Income Tax Notice held invalid as escaped income was below Rs. 50 lakh: ITAT:

Income Tax Reassessment time-barred, Rs. 50L limit applicable, Section 68 addition validity

Reassessment Notice Quashed: Rs. 50 Lakh Threshold Saves Taxpayer

Income Tax Notice held invalid as escaped income was below Rs. 50 lakh: ITAT

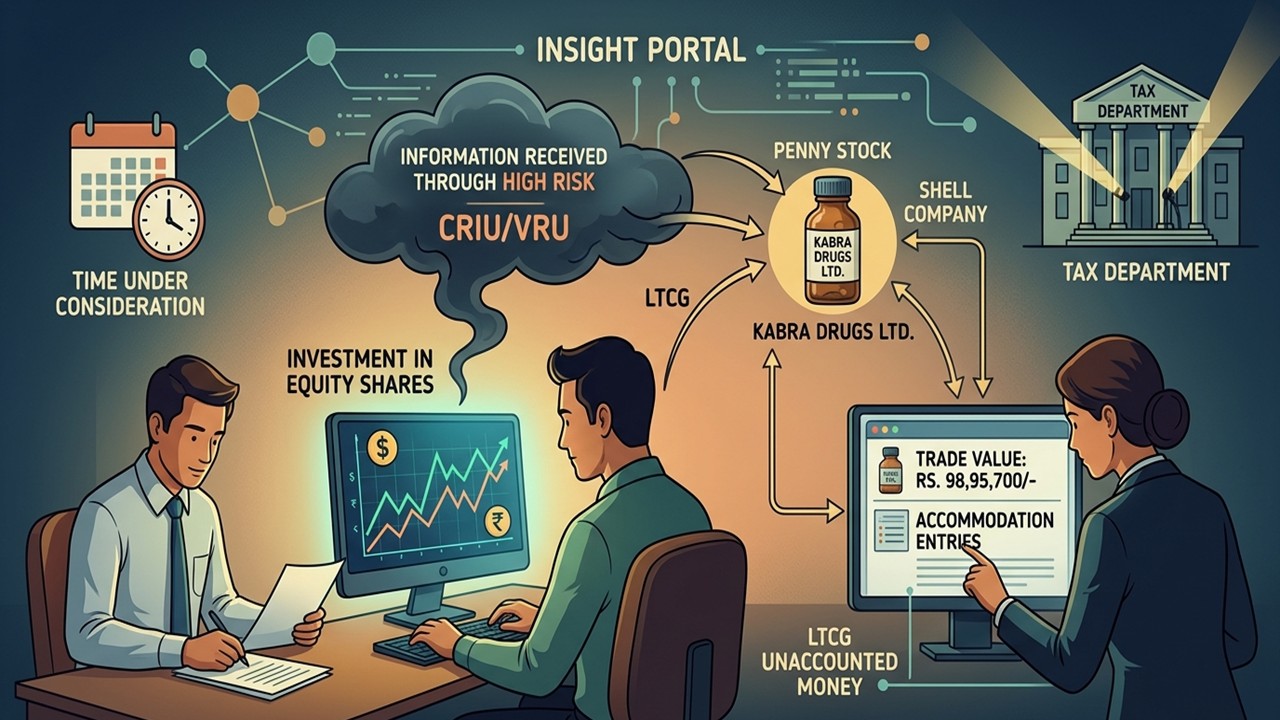

A salaried taxpayer sold Kabra Drugs shares for Rs. 49.47 lakh, but the tax department treated it as a penny stock transaction, reopened the case, and added the amount as unexplained income under Section 68.

Fact of The Case:

The assessee, a salaried person who also invested in shares, claimed that he bought 70,500 physical shares of M/s Kabra Drugs Ltd. in 2009 and later sold 48,500 of them in the financial year 2014–15 for Rs. 49,47,850; however, the Income Tax Department flagged this company’s shares as a “penny stock” often used to convert unaccounted money into legal gains, which led the Assessing Officer to reopen the case under Section 147 by issuing notices under Section 148 in 2021 and 2022, and finally treat the entire sale amount as unexplained income under Section 68 of the Income Tax Act.

Issue Involved in the Case

Whether the reassessment notice for AY 2015–16 issued after 01.04.2021 was time-barred under the new Section 149, whether the extended time limit could be applied when the alleged escaped income was below Rs. 50 lakh, and whether the addition of Rs. 49,47,850 under Section 68 was justified.

Decision of the Tribunal

The Tribunal held that the reassessment notice for A.Y. 2015–16 was time-barred since the normal three-year limit ended on 31.03.2019, and the extended period under Section 149 could not be applied as the alleged escaped income of Rs. 49,47,850 was below Rs. 50 lakh; relying on the Supreme Court ruling in Union of India vs. Rajeev Bansal, where the Revenue itself accepted that such notices issued after 01.04.2021 must be dropped, the Tribunal quashed the reassessment as void ab initio and allowed the assessee’s appeal.

About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2553

2553My Recent Articles

- ITAT Restores Case of Suspicious Transactions to CIT(A) After Rule 46A Application and Key Issues Were Not Properly ConsideredPremium

- ITAT Grants Educational Trust Fresh Opportunity for Seeking 12AB Registration and 80G Approval After CIT(E) RejectionPremium

- ITAT Quashes Section 147 Reassessment Proceedings, Holds Income Tax Dept Must Follow Section 153C After Third-Party SearchPremium

- CBIC Directs CGST Authorities to Share Data with State Mining Departments for Detecting GST Evasion in Illegal Mining Cases

- ICAI Publishes Copy of 77th Annual Report and Accounts of Institute for Year 2025-26 in Gazette of India

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts