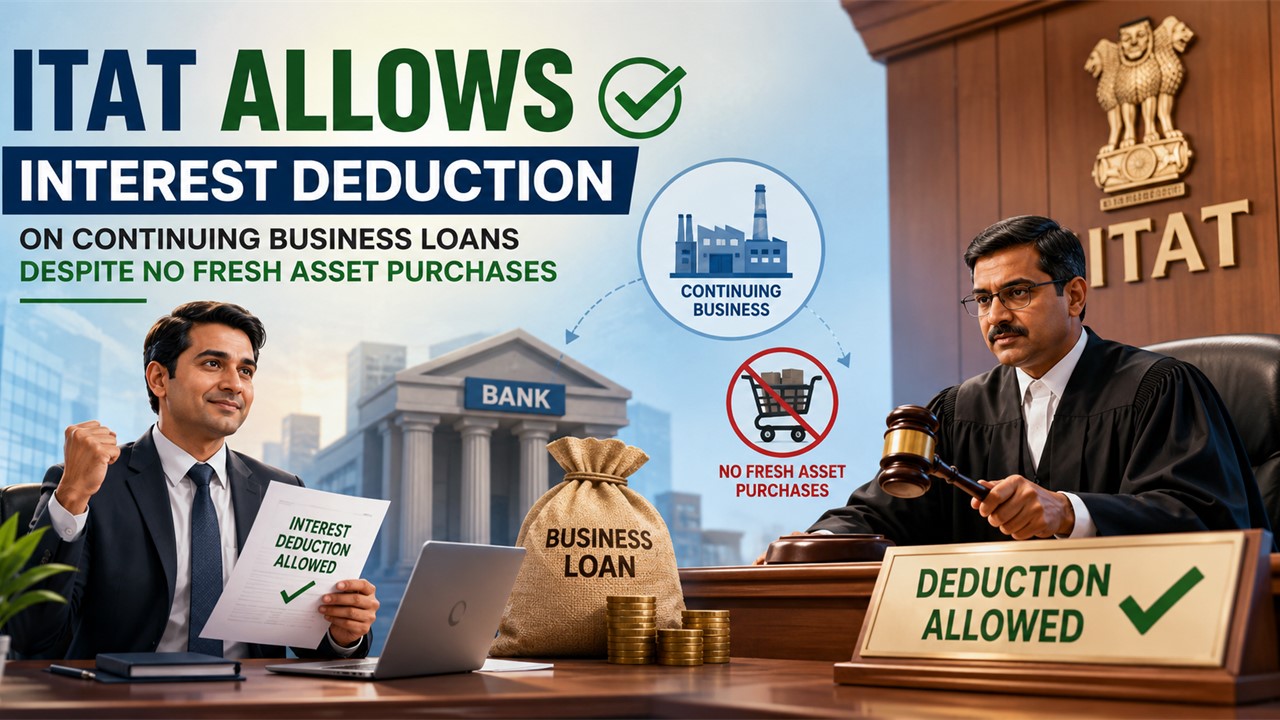

ITAT Grants Relief Against Vehicle Loan Interest Disallowance Addition:

ITAT allows interest deduction on continuing business loans despite no fresh asset purchases during year.

AO Disallowed Interest Citing Absence of Fresh Vehicle Purchases During Year

The Delhi Bench of the Income Tax Appellate Tribunal (ITAT) on 15 April held that interest paid on loans taken for the purchase of business assets in earlier years cannot be disallowed merely because no new assets were acquired during the relevant assessment year. A Bench comprising Accountant Member S. Rifaur Rahman and Judicial Member Vimal Kumar deleted the disallowance of Rs 10.49 lakh made against Bright Enterprises Pvt. Ltd. for AY 2016-17 and held that the interest expenditure constituted a genuine business expense.

The Assessing Officer (AO) had observed that there was an increase in interest expenditure on vehicle loans without any corresponding addition to fixed assets during the year. On that basis, the AO restricted the claim of interest expenditure and disallowed the excess amount of Rs. 10.49 lakh. The Commissioner of Income Tax (Appeals) affirmed the addition.

Before the ITAT, Bright Enterprises submitted that the loans pertained to vehicles purchased during the earlier assessment year. It explained that one of the cars had been acquired towards the end of the preceding financial year and therefore interest for only part of the year was claimed earlier, whereas full-year interest was claimed during the year under consideration. The assessee also produced the fixed asset schedule and details of the vehicle loans obtained from HDFC Bank.

The Tribunal observed that the loans were admittedly taken for the purchase of business vehicles and the interest expenditure had been allowed in earlier years. It further noted that the increase in interest cost was attributable to the fact that the loans remained outstanding for the entire year under consideration. The court highlighted that “Merely because there is no purchase of vehicles in the year under consideration, it does not mean that the interest claimed by the assessee is excessive as it was claimed on the assets purchased in the earlier years, for which the loan is outstanding in the year under consideration.”

The Bench held that the interest expenditure represented a genuine business expense incurred on loans obtained from banks for acquisition of business assets. It further observed that the absence of fresh purchases during the relevant year could not be a valid ground for disallowing interest on existing business liabilities.

Thus, the ITAT deleted the addition and allowed the appeal in favour of the assessee.

To Read Full Order, Download PDF Given Below

About Author

Meetu Kumari

Content Manager

Studycafe

Studycafe Jodhpur, Rajasthan, India

Jodhpur, Rajasthan, India 2257

2257My Recent Articles

- ITAT Deletes Rs 8.49 Crore Additions, Says CIT(A) Can Admit Evidence to Grant ReliefPremium

- ITAT Restores Appeal After Condoning Delay, Says Substantial Justice Must Prevail Over TechnicalitiesPremium

- ITAT Allows Section 80-IE Deduction on Enhanced Business Income After Assessment AdditionPremium

- India Notifies India-Sri Lanka DTAA Protocol Introducing Principal Purpose Test

- ITAT: Entire Gross Receipts of Trust Cannot Be Taxed Despite Section 11 DenialPremium

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts