Interplay of TDS/TCS Provisions of Section 194Q & Section 206C(1H)

Interplay of TDS/TCS Provisions of Section 194Q & Section 206C(1H) Provisions of Section 206C(1H) were made applicable w.e.f from 1st Oct 2020 &a…

Table of Contents

Interplay of TDS/TCS Provisions of Section 194Q & Section 206C(1H)

Provisions of Section 206C(1H) were made applicable w.e.f from 1st Oct 2020 & Provisions of Section 194Q will be made applicable w.e.f 1st July 2021.

This article discusses the interplay between TDS Provisions of Section 194Q [Deduction of tax at source on payment of a certain sum for the purchase of goods] and TCS Provisions of Section 206C(1H) [Collection of tax at source on reciept of a certain sum for sale of goods]

Interplay of TDS/TCS Provisions of Section 194Q & Section 206C(1H)[/caption]

Interplay of TDS/TCS Provisions of Section 194Q & Section 206C(1H)[/caption]

Who is liable to Deduct TDS on Purchases?

Person Responsible for Deducting TDS

Buyer is responsible for paying to any resident for the purchase of goods of the value or aggregate of such value in excess of Rs 50 Lakh in any previous year is liable to deduct TDS.Applicability

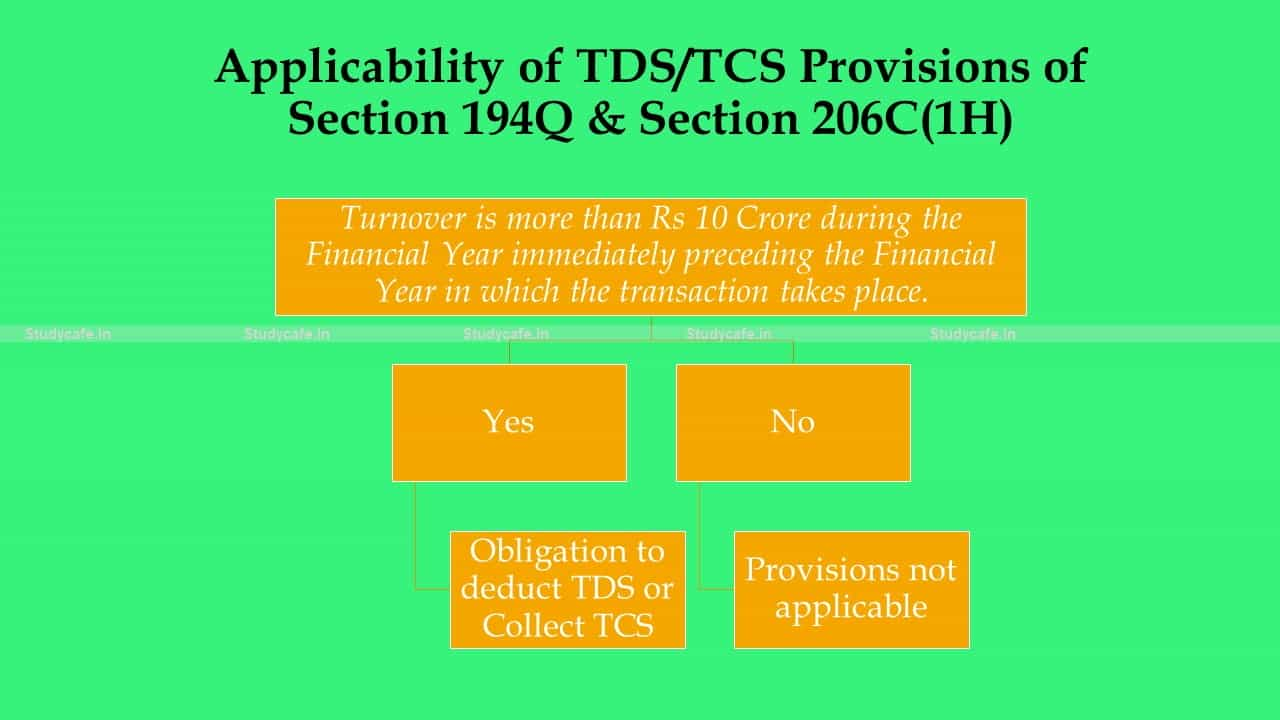

- The provisions of this section will be applicable to the Buyer if the turnover of Buyer is more than Rs 10 Crore during the Financial Year immediately preceding the Financial Year in which the purchase takes place.

Who is liable to Collect TCS on Sales?

Seller is receiving aggregate receipts for the sale of goods of the value or aggregate of such value in excess of Rs 50 Lakh in any previous year is liable to collect TCS.Applicability

- The provisions of this section will be applicable to the Seller if the turnover of Seller is more than Rs 10 Crore during the Financial Year immediately preceding the Financial Year in which the sale takes place.

Interplay of TDS/TCS Provisions of Section 194Q & Section 206C(1H)[/caption]

Rate of TDS/TCS

| Rate | If PAN is available | If PAN is not available |

| TDS | 0.10% | 5% |

| TCS | 0.10% | 1% |

TDS on GST portion of Purchase

- TCS u/s 206C(1H) is applicable on GST Portion of Sales as per Circular No. 17 of 2020. As per CBDT Circular Number 23/2017 no TDS is applicable on GST Portion of Taxable Value of Services. However, there is no such clarification for TDS on the purchase of goods. Thus on the safer side, one should Deduct TDS on GST Portion of Purchase of Goods as well.

Brief Pointers:

- Purchase Expenditure up to the extent of 30% will be disallowed in case of Failure to Deduct TDS u/s 194Q

- TDS u/s 194Q is not applicable in case of import of Goods

- TCS u/s 206C(1H) is not applicable in the case of the export of Goods.

- One May Also note that Section 194Q makes no distinction between Capital goods or stock in trade. Provisions of Section 194Q will be equally applicable on the Purchase of Capital Goods if the transaction qualifies monetary limits specified in the Section.

What to do when on a Transaction TDS is liable to be deducted under any other Section and provisions of TDS u/s 194Q are also applicable?

If TDS is liable to be deducted under any other section of Income Tax, then provisions of Section 194Q will not be applicable. Please note that If any transaction attracts TCS under section 206C(1H) and TDS under section 194Q, then TDS under section 194Q will be applicable. But if TCS is liable to be collected under any other provisions of Section 206C, then TDS under section 194Q will not be applicableAbout Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts