepted the claim. It was further argued that the right to operate the highway and collect toll constituted a licence or business/commercial right eligible for depreciation under Section 32(1)(ii) and that the CBDT Circular merely provided an alternative method of claiming deduction through amortisation.

“The benefit of the Circular cannot be thrust upon the assessee, if it is not claimed.” The Tribunal noted that the assessment was selected for scrutiny specifically on the issue of intangible assets and depreciation. It observed that detailed notices were issued and comprehensive replies were furnished by the assessee, demonstrating that the Assessing Officer had conducted adequate enquiries before accepting the claim.

The Bench further held that the rights acquired under the concession agreement were in the nature of a licence and constituted an intangible asset eligible for depreciation under Section 32(1)(ii). It observed that the assessee had capitalised the expenditure and claimed depreciation consistently, while the CBDT Circular merely provided an optional mechanism of amortisation.

“The right granted to the assessee under the concession agreement to operate the project facility and collect toll charges is a license or akin to license, hence, being an intangible asset is eligible for depreciation under section 32(1)(ii) of the Act.”

The Bench additionally noted that the revision proceedings originated from an audit objection and reiterated that revisionary jurisdiction cannot be exercised merely on the basis of audit objections without independent application of mind by the Principal Commissioner.

Thus, the ITAT held that the twin conditions required under Section 263, namely, that the assessment order must be both erroneous and prejudicial to the interests of the Revenue, were not satisfied. The revision order was quashed, and the assessee’s appeal was allowed.

To Read Full Order, Download PDF Given Below.

About Author

Meetu Kumari

Content Manager

Studycafe

Studycafe Jodhpur, Rajasthan, India

Jodhpur, Rajasthan, India 2235

2235My Recent Articles

- ITAT Allows Section 54F Relief Without Completion Certificate for New House ConstructionPremium

- HC Sets Aside GST Registration Revocation Rejection Over Procedural Lapse.Premium

- ITAT Upholds Deletion of Bogus Purchase Additions Lacking Search EvidencePremium

- High Court Refuses GST Writ, Directs Appeal Against Fake ITC DemandPremium

- ITAT Restricts Bogus Purchase Addition to 1.15% Profit Element Despite Seller DenialsPremium

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts