NBFC Faced ₹3.09 Crore Tax Addition Over Alleged Accommodation Entry; ITAT Upholds Fresh Hearing Due to Natural Justice Violations:

ITAT upholds CIT(A)’s remand order, directs AO to re-adjudicate reassessment after granting fair hearing.

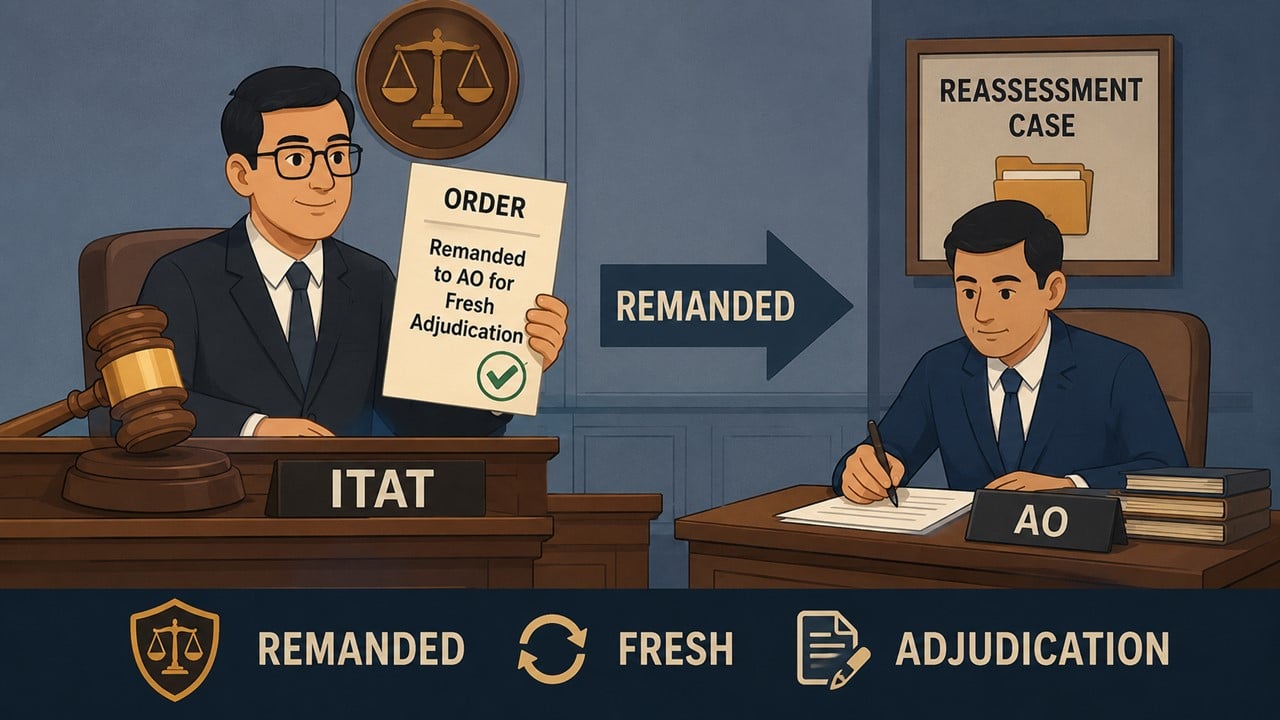

ITAT Upholds CIT(A) Order for Fresh Adjudication

NBFC Faced ₹3.09 Crore Tax Addition Over Alleged Accommodation Entry; ITAT Upholds Fresh Hearing Due to Natural Justice Violations

The Delhi Bench of the Income Tax Appellate Tribunal (ITAT) has dismissed the appeal filed by M/s Rita Finance Pvt. Ltd. for Assessment Year 2022-23 and upheld the order of CIT(A).

The dispute came up after the revenue got information that the company had allegedly received accommodation entries of Rs. 3 crores from the entities related to Galaxy Group. On the basis of this information, proceedings for reassessment were initiated under section 148 of Income Tax Act.

AO noted that the assessee had not responded to various statutory notices issued during the reassessment proceedings. Accordingly AO passed best judgment assessment u/s 144 and made addition of Rs. 3 crores u/s 68 (unexplained cash credits) and Rs. 9 lakh u/s 69C (unexplained expenditure) and assessed total income of Rs. 4,65,09,910 against returned income of Rs. 1,56,09,910.

Before the CIT(A) the company pleaded that the reassessment proceedings were in violation of principles of natural justice. Significant documents like reasons for reopening, appraisal reports, statements and other relied upon materials were not furnished or furnished very late it said. The company also argued that the AO has not considered the detailed reply and supporting documents filed by it in the month of February 2025.

The CIT(A) on perusal of the record, found merit in these objections. The appellate authority observed that the reply filed by the assessee was not properly considered and serious procedural lapses had taken place including denial of fair opportunity of hearing. The CIT(A) was of the opinion that the proceedings of reassessment were vitiated by violation of principles of natural justice and accordingly set aside the order of assessment and directed the AO to pass a fresh reasoned order after giving adequate opportunity to the assessee.

The assessee then moved to the ITAT arguing that the CIT(A) should have quashed the reassessment proceedings in entirety and not remanded the matter to the AO. The assessee further contended that the loan transaction was real as the money was received and repaid through banking channels and supported by financial statements and tax documents.

The Revenue submitted that the assessee had not cooperated with the assessment proceedings and the decision of the CIT(A) to restore the matter to AO was fair and justified.

The ITAT observed that it was not in dispute that the assessee had not complied with statutory notices issued during assessment proceedings. The Tribunal also observed that there is evidence that the AO did not properly consider the later submissions and defence of the assessee.

Considering these facts, the Tribunal held that the CIT(A) was justified in setting aside the assessment and directing a fresh examination of the case.

As a result, the tribunal stated that "we do not find any infirmity in the decision of the ld. CIT(A) to have set-aside the matter to ld. AO for re-adjudication. Accordingly, we confirm the order of the Ld. CIT(A) and dismiss all the grounds raised by the assessee".

About Author

Vanshika verma

Content Writer

Vanshika Verma is a Content Writer with 1+ year of experience at Studycafe.in. A B.Com graduate from Delhi University, She writes articles on Finance, Tax, ICAI, GST, and the latest financial news, with a focus on making complex topics easy for readers and professionals.

Vanshika Verma is a Content Writer with 1+ year of experience at Studycafe.in. A B.Com graduate from Delhi University, She writes articles on Finance, Tax, ICAI, GST, and the latest financial news, with a focus on making complex topics easy for readers and professionals.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 1636

1636My Recent Articles

- ITAT Allows Fresh Opportunity in Dispute Over Suppressed Sales and Commission ExpensesPremium

- ITAT Deletes Rs 2.13 Crore Addition Under Section 68, Grants Major Tax ReliefPremium

- ITAT: Protective Addition Cannot Survive After Substantive Assessment Is QuashedPremium

- ITAT Remands Rs 8.12 Crore Cash Withdrawal Disallowance Case to AO for Fresh AssessmentPremium

- ITAT Deletes Rs 1.20 Crore Disallowance on Business Development and Marketing ExpensesPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts