UAE VAT : Registration Provisions and Procedures

reclaiming vat on expenses uae, uae vat law pdf, vat in uae pdf, uae vat law download, vat on export in uae, vat on imports in uae, value ad

Table of Contents

reclaiming vat on expenses uae, uae vat law pdf, vat in uae pdf, uae vat law download, vat on export in uae, vat on imports in uae, value added tax uae ppt, vat on imported goods in uae, Registration Provisions and Procedures under UAE VAT, vat deregistration uae, uae vat registration online, vat registration uae, fta, vat group registration uae, vat in tally uae, how to check vat registration, vat filing in uae, UAE VAT : Registration Provisions and Procedures, Registration Procedure under UAE VAT

UAE VAT : Registration Provisions and Procedures |Being registered under the VAT law means that a business is acknowledged by the government, as a supplier of Goods and Services and is authorized to collect VAT from customers and remit the same to the government. Only VAT registered businesses will be allowed to do the following:-

- Charge VAT on taxable supply of goods and services.

- Claim Input Tax Credit on VAT paid on their purchases, which will be deducted from VAT liability on sales.

- Payment of VAT to the government.

- Periodic filing of VAT return.

UAE VAT : Registration Provisions and Procedures

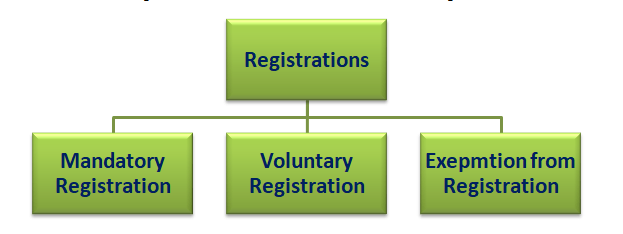

Who should register under UAE VAT

Are all businesses liable to register under VAT No, only those businesses crossing the defined annual aggregate turnover threshold are liable to register under VAT. Based on the registration threshold, a business will either be mandated to register or as an option, a business can apply for registration or can seek exemption from VAT registration, in case it is engaged only on supply of Zero rated supplies. On this basis, VAT registration in UAE can be classified into the following:

Article (13) of Decree-Law: Mandatory Registration under UAE VAT

Every Person, who has a Place of Residence in the State or an Implementing State and is not already registered for Tax, shall register in the following situations:-

-

- Where the total value of all supplies referred to in Article (19) exceeded the Mandatory Registration Threshold limit i.e AED 375,000 over the previous 12-month period.

- Where it is anticipated that the total value of all supplies referred to in Article 19 will exceed the Mandatory Registration Threshold in the next thirty 30 days.

-

VAT Registration Threshold Calculation in UAE

-

-

- The value of taxable supply of Goods and Services:Taxable supplies refer to all the supplies of goods and services made in UAE on which VAT is levied at the standard rate of 5% including zero-rated supplies. This does not include the notified supplies which are exempted from VAT.

- The value of reverse charge Supplies:Reverse charge supplies are those notified supplies on which the recipient or the buyer are required to pay the VAT to the government unlike forward charge, where the supplier will collect VAT from the buyer and pay. The value of such supplies needs to be considered in arriving at the turnover threshold for VAT registration.

- Imports: The value of taxable goods and services imported on which the importer is liable to pay tax.

-

| Type of Supplies | Turnover in AED | Qualifying Turnover for Calculation Threshold Limit |

| Taxable Supplies (Sale in UAE) | 375,000 | 375,000 |

| Exports (Zero-Rated Supplies) | 125,000 | 125,000 |

| Exempt Supplies | 50,000 | - |

| Imports | 100,000 | 100,000 |

| Reverse Charge Supplies | 25,000 | 25,000 |

Consequences for Non Registration:

In case of failure of a person to apply for registration when he becomes liable to do, the following will be consequences:-

-

- Authority shall register such person with effect from the date on which the Person first became liable (obliged) to be registered, with effect from the first day of the month following the month in which the Person is required to register.

- Penalties for Non Registration as per Executive Regulations.

- liable to account for and pay to the Authority the Due Tax on all Taxable Supplies and Imports made by him before registering.

-

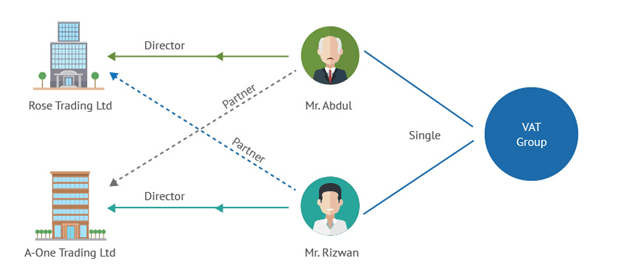

Article (14) of Decree-Law: Tax Group

In UAE VAT, any person conducting a business is not allowed to have more than one Tax Registration Number (TRN), unless otherwise prescribed in the UAE Executive Regulation. Thus, even if you are operating via branches in more than one Emirate, only one VAT registration is required. With the similar objective, if two or more persons are related or associated parties in the businesses, they are allowed to apply for VAT group registration. The VAT Law has provided an option for persons conducting business to apply for registration as a tax group. Persons can apply for Tax registration as a Tax group if all of the following conditions are fulfilled:-

-

- Each person should have a place of establishment or a fixed establishment in the State of UAE.

- Such persons should be related parties as per the definition mentioned in this VAT Law.

- One or more persons conducting business in partnership shall control the other.

- Each person should have a place of establishment or a fixed establishment in the State of UAE.

-

Two or more Persons shall be considered Related Parties if they are associated in economic, financial and regulatory aspects, taking into account the following:

A. Economic practices, which shall include at least one of the following:

Two or more Persons shall be considered Related Parties if they are associated in economic, financial and regulatory aspects, taking into account the following:

A. Economic practices, which shall include at least one of the following:

-

-

- Achieving a common commercial objective;

- One Persons Business benefiting another Persons Business;

- Supplying of Goods or Services by different Businesses to the same customers.

-

-

-

- Financial support given by one Persons Business to another Persons Business.

- One Persons Business not being financially viable without another Persons Business.

- Common financial interest in the proceeds.

-

-

-

- Common management.

- Common employees whether or not jointly employed.

- Common shareholders or economic ownership

-

VAT Group Registration Benefits

The following are the benefits of VAT Group Registration for the business:-

-

- All the entities within a VAT Group will be treated as 'ONE' entity for VAT purpose. This will help the businesses in simplifying accounting for VAT, and also compliance reporting like VAT returns are required to be prepared and reported at the group level instead of entity level.

- Any supplies within the entities of a VAT group, are out of the scope of the VAT. This means, VAT will not be levied on the supplies between the entities of a VAT Group. However, supplies made by the VAT group to an entity outside the VAT group are subject to VAT.

-

Procedure for Registration as Tax Group

Step-1: Creating and using your e-Services account When you arrive at the FTA website (https://eservices.tax.gov.ae/en-us/loginreturnurl=%2fen-us%2fuser%2fdashboard), you will notice in the top right hand corner of the screen you have the option to either Sign up to the e-Services account service, or Login to an existing e-Services account. Create an e-Services account (new users) Sign up To create an account, simply click on the Sign up button on the home page. To sign up, you must enter a working email address and a unique password of 6-20 characters that includes at least: one number; one letter; and one special character (i.e. @, #, $, %, & and *). You must confirm that you are a genuine applicant by completing the CAPTCHA or alphanumeric verification test that you will see. Finally, you will be asked to select a security question and provide an answer and a hint in order to recover your password in case you forget it. Verify your e-Services account You will receive an email at your registered email address asking you to verify your email address. Please verify your email address within 24 hours of requesting to create the e-Services account, otherwise the verification link will expire and you will have to re-register. Once you have successfully verified your email address, your e-Services account will be created and you will be invited to Login for the first time. Services available in your e-Services account There are a number of dedicated services available to you through your e-Services account. Currently, you will be able to access the following:-

-

- Dashboard which displays key information relating to your VAT and Tax group registration/amendments.

- My Profile which contains a range of information about your e-Services account; and

- Downloads which contains more detailed guidance which is designed to help you understand and manage your day-to-day VAT obligations.

-

-

-

- Be a legal person

- Be resident in the UAE; and not a member of another Tax group.

-

-

-

- On logging into your e-Services account, click on the Register for VAT button. You will arrive at the VAT registration form.

- Please select the Yes button for the field Are you also applying to create or join a Tax group

- Complete the VAT registration form and submit it. Upon submission of the completed form, you will receive a Tax Identification Number (TIN). A TIN is not a valid TRN. It is a Tax Identification Number issued by the FTA for Tax group registration purposes and will be displayed on the Dashboard tab.

- As the representative member of a Tax group, you will now see a button inviting you to apply to Register for Tax group.

- Please select the Yes button for the field Are you intending to apply as the Representative Member of the Tax Group

- Youre TRN/TIN and legal name in both English and Arabic will be auto-populated as shown below.

- Please click on Add member to the group button to add the member to the Tax group.

- Please agree to the declaration at the bottom of the form by checking the box for I accept & agree as shown on the right.

-

-

-

- From the first day of the Tax Period following the Tax Period in which the application is received;

- From any date as determined by the Authority.

-

-

-

- The Persons do not meet the requirements for Tax Group registration in accordance with the provisions of the Decree-Law and Article (9) of the Executive Regulations.

- Where there are serious grounds for believing that if the registration as a Tax Group is permitted, it would enable Tax Evasion or significantly decrease Tax revenues of the Authority or increase the administrative burden on the Authority significantly.

- Where any of the Persons included in the application is not a legal Person.

- Where one of the Persons is a Government Entity specified under Article (10) and (57) of the Decree-Law and the other is not.

- If there are serious grounds for believing that registering the Related Parties would significantly decrease Tax revenue.

-

-

-

- Addition of a new member to the Tax group;

- Removal of an existing member from the Tax group; and

- Amendment of the Tax group details

-

-

-

- Be a legal person

- Be resident in the UAE; and

- Not a member of another Tax group.

-

Article 17- Voluntary Registration

There could be situations where a person, though not mandatorily required to register, may be willing to register. The purpose of voluntary registration could be to recover input tax credits so that cascading effect of taxes does not take place. Conditions to be satisfied for Voluntary Registration:-

-

- Where the person intending to opt for registration establishes that the value of total supplies made by him in the preceding 12 months have exceeded the voluntary registration threshold limit i.e. AED 187,500.

- If the value of supplies has not exceeded but the taxable expenses* incurred by such person within this time has crossed voluntary threshold limit.

- If the value of supply is not expected to exceed the voluntary threshold limit but expenses to be incurred within the next 30 days are expected exceed the voluntary registration limit.

-

Article (21): Tax De-Registration Cases

A Registrant shall apply to the Authority for Tax Deregistration in any of the following cases:-

-

- If he stops making Taxable Supplies.

- If the value of the Taxable Supplies made over a period of 12 consecutive months is less than the Voluntary/Mandatory Registration Threshold limit.

-

-

-

- Paid all due taxes payable by him;

- paid all Administrative Penalties due by him;

- Filed all the return required to be filed under Decree Law or Tax procedure Law.

-

-

-

- If the Persons who are registered as a Tax Group no longer meet the requirements for registration as a Tax Group in accordance with the Decree-Law.

- If there is no longer an association based on economic, financial and regulatory practices.

- If there are serious grounds for believing that if the registration as a Tax Group is permitted to continue, it would enable Tax Evasion or would significantly decrease Tax paid to the Authority.

-

**************************************************************

Disclaimer All rights reserved. No part of this Article may be reproduced, stored in a retrieval system, or transmitted, in any form, or by any means, electronic, mechanical, photocopying, recording, or otherwise without prior permission, in writing, from the author. About Author

Author of this article is CA Deepak Bharti who is member of ICAI. Currently he is working as partner in M/s N A V & Co. Chartered Accountants, handling the Corporate Compliance and Legal Department. He can be reached [email protected]. Suggestions/comments are most welcome.

About Author

Author of this article is CA Deepak Bharti who is member of ICAI. Currently he is working as partner in M/s N A V & Co. Chartered Accountants, handling the Corporate Compliance and Legal Department. He can be reached [email protected]. Suggestions/comments are most welcome.About Author

CA Deepak Bharti

na

na

na na, Delhi, India

na, Delhi, India 12

12Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.