ICAI issues Concept Paper on Estimating Discount Rates in Valuation brought out by ICAI and ICAI RVO

ICAI issues Concept Paper on Estimating Discount Rates in Valuation brought out by ICAI and ICAI RVO 1. Introduction Discount rate used in valuation …

Table of Contents

ICAI issues Concept Paper on Estimating Discount Rates in Valuation brought out by ICAI and ICAI RVO

Income approach is considered as one of the most appropriate approach under-going concern as it determines the intrinsic value of an asset by estimating the present value of future earnings of assets. Income Approach is also not as vulnerable to accounting conventions (like depreciation, inventory valuation) in comparison with the other techniques/ approaches since it is based on cash flows rather than accounting profits.

The Income Approach includes a number of methods, such as Discounted Cash Flow (DCF) Method, Relief from Royalty (RFR) Method, Multi-Period Excess Earnings Method (MEEM), With and Without Method (WWM) and Option pricing models such as Black-Scholes-Merton formula or binomial (lattice) model.

Discounted Cash Flow Method (DCF) is the most commonly used method in valuation and it arrives at a value by projecting the cash flows in the future and then discounting the cash flows back to the date of the valuation using the Discount Rate.

While discount rate is an important factor in valuation but at the same time estimating discount rate is difficult and also prone to judgement. Therefore, understanding the methodology and concepts in determining an appropriate discount rate is extremely critical for valuers.

Income approach is considered as one of the most appropriate approach under-going concern as it determines the intrinsic value of an asset by estimating the present value of future earnings of assets. Income Approach is also not as vulnerable to accounting conventions (like depreciation, inventory valuation) in comparison with the other techniques/ approaches since it is based on cash flows rather than accounting profits.

The Income Approach includes a number of methods, such as Discounted Cash Flow (DCF) Method, Relief from Royalty (RFR) Method, Multi-Period Excess Earnings Method (MEEM), With and Without Method (WWM) and Option pricing models such as Black-Scholes-Merton formula or binomial (lattice) model.

Discounted Cash Flow Method (DCF) is the most commonly used method in valuation and it arrives at a value by projecting the cash flows in the future and then discounting the cash flows back to the date of the valuation using the Discount Rate.

While discount rate is an important factor in valuation but at the same time estimating discount rate is difficult and also prone to judgement. Therefore, understanding the methodology and concepts in determining an appropriate discount rate is extremely critical for valuers.

The discount rate measures the risk associated with the investment, i.e., the danger of low returns that is different from the expected return on investment. It determines what should be the idle expected rate of return to compensate/reward for the danger or risk undertaken by an investor. This together with the risk-free market rate of return forms the Discount rate for Discounted Cash Flow method.

The discount rate measures the risk associated with the investment, i.e., the danger of low returns that is different from the expected return on investment. It determines what should be the idle expected rate of return to compensate/reward for the danger or risk undertaken by an investor. This together with the risk-free market rate of return forms the Discount rate for Discounted Cash Flow method.

Hence for calculating Equity Value using Free Cash Flow to Equity, we use Cost of Equity (COE) as discount rate while for calculating Enterprise Value using Free Cash Flow to Firm approach, Weighted Average Cost of Capital (WACC) is used to discount the future cash flows. Of course, to both the COE and WACC, suitable premiums or discounts may be adjusted to arrive at the discount rate based on the factors such as liquidity, control, size, specific risks etc.

Hence for calculating Equity Value using Free Cash Flow to Equity, we use Cost of Equity (COE) as discount rate while for calculating Enterprise Value using Free Cash Flow to Firm approach, Weighted Average Cost of Capital (WACC) is used to discount the future cash flows. Of course, to both the COE and WACC, suitable premiums or discounts may be adjusted to arrive at the discount rate based on the factors such as liquidity, control, size, specific risks etc.

1. Introduction

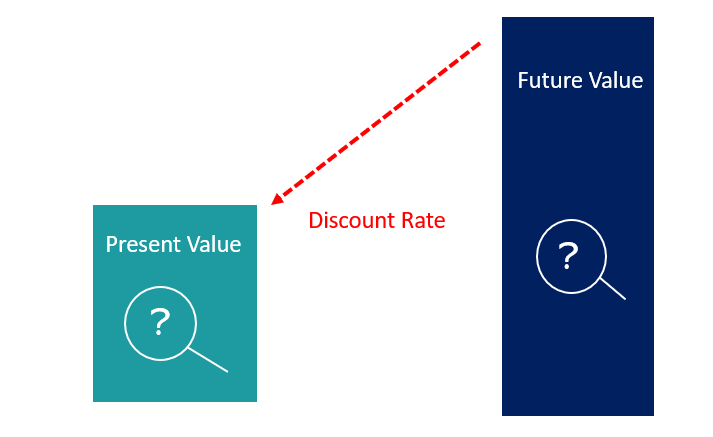

Discount rate used in valuation reflects the riskiness of the asset and is one of the critical inputs of Discounted Cash Flow method. ICAI Valuation Standards 2018 defines “Discount Rate” as the return expected by a market participant from a particular investment and shall reflect not only the time value of money but also the risk inherent in the asset being valued as well as the risk inherent in achieving the future cash flows. ICAI Valuation Standards recognize the following three approaches in valuation and they are globally accepted approaches as well: - 1) Market Approach 2) Income Approach 3) Cost Approach

Income approach is considered as one of the most appropriate approach under-going concern as it determines the intrinsic value of an asset by estimating the present value of future earnings of assets. Income Approach is also not as vulnerable to accounting conventions (like depreciation, inventory valuation) in comparison with the other techniques/ approaches since it is based on cash flows rather than accounting profits.

The Income Approach includes a number of methods, such as Discounted Cash Flow (DCF) Method, Relief from Royalty (RFR) Method, Multi-Period Excess Earnings Method (MEEM), With and Without Method (WWM) and Option pricing models such as Black-Scholes-Merton formula or binomial (lattice) model.

Discounted Cash Flow Method (DCF) is the most commonly used method in valuation and it arrives at a value by projecting the cash flows in the future and then discounting the cash flows back to the date of the valuation using the Discount Rate.

While discount rate is an important factor in valuation but at the same time estimating discount rate is difficult and also prone to judgement. Therefore, understanding the methodology and concepts in determining an appropriate discount rate is extremely critical for valuers.

2. Discount Rate & Relationship between Risk and Return

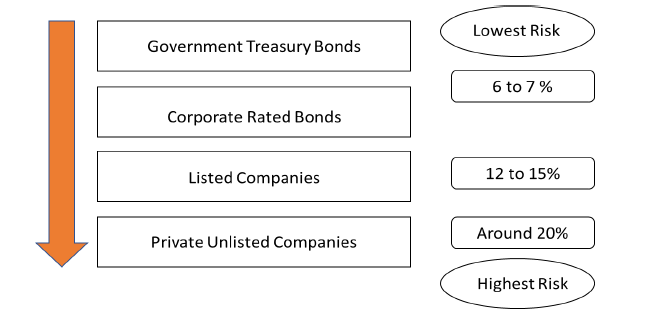

Discount Rate is the return expected by a market participant from a particular investment and shall reflect not only the time value of money but also the risk inherent in the asset being valued as well as the risk inherent in achieving the future cash flows. An Investor expects to be compensated for both risk and the time value of money which together forms the expected return on investment. An investor selects between different investments options on the basis of the assessment and comparison of the risk involved and the expected rate of return from each investment option. Theoretically, the time value of money on an investment without any risk is normally represented by a risk-free rate of return but hardly any investment is completely risk-free. Hence there is always a need to compensate the investor for the higher level of risk by giving a higher rate of return. The fundamental relationship between risk and return is “Higher the risk associated with an investment higher is the expected return from it” and this is what drives an Investors decision. The diagram hereunder clearly depicts how an expected rate of return varies basis the risk involved in the asset (the percent range given below is only an example).

The discount rate measures the risk associated with the investment, i.e., the danger of low returns that is different from the expected return on investment. It determines what should be the idle expected rate of return to compensate/reward for the danger or risk undertaken by an investor. This together with the risk-free market rate of return forms the Discount rate for Discounted Cash Flow method.

3. Types of Discount Rates

Following are the commonly used Discount Rates in Discounted Cash Flow Method:- i) The Cost of Equity (“COE”) – It reflects the return expected by the equity shareholders, to compensate for the risk assumed through their investment in the business. ii) The Weighted Average Cost of Capital (“WACC”) – It is based on the proportionate weights of each component of the source of capital, i.e., weighted average of COE and COD wherein the ratio of Equity/Debt on total capital is the proportionate weights. WACC constitutes all capital sources:- Equity shares

- Preference shares

- Long term debts

- Short term debts

= Free Cash Flow to the Firm (FCFF)/ Weighted Average Cost of Capital

= (Earnings Before Interest and Tax * (1-tax rate) + Depreciation/Non- Cash Expenditure – Capital Expenditure – Increase in Non-Cash Working Capital)/ WACC

ii) Equity Value: Equity Value is the value of the business attributable to equity shareholders after all expenses, reinvestments and debt obligations have been met by the company. Equity Value= Free Cash Flow to Equity (“FCFE”)/ Cost of Equity = (Net Income or Profit After Tax + Depreciation & Amortization – Capital Expenditure – Increase in Non Cash Working Capital + Change in Debt)/ Cost of Equity

Equity Value can be determined from Enterprise Value by eliminating following:

Add/(Less) : Adjustments Add : Cash & Cash Equivalents (to the extent it is in excess of routine business) Add : Fair Value of Surplus Assets including Land Add : Fair Value of Investments and Deposits Add : PV of MAT Credit (Less) : Fair Value of Contingent Liability (Less) : Fair Value of Long-Term Debt (Less) : Fair Value of Short-Term Debt (“Further adjustments would be required if there are preference shares and / or non-controlling interests are involved, which have not been considered in the above example”).As per ICAI Valuation Standards 2018 a valuer may consider the following factors while determining the discount rate:

i) type of asset being valued, example: debt, preference shares, business, real estate, intangibles, etc.; ii) life of the asset such as the risk-free rate used for determining the cost of equity in the CAPM model differs for an asset with a one-year life vs an indefinite life; iii) geographic location of the asset; iv) currency in which the projections have been prepared; v) type of cash flows; vi) risk in achieving the projected cash flows; vii) cash flows used for the projections as FCFE needs to be discounted by Cost of Equity whereas FCFF to be discounted using WACC; viii) discount the cash flows in the functional currency using a discount rate appropriate for that functional currency; and ix) pre-tax cash flows need to be discounted by pre-tax discount rate and post-tax cash flows to be discounted by post-tax discount rate; To Read More: Click HereAbout Author

Sushmita Goswami

Content Manager

Sushmita Goswami is a content writer with 2+ years of experience in Finance, Recruitment, Education and career Related Content. She is a Graduate from Delhi University in Journalism and Mass Communication

Studycafe

Studycafe  New Delhi , Delhi, India

New Delhi , Delhi, India 886

886My Recent Articles

- What to Consider When Choosing an Online Trading Platform?

- Post Office Franchise Scheme: Take Post Office Franchise at Rs 5000 and Earn Commission upto 20%; Check Details Here

- IAN invests INR 4.5 crore in Fintech NBFC Indium Finance

- UPI a Digital Public Good, No Charges in Consideration: Finance Ministry

- ITR Filing Penalty: Check Taxpayers Exempt from Paying a Late Fee even Missing the Deadline

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts