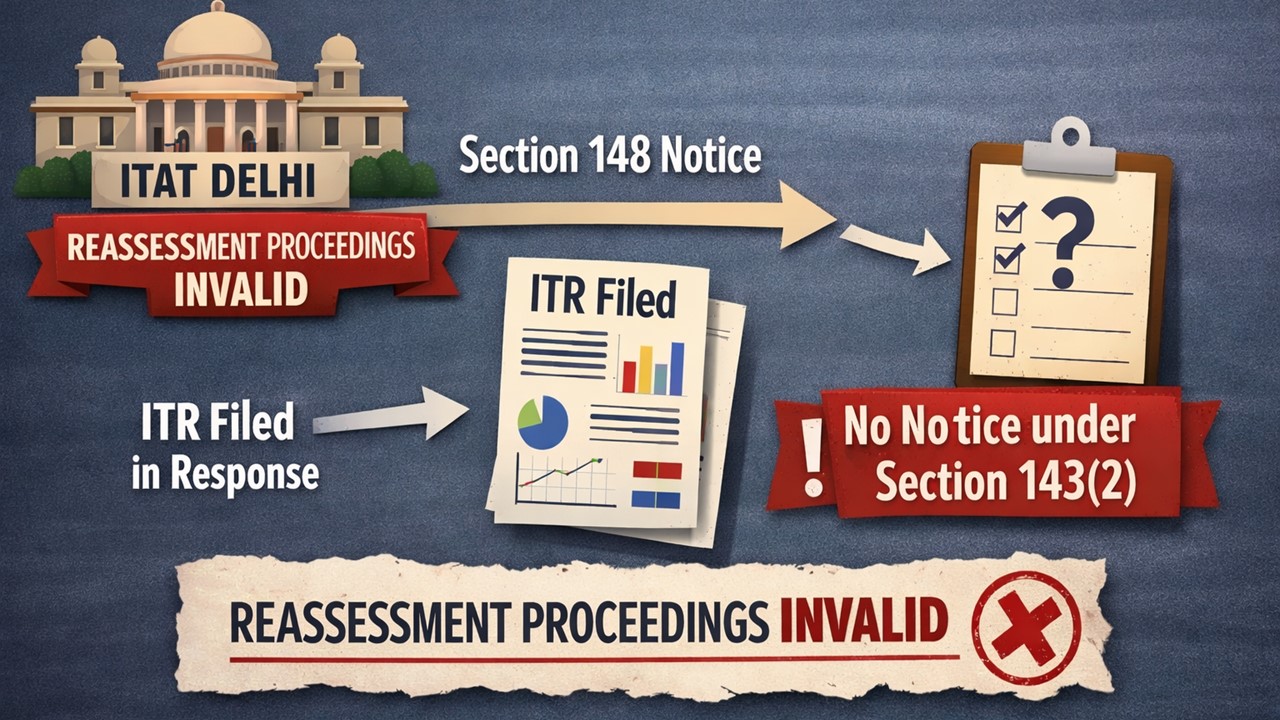

Reassessment Proceedings Are Invalid Without Section 143(2) Notice, Says ITAT:

The ITAT held that reassessment proceedings are invalid if no mandatory notice under Section 143(2) is issued after filing ITR in response to Section 148 notice.

ITAT Quashes Rs 2.23 Crore Addition

Reassessment Proceedings Are Invalid Without Section 143(2) Notice, Says ITAT

The ITAT Delhi quashed the reassessment order, holding that once a taxpayer filed its ITR in response to the notice issued under Section 148, thereafter the tax authorities are compelled to issue another notice under Section 143(2) in their next step. In the absence of this notice, the entire reassessment proceedings are considered invalid.

The case of Sitanshu Gupta (assessee or appellant) was reopened based on the information received from the Deputy Director of Income Tax (Investigation)-1, Faridabad. In conclusion of the reassessment, the tax authorities had made an addition amounting to Rs 2.23 crore to the assessee's income.

The assessee, being aggrieved with the reassessment order, filed an appeal before the Commissioner of Income Tax (Appeals) [CIT(A)]; however, his appeal was rejected. Thereafter, the assessee filed another appeal before the Income Tax Appellate Tribunal (ITAT), Delhi, arguing that the tax authorities had not issued the mandatory notice under Section 143(2) of the Income Tax Act after the issuance of the Section 148 notice. The tax authorities argued that under Section 292BB, the assessee has no right to highlight this topic at a later stage since, during the assessment proceedings in the present, he had not raised an objection regarding this issue.

When the tribunal analysed the case, it noted that the tax authorities had failed to issue a mandatory notice under Section 143(2) of the Income Tax Act. Which ultimately makes the entire reassessment proceedings invalid. The ITAT held that once an income tax return (ITR) is filed in response to a notice under Section 148, it becomes mandatory for the tax authorities to pass a notice under Section 143(2) in their next step. However, in the present case, no such notice was issued by the tax authorities.

To support this ruling, the tribunal also cited an earlier judgement of the Supreme Court of India in the case of Laxman Das Khandelwal, based on the same issue. The tribunal further flagged that Section 292BB only applies to cases where there is a defect in serving a notice, not where no notice was issued at all. Therefore, this defect could not be corrected.

In conclusion to the aforementioned findings, the tribunal quashed the impugned reassessment order and held in favour of the assessee.

About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2525

2525My Recent Articles

- GST Collections Jump 15.4% to Rs 2.11 Lakh Crore in July 2026; Haryana Tops State-Wise Growth

- ICAI Announces ISA Assessment Test Declaration Date; Scorecard to Be Released on isaat.icai.org

- ICAI Offers One-Time Opportunity to CA Final Passed Candidates for Completing Virtual Advanced ITT and MCS Courses

- High Court Directs Custom Dept to Shift Accused to KIMS Hospital for Medical Treatment under Police EscortPremium

- CBI Court Sentences Eight Accused to 10 Years Rigorous Imprisonment in Rs 1.97 Crore SBI Loan Fraud Case

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts