ICAI Releases Hand Book on GST Annual Return

ICAI Releases Hand Book on GST Annual Return Introduction GST is a value-added tax levied at all points in the supply chain, with credit for

ICAI Releases Hand Book on GST Annual Return

Introduction

GST is a value-added tax levied at all points in the supply chain, with credit for taxes paid on goods and/or services acquired for use in making the supply. It applies to both goods and services in a comprehensive manner. On a macro note, it may be said that GST is a mechanism which supports self-compliance wherein the assessees assess the taxes payable by them. To ensure the correctness and veracity of the reported information, annual return and GST audit are required. It becomes essential to have counter checks and balances to ensure that there is no seepage of exchequers revenue. GST principles embrace information technology and reduce the interaction with the tax administrators.

All entities having GST registration, except few specified categories of persons, are required to file GST annual return for every financial year irrespective of their turnover during the return filing period. Hence, even a dormant business that has obtained GST registration must file GST return.

Legal provisions of GST Annual Return

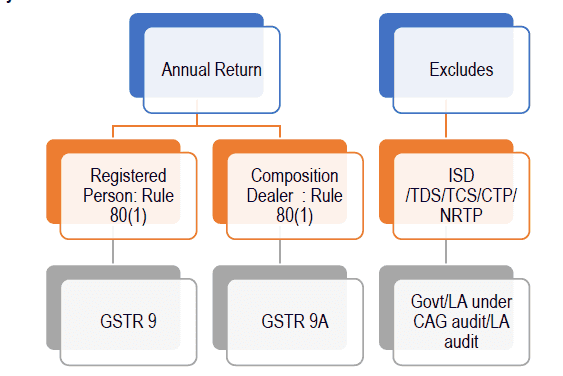

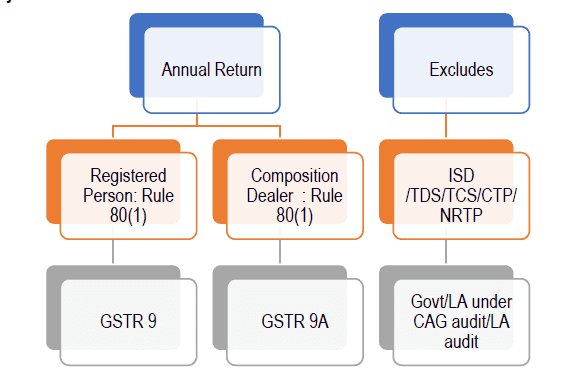

In order to understand the gamut of the GST Annual return and its requirement, it would be relevant for us to understand the legal provisions relevant for GST Annual Return. Two important provisions which are relevant and important in this context are Section 44(1) of CGST Act, 2017 and Rule 80(1) of the CGST Rules, 2017.

Section 44(1) requires that every registered person, other than an Input Service Distributor, a person paying tax under section 51 or section 52, a casual taxable person and a non-resident taxable person, shall furnish an annual return for every financial year electronically in such form and manner as may be prescribed on or before the thirty-first day of December following the end of such financial year. However, the due date for filing of annual return for the period 1st July, 2017 to 31st March, 2018 has first been extended to 31st March, 2019 and then to June 30, 2019 vide Removal of Difficulty Order No.01/2018-Central Tax dated 11th December, 2018 and 03/2018-Central Tax dated 31st December, 2018 respectively.

In terms of Rule 80(1) of the CGST Rules, 2017 Every registered person, other than an Input Service Distributor, a person paying tax under section 51 or section 52, a casual taxable person and a non-resident taxable person, shall furnish an annual return as specified under sub-section (1) of section 44 electronically in FORM GSTR-9 through the common portal either directly or through a Facilitation Centre notified by the Commissioner:

Provided that a person paying tax under section 10 shall furnish the annual return in FORM GSTR-9A.

The government vide Notification No. 39/2018 on 4th September 2018 notified the Annual return form GSTR 9/9A, which has been further amended by Notification No. 74/2018 Central Tax dated 31st December, 2018.

In terms of Rule 80(2), every electronic commerce operator required to collect tax at source under section 52 shall furnish annual statement in Form GSTR-9B.

Points to Note on Annual Returns

1.) Nil Annual Return- A person registered under GST but having no transactions during the year is also required to file a Nil Annual Return. A person whose registration has been cancelled during the year is also required to file the Annual returns unless final return has been filed and cancellation completed before 31st March, 2018.

2.) A Registered person who has opted in or opted out of composition is required to file both GSTR 9 & GSTR 9A for the relevant periods.

3.) GSTR-9 does not allow for any revision after filing.

4.) It is mandatory to file FORM GSTR-1 and FORM GSTR-3B for the FY 2017-18 before filing this return.

5.) The exceptions to filing of the Annual return applies to the following category of registered persons:

Input Service Distributor

Tax deductor u/s 51

Tax collector u/s 52

Casual Taxable Person

Non-Resident Taxable Person

any department of the Central Government or a State Government or a local authority, whose books of account are subject to audit by the Comptroller and Auditor-General of India or an auditor appointed for auditing the accounts of local authorities under any law for the time being in force.

6.) The declaration of the information in the Annual returns has multiple implications. Any incorrect information can attract tax demands, interest and penalties on the same, leave alone the long-term litigations that follow years later.

7.) Liability identified during filing Annual Return can be deposited with Government using DRC-03 Form.

Types of forms

Following are the different annual return forms: -

GSTR-9: This form is to be filed by regular taxpayers registered under GST. It consists of details regarding advances, supplies made and received during the financial year under different tax heads i.e. CGST, SGST and IGST as well as details of outward supplies made during the financial year on which tax is not payable. Further, it also contains the details of ITC availed and reversed, taxes payable and paid, transactions reported in next financial year, particulars of demands and refunds, HSN wise details of outward and inward supplies etc. It consolidates the information furnished in the monthly or quarterly returns during the year.

GSTR-9A: This form is to be filed by taxpayers registered under GSTs composition scheme. It is a summary of all quarterly returns previously filed by the composition taxpayer. (Proviso to Sub Rule (1) of Rule 80)

GSTR-9B: This form is to be filed by e-commerce operators who have filed GSTR-8 during the previous financial year. It is basically an annual statement. (Sub-Rule 2 of Rule 80 - Form Not yet notified)

Summary

Here, ISD: Input Service Distributor, CTP= Casual Taxable Person, NRTP= Non-Resident Taxable Person, LA= Local Authority

Consequences of failure to submit the annual return

Notice to defaulters

Section 46 of the CGST Act provides where a registered person fails to furnish a return under section 39 or section 44 or section 45, a notice shall be issued requiring him to furnish such return within fifteen days in such form and manner as may be prescribed.

Late Fee for delayed filing

Section 47(2) of the CGST Act provides for levy of a late fee of Rs. 100/- per day for delay in furnishing annual return in Form GSTR 9, subject to a maximum amount of quarter percent (0.25%) of the turnover in the State or Union Territory. Similar provisions for levy of late fee exist under the State / Union Territory GST Act, 2017.

On a combined reading of Section 47(2) and Section 44 (1) of the CGST Act, 2017 and State / Union Territory GST Act, 2017 a late fee of Rs.200/- per day (Rs. 100 under CGST law + Rs. 100/- under State / Union Territory GST law) could be levied which would be capped to a maximum amount of half percent (0.25% under the CGST Law + 0.25% under the SGST / UTGST Law) of turnover in the State or Union Territory.

General Penalty for Contravention of Provisions

As per section 125, any person, who contravenes any of the provisions of this Act or any rules made there under for which no penalty is separately provided for in this Act, shall be liable to a penalty which may extend to twenty-five thousand rupees. An equal amount of penalty under the SGST/UTGST/IGST Act would also be applicable. To sum up a penalty of up to Rs.75,000/- could be levied.

It is important to note that to impose penalty under section 125 upto Rs. 25,000, the ingredients such as willful default, etc., must be established and by a process of adjudication allowing reasonable opportunity to the taxable person and not imposed as a matter of routine.

Conclusion

The GST Annual Return being mandatory, it would be pertinent to understand the various elements of the Form. In order to assist the readers in filling the form a detailed analysis of the form is presented in the ensuing chapters.

Click Here to Buy CA Final Pendrive Classes at Discounted Rate

About Author

CA Pratibha Goyal

Co Founder

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.