How to determine fair value hedge or cash flow hedge under Ind AS 109

How to determine fair value hedge or cash flow hedge under Ind AS 109 Hedge accounting as covered under Para 6 of Ind AS 109 needs to determ

How to determine fair value hedge or cash flow hedge under Ind AS 109

Hedge accounting as covered under Para 6 of Ind AS 109 needs to determine the TYPE of hedge relationship that an entity is dealing with because the typeof hedge determines accounting entries. If incorrectly identified the type of the hedge, then accounting will be totally wrong.

All types ofhedges are defined in Ind AS 109, understanding the differences and distinguishing one type from the other one requires thorough understanding

Types of hedges

There are three types of hedge explained in para 6.5.2

1.Fair Value Hedge;

2. Cash Flow Hedge, and

3. Hedge of a Net Investment in a Foreign Operation similar to cash flow hedge.

Fair Value Hedge

Para 6.5.2 (a) says a hedge of the exposure to changes in fair value of a recognised asset or liability or an unrecognised firm commitment, or a component of any such item, that is attributable to a particular risk and could affect profit or loss

In short there is some fixed return instrumentand we are worried that its value may fluctuate with the market.

What is a Cash Flow Hedge

Para 6.5.2 (a) says Cash flow hedgeis a hedge of the exposure tovariability in cash flowsthat is attributable to a particular risk associated with all or a component of a recognized asset or liability or a highly probable forecast transaction, and could affect profit or loss.

In short there is some variable return financial instrument and we might get less money or have to pay more money in the future than now.

Equally, there can be a highly probable forecast transaction that hasnt been recognized in accounts yet.

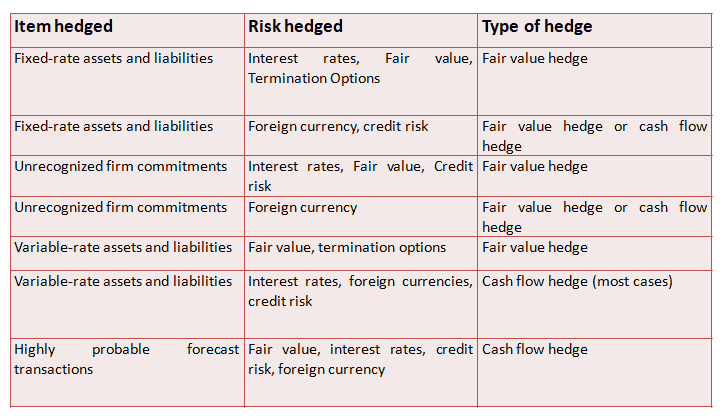

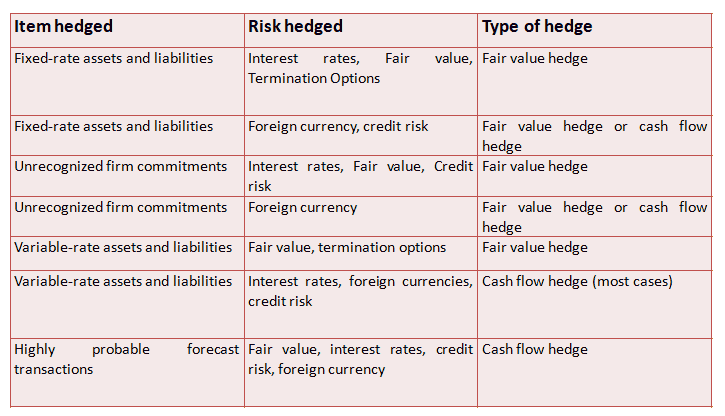

How to Distinguish Fair Value Hedge and Cash Flow Hedge

Distinguishment Depends on what kind of item are we hedging. We can hedge a fixed return FI or a variable return FI.

Hedging a Fixed return Financial Instrument

A fixed return financial instrument means that the item has a fixed value in your accounts and it may repay or return fixed amount of cash in the future.

The same applies forunrecognized firm commitmentsthat have not been accounted in your accounts yet, but they will be in the future.

And when it comes to hedging fixed return financial instruments, and then were dealing with the fair value hedge.

Justification: We think that in the future, we would be paying or receiving a different amount than the fair value of the instrument will be and we dont want to FIX the amount, we dont wish a different carrying amount in books and account exactly what market value is.

Fair Value Hedge Example

Entity issued some bonds with interest 10% p.a.

Entity knows what they have to pay in future, however thay may think, market interest rate will be much lower than 10% and will end up paying higher interest.

Therefore, thay enter into interest rate swap to receive 10% fixed / pay MIBOR + 0.25% lets say. This is a fair value hedge they hedged the fair value of your interest payments to market rates.

Hedging a Variable return financial instrument

A variable return financial instrument means that the expected future cash flows from this instrument changes as a result of risk exposure, for example, variable interest rates or foreign currencies fluctuation.

When it comes to hedging variable items, were dealing with cash flow hedge.

Justification: Entity may think that they may end up paying or receiving different amount of money in certain currency in the future that you would get now.

In a cash flow hedge, we wish to FIX the amount of money to be received or to be repaid so that this amount would be the same as NOW and IN THE FUTURE. Ie. amount should be known

Cash Flow Hedge Example

Entity issued some bonds with coupon MIBOR +0.25%.

It means that in the future, Entity will pay interest in line with the market, because MIBOR reflects the market conditions and entity doesnt want to pay in line with market. Entity wish to know how much they will pay in the future, as they dont wish to carry risk of fluctuation.

Therefore they enter into interest rate swap to receive MIBOR + 0.25% / pay 10% fixed. This is cash flow hedge entity has fixed cash flows and will always pay 10%.

How to Account for a Fair Value Hedge

Para 6.5.8 specifies As long as a fair value hedge meets the qualifying criteria in paragraph 6.4.1, the hedging relationship shall be accounted for as follows:(a) the gain or loss on the hedging instrument shall be recognised in profit or loss (or other comprehensive income, if the hedging instrument hedges an equity instrument for which anentity has elected to present changes in fair value in other comprehensive income in accordance with paragraph 5.7.5).

(b) the hedging gain or loss on the hedged item shall adjust the carrying amount of the hedged item (if applicable) and be recognised in profit or loss. If the hedged item is a financial asset (or a component thereof) that is measured at fair value through other comprehensive income in accordance with paragraph 4.1.2A, the hedging gain or loss on the hedged item shall be recognised in profit or loss. However, if the hedged item is an equity instrument for which an entity has elected to present changes in fair value in other comprehensive income in accordance with paragraph 5.7.5, those amounts shall remain in other comprehensive income. When a hedged item is an unrecognised firm commitment (or a component thereof), the cumulative change in the fair value of the hedged item subsequent to its designation is recognised as an asset or a liability with a corresponding gain or loss recognised in profit or loss.

This can be explained in summarized pattern as under

Step 1: Determine the fair value of both your hedged item and hedging instrument at the reporting date;

Step 2: Recognize any change in fair value (gain or loss) on the hedging instrument in profit or loss.

Step 3: Recognize the hedging gain or loss on the hedged item in its carrying amount.

Accounting entries for a fair value hedge:

How to Account for a Cash Flow Hedge

Para 6.5.11 specifies that As long as a cash flow hedge meets the qualifying criteria in paragraph 6.4.1, the hedging relationship shall be accounted for as follows:

(a) the separate component of equity associated with the hedged item (cash flow hedge reserve) is adjusted to the lower of the following (in absolute amounts):

(i) the cumulative gain or loss on the hedging instrument from inception of the hedge; and

(ii) the cumulative change in fair value (present value) of the hedged item (ie the present value of the cumulative change in the hedged expected future cash flows) from inception of the hedge.

(b) the portion of the gain or loss on the hedging instrument that is determined to be an effective hedge (ie the portion that is offset by the change in the cash flow hedge reserve calculated in accordance with (a)) shall be recognised in other comprehensive income.

(c) any remaining gain or loss on the hedging instrument (or any gain or loss required to balance the change in the cash flow hedge reserve calculated in accordance with (a)) is hedge

To summarise we may say that

Step 1: Determine the gain or loss on your hedging instrument and hedge item at the reporting date;

Step 2: Calculate the effective and ineffective portions of the gain or loss on the hedging instrument;

Step 3: Recognize the effective portion of the gain or loss on the hedging instrument in other comprehensive income (OCI). This item in OCI will be called Cash flow hedge reserve in OCI.

Step 4: Recognize the ineffective portion of the gain or loss on the hedging instrument in profit or loss.

Accounting entries for a cash flow hedge:

Summary

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.