Non-Filing of Annual Return: ROC levies penalty of Rs.23,50,300:

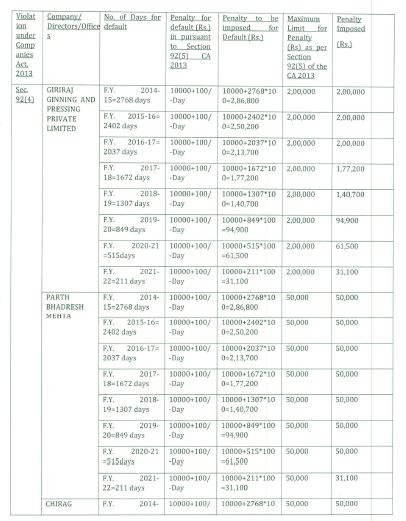

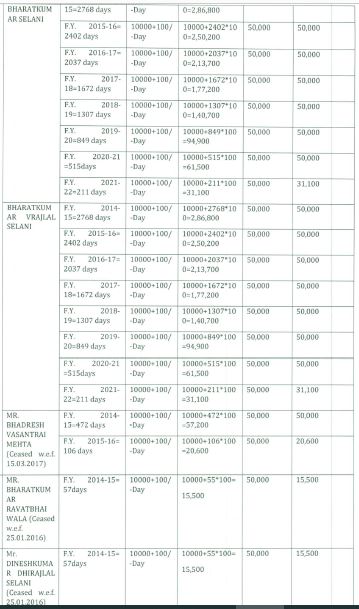

The Registrar of Companies in the matter of GIRIRAJ GINNING AND PRESSING PRIVATE LIMITED has imposed penalty of Rs.23,50,300 for Non-Filing of Annual Return.

Penalty for Non-Filing of Annual Return

Table of Contents

Non-Filing of Annual Return: ROC levies penalty of Rs.23,50,300

The Registrar of Companies in the matter of GIRIRAJ GINNING AND PRESSING PRIVATE LIMITED has imposed penalty of Rs.23,50,300 for Non-Filing of Annual Return.

Giriraj Ginning And Pressing Private Limited (herein after referred to as "company") is a company registered under the provisions of the Companies Act, 1956/2013 [hereinafter referred to as "Act") in the State of Gujarat on 11.09.1998 having its registered office at "SUR NO 5A AT HADAMTALA TALKOTDA SANGANI, DIST RAJKOT, GUJARAT". The CIN of the Company is U17L19GJL99BPTCO34650.

The Company/Officer are further directed to rectify the default failing which this office shall be proceeded further the matter in pursuant to Section 454A of the Companies Act, 2013 for the non-compliance of the aforesaid provisions of the Companies Act, 2013.

The noticee shall pay the amount of penalty individually for the company and its officers from their personal sources/income by way of e-payment available on Ministry website under "Pay miscellaneous fees" category in MCA fee and payment Services under Rule 3(14) of Company (Adjudication of Penalties) (Amendment) Rules, 2019 within 90 days from the date of receipt of this order and copy of this adjudication order and Challan/SRN generated after payment of penalty through online mode shall be filed in INC-28 under the MCA portal without further reference.

For Official Order Download PDF Given Below:

The Company/Officer are further directed to rectify the default failing which this office shall be proceeded further the matter in pursuant to Section 454A of the Companies Act, 2013 for the non-compliance of the aforesaid provisions of the Companies Act, 2013.

The noticee shall pay the amount of penalty individually for the company and its officers from their personal sources/income by way of e-payment available on Ministry website under "Pay miscellaneous fees" category in MCA fee and payment Services under Rule 3(14) of Company (Adjudication of Penalties) (Amendment) Rules, 2019 within 90 days from the date of receipt of this order and copy of this adjudication order and Challan/SRN generated after payment of penalty through online mode shall be filed in INC-28 under the MCA portal without further reference.

For Official Order Download PDF Given Below:

Fact About Case:

The Ministry has ordered to inquiry of the subject company u/s 206(4) of the Companies Act, 2013. During the course of Inquiry, it is observed that the company has failed to file Annual Return for the Financial year ended 31.03.2015, 31.03.2016, 31.03.2017, 31.03.2018, 31.03.2019, 31.03.2020, 31.03.2021 and 31.03.2022 as per the requirement of provisions of Section 92(4) of the companies Act, 2013 and the aforesaid provisions of the companies Act, 2013 have not been complied with. Hence, the company, its directors, officers in defaults are liable to be penalized under section 92(5) of the Companies Act, 2013 Read with Section 454 of the Companies Act, 2013. The Directorate vide order dated 05.09.2022 has issued directions to ROC, Ahmedabad to take necessary action in the matter accordingly. The said Annual Return has not so far been filed under the MCA21 portal till date and the undersigned has reasonable cause to believe that aforesaid provisions of the Companies Act, 201.3 have not been complied with. The Registrar of Companies vide the Companies (Amendment) Act, 2019 is entrusted with power to adjudicate penalty as provided under Section 92(5) of the Companies Act, 2013 w.e.f. 02.11.2018. The DGCoA vide letter dated 11.05.2022 has instructed that all cases filed under Companies Act, 1956 and Companies Act 2013 can be considered under In house Adjudication Penalty Mechanism (IAM). The DGCoA further directed that all cases filed under CA, 1956 and CA, 2013 can be considered for adjudication process which are now decriminalized (earlier prosecutions to be filed by Companies Amendment Act effective from 02.11.2018 and further Amendment in 2020 effective from 28.09.2020). By keeping in mind, the ease of doing business in India and in compliance to the instructions of the Ministry, the matter should be considered to take cognizance of the default committed for the financial year 2016-17 under In house Adjudication Penalty Mechanism (1AM).Order:

1. While adjudging quantum of penalty under 92(5) of the Act, the Adjudicating Officer shall have due regard to the following factors, namely; a. The amount of disproportionate gain or unfair advantage, whenever quantifiable, made as a result of default. b. The amount of loss caused to an investor or group of investors as a result of the default. c. The repetitive nature of default. With regard to the above factors to be considered while determining the quantum of penalty, it is noted that the disproportionate gain or unfair advantage made by the noticee or loss caused to the investor as a result of the delay on the part of the notice to redress the investor grievance are not available on the record. Further, it may also be added that it is difficult to quantify the unfair advantage made by the noticee or the loss caused to the investors in a default of this nature. Having considered the facts and circumstances of the case and submissions made by the Presenting Officer and after taking into accounts the factors above, the undersigned has reasonable cause to believe that the company and its officers in default have failed complied with the provisions of Section 92 (4) of the Companies Act, 2013. Hereby ROC has imposed below mentioned penalty for default in non filing of Annual Return for the Financial Year ended 31.03.2015, 31.03.2016, 31.03.2017, 31.03.2018, 31.03.2019, 31.03.2020, 31.03.2021 and 31.03.2022.

The Company/Officer are further directed to rectify the default failing which this office shall be proceeded further the matter in pursuant to Section 454A of the Companies Act, 2013 for the non-compliance of the aforesaid provisions of the Companies Act, 2013.

The noticee shall pay the amount of penalty individually for the company and its officers from their personal sources/income by way of e-payment available on Ministry website under "Pay miscellaneous fees" category in MCA fee and payment Services under Rule 3(14) of Company (Adjudication of Penalties) (Amendment) Rules, 2019 within 90 days from the date of receipt of this order and copy of this adjudication order and Challan/SRN generated after payment of penalty through online mode shall be filed in INC-28 under the MCA portal without further reference.

For Official Order Download PDF Given Below:About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts