ITAT Delhi Quashes 153C Assessments Over Lack of ‘Bearing’ in Satisfaction Note:

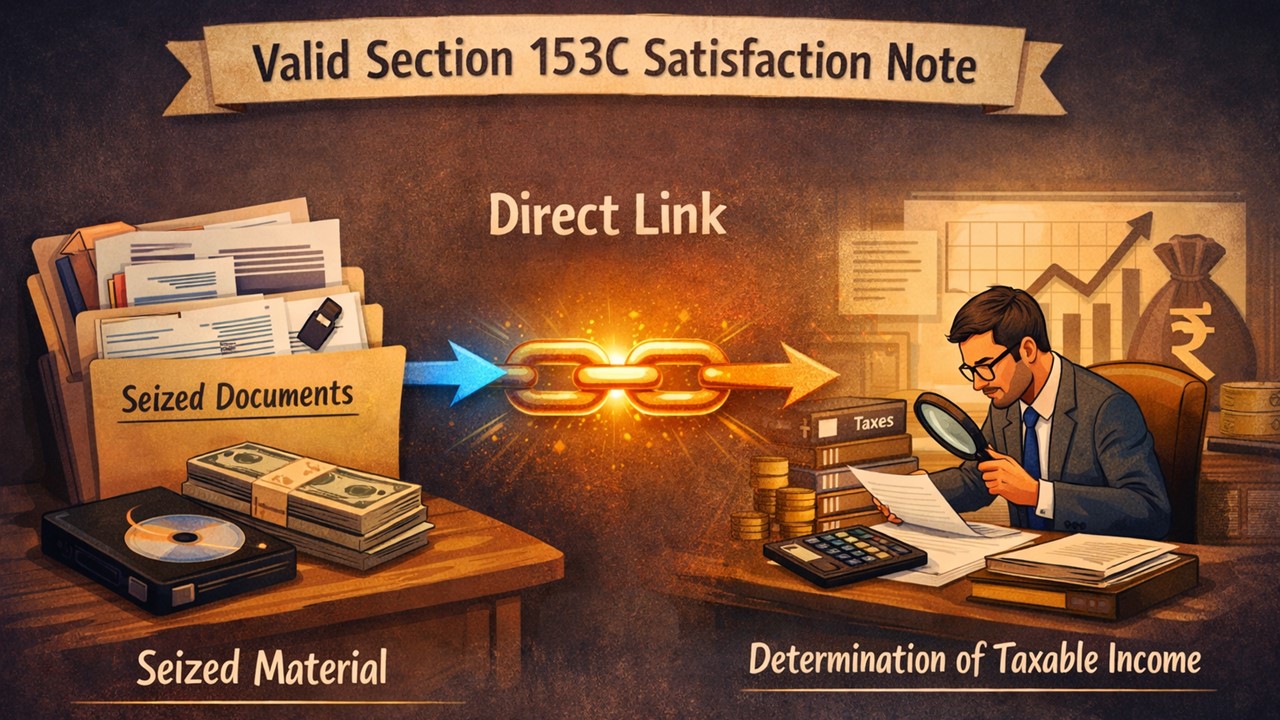

The ITAT held that a valid Section 153C satisfaction note must clearly establish a direct link between seized material and the determination of taxable income.

ITAT Finds No ‘Bearing’ on Taxable Income”

ITAT Delhi Quashes 153C Assessments Over Lack of ‘Bearing’ in Satisfaction Note

The ITAT held that a valid Section 153C satisfaction note must clearly establish a direct link between seized material and the determination of taxable income. Since the AO failed to demonstrate this "bearing", in conclusion, the tribunal quashed all assessments.

The Income Tax Appellate Tribunal (ITAT), Delhi, has delivered its judgement on seven appeals simultaneously for the Assessment Years 2013-14 to 2020-21. The appeals were filed by M/s Atoll Vyapaar (P) Limited against the Income Tax Authorities.

The dispute arose from assessments made under Section 153C read with Section 143(3) of the Income-tax Act, 1961. These assessments were made following a search operation conducted on October 18, 2019, in relation to the issue with M/s. Alankit Group. The search concluded that certain materials were allegedly linked to the assessee. Based on this, the Assessing Officer (AO) recorded a satisfaction note on December 24, 2021, to initiate proceedings against the assessee for multiple years.

The assessee claimed that the note failed to prove that the confiscated material had a direct relation or "bearing" on determining its taxable income for the relevant years. The tax authorities claimed that using the specific word “bearing” to determine the assessee’s taxable income in such a satisfaction note under Section 153C of the Act is not mandatory. However, the tribunal held that it is obligatory for such satisfactory notes to establish a clear link between seized material and income determination. To support this ruling, the tribunal also cited a Delhi High Court judgement in a case titled 'Saksham Commodities Ltd. vs. ITO (2024).

Since the AO's satisfactory note did not meet the aforementioned requirements, the tribunal quashed all the assessments made under Section 153C of the Act and allowed all seven appeals of the assessee.

About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2515

2515My Recent Articles

- Missed July 31 ITR Deadline? Here’s What Taxpayers Need to Know Now

- Confused Between Belated, Revised and Updated Return? Here's Clarification on What You Should File

- Missed the July 31 ITR Deadline? File Your Belated Return to Avoid Penalties, Refund Loss, and Tax Notices

- Why Do You Need to File an ITR? 6 Key Reasons Every Taxpayer Must Know Before July 31 Deadline

- SC Directs IGP Kiran S. to Head Reconstituted SIT, Directs CA Appointment in Ayodhya Ram Temple Donation Theft Probe

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts