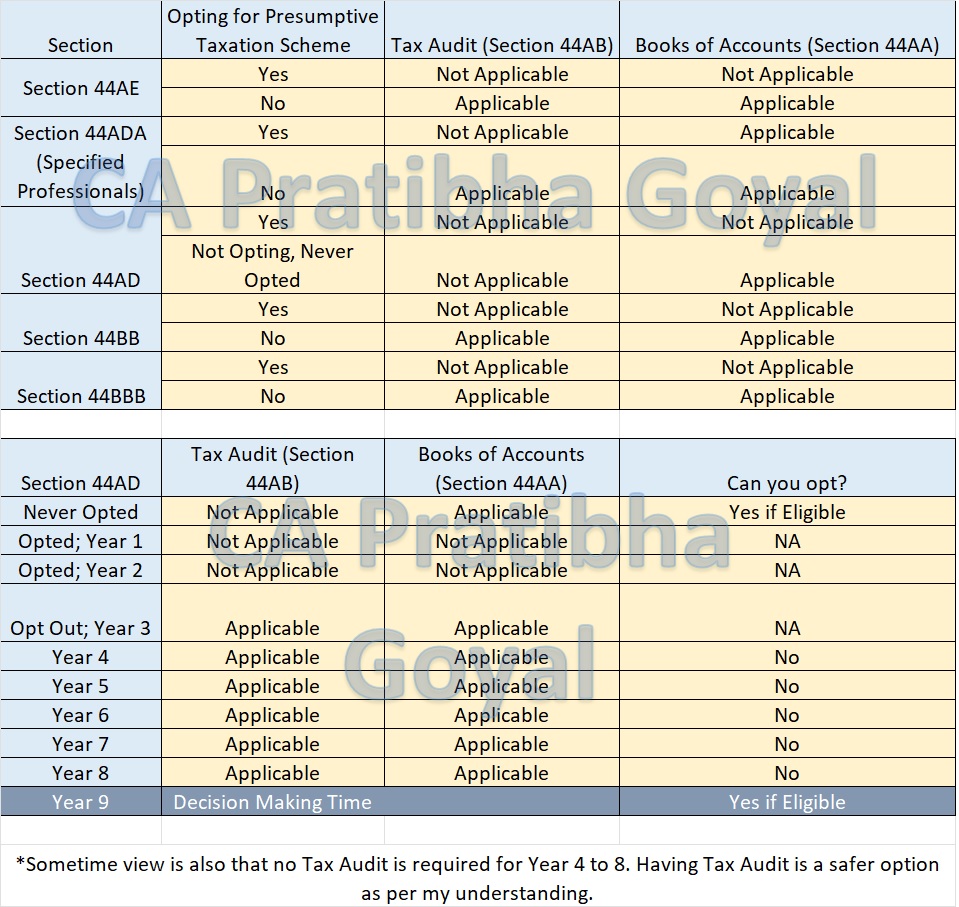

Interplay of Presumptive Taxation Scheme, Tax Audit and Maintaining Books of Accounts:

To give relief to small taxpayers from tedious job of maintenance of books of account and getting it audited, Income tax Act has framed Presumptive Taxation Scheme.

Presumptive Taxation Scheme

Interplay of Presumptive Taxation Scheme, Tax Audit and Maintaining Books of Accounts

Here is, the Interplay of the Presumptive Taxation Scheme (Section 44AD, Section 44ADA, Section 44BB, Section 44BBB, Section 44AE), Tax Audit Applicability (Section 44 AE), and Maintaining Books of Accounts (Section 44AA).

To give relief to small taxpayers from the tedious job of maintenance of books of account and getting the books of account audited, the Income tax Act has framed the Presumptive Taxation Scheme. The taxpayer adopting the Presumptive Taxation scheme can declare income at a prescribed rate instead.

However, the provisions are not as simple as it seems.

Please note that if the company is eligible for the Presumptive Taxation Scheme, the company will maintain Books of Accounts as per the Company Act 2013.

Category of assessees eligible for Presumptive Taxation u/s section 44AD:

An Individual, Hindu undivided family or a partnership firm, who is a resident, but not a limited liability partnership firm as defined under clause (n) of sub-section (1) of section 2 of the Limited Liability Partnership Act, 2008 (6 of 2009).

The eligible assessee must be carrying on any business except the business of plying, hiring or leasing goods carriages referred to in section 44AE; and whose total turnover or gross receipts in the previous year does not exceed an amount of two crore rupees.

Category of Persons not eligible for Presumptive Taxation u/s 44AD.

Please note that if the company is eligible for the Presumptive Taxation Scheme, the company will maintain Books of Accounts as per the Company Act 2013.

Category of assessees eligible for Presumptive Taxation u/s section 44AD:

An Individual, Hindu undivided family or a partnership firm, who is a resident, but not a limited liability partnership firm as defined under clause (n) of sub-section (1) of section 2 of the Limited Liability Partnership Act, 2008 (6 of 2009).

The eligible assessee must be carrying on any business except the business of plying, hiring or leasing goods carriages referred to in section 44AE; and whose total turnover or gross receipts in the previous year does not exceed an amount of two crore rupees.

Category of Persons not eligible for Presumptive Taxation u/s 44AD.

Please note that if the company is eligible for the Presumptive Taxation Scheme, the company will maintain Books of Accounts as per the Company Act 2013.

Category of assessees eligible for Presumptive Taxation u/s section 44AD:

An Individual, Hindu undivided family or a partnership firm, who is a resident, but not a limited liability partnership firm as defined under clause (n) of sub-section (1) of section 2 of the Limited Liability Partnership Act, 2008 (6 of 2009).

The eligible assessee must be carrying on any business except the business of plying, hiring or leasing goods carriages referred to in section 44AE; and whose total turnover or gross receipts in the previous year does not exceed an amount of two crore rupees.

Category of Persons not eligible for Presumptive Taxation u/s 44AD.

- Non residents;

- Persons who have made any claims towards deductions under any of the section 10A, 10AA, 10B, 10BA or deduction under any provisions of Chapter VIA under the heading “C- deductions in respect of certain incomes” in the relevant year;

- a person carrying on any agency business;

- a person carrying on profession as referred to in sub-section (1) of section 44AA;

- a person earning income in the nature of Commission or Brokerage/ Insurance Agents;

- Companies & LLPs

- Legal

- Medical

- Engineering

- Architecture

- Accountancy

- Technical consultancy

- Interior Decoration or

- Other professions notified by CBDT,

About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts