Relief to Wipro: Dept cannot take coercive steps for Tax Recovery when appeal is still pending with Tribunal

Relief to Wipro: Dept cannot take coercive steps for Tax Recovery when appeal is still pending with Tribunal The Company (M/S WIPRO LTD) is engaged i…

Table of Contents

Relief to Wipro: Dept cannot take coercive steps for Tax Recovery when appeal is still pending with Tribunal

The Company (M/S WIPRO LTD) is engaged in the business of information technology services including the sale of hardware and software, the sale of consumer products and supply and installation of solar power generation plant.

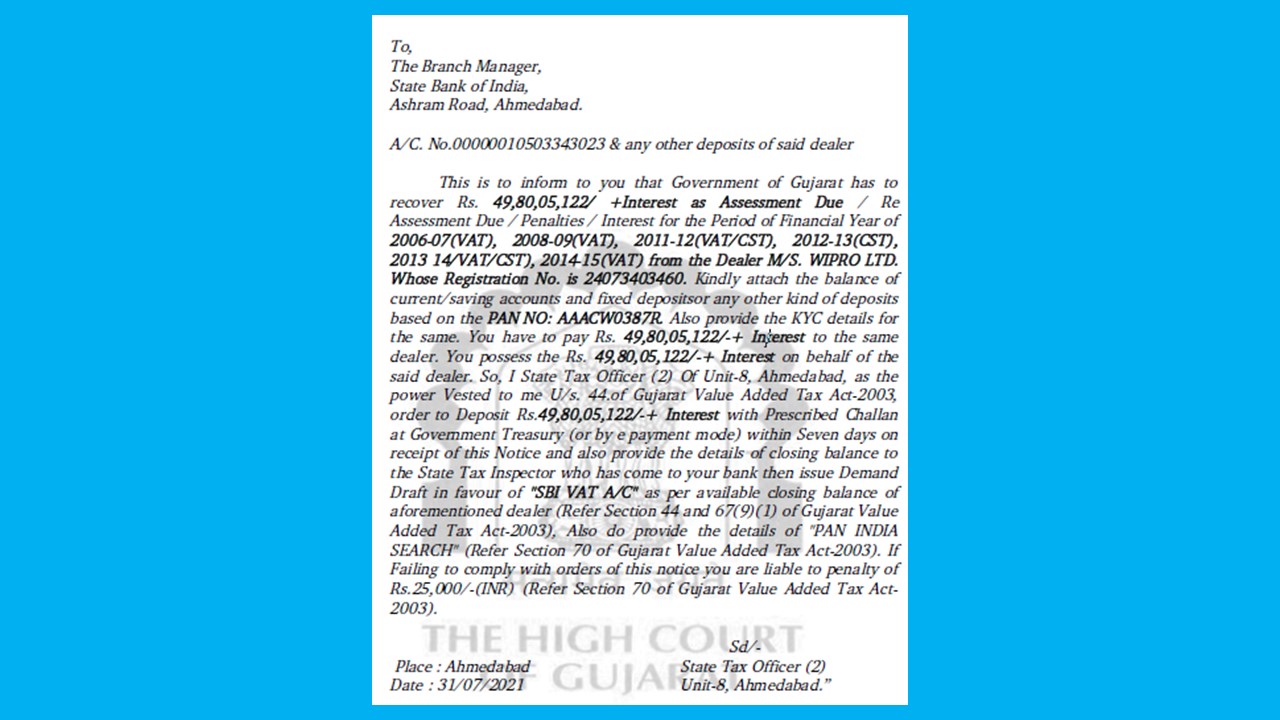

The subject matter of challenge is the legality and validity of the notice issued by the State Tax Officer-II, Unit – 8, Ahmedabad dated 31st July 2021 to the Branch Manager, State Bank of India, Ashram Road, Ahmedabad. The Notice is given below for reference:

Mr. Tushar Hemani, the learned counsel of Appellant Wipro Ltd. made the following submissions:

“(i) Indisputably, the respondent No.3 has not invoked the power under Section 45 of the VAT Act to attach the bank accounts of the writ applicant No.1 during the pendency of any proceedings of assessment or reassessment of turnover escaping assessment.

(ii) The respondent No.3 has failed to frame an opinion for the purpose of protecting the interest of the government revenue by attaching the bank accounts of the writ applicant no.1.

(iii) Further, the respondent No.3 has not brought on record any tangible material on the basis of which he would have framed an opinion that the writ applicant No.1 is likely to defeat the demand and therefore attachment is necessary for protecting the interest of government revenue.

(iv) The respondent No.3 has not served copy of order of attachment to the writ applicant No.1.

(v) Further, a final demand or liability against the petitioner No.1 has not been finalized so far because appeals together with stay applications under the VAT Act and the Central Act, for the periods for which bank accounts have been attached, are pending before the appellate authorities including VAT Tribunal.

Further, it is submitted that without following procedure prescribed under Section 44 of the VAT Act the respondent No.3 has initiated recovery proceedings under the said section and threatened the bank managers of the said banks to issue Demand Draft of Rs. 49,80,05,122/- + interest in favour of “SBI VAT A/C” from account of the writ applicant Appellant.

(i) The respondent No.3 has initiated coercive third party recovery proceedings under Section 44(1)(b) of the VAT Act against the writ applicant No.1 during the pendency of its appeals and stay application filed therein under the VAT Act and the Central Act.

(ii) The respondent No.3 has not served copy of notices dated 31.07.2021 and 02.08.2021 to the writ applicant No.1 though it is a mandatory requirement under Section 44(1) of the VAT Act.

(iii) The respondent No.3 has failed to provide the calculation on the basis of which he has determined dues of Rs.49,80,05,122/- + interest for the period 2006-07 (VAT), 2008-09 (VAT), 2011-12 (VAT/CST), 2012-13(CST), 2013-14(VAT/CST), 2014-15(VAT).”

Mr. Tushar Hemani, the learned counsel of Appellant Wipro Ltd. made the following submissions:

“(i) Indisputably, the respondent No.3 has not invoked the power under Section 45 of the VAT Act to attach the bank accounts of the writ applicant No.1 during the pendency of any proceedings of assessment or reassessment of turnover escaping assessment.

(ii) The respondent No.3 has failed to frame an opinion for the purpose of protecting the interest of the government revenue by attaching the bank accounts of the writ applicant no.1.

(iii) Further, the respondent No.3 has not brought on record any tangible material on the basis of which he would have framed an opinion that the writ applicant No.1 is likely to defeat the demand and therefore attachment is necessary for protecting the interest of government revenue.

(iv) The respondent No.3 has not served copy of order of attachment to the writ applicant No.1.

(v) Further, a final demand or liability against the petitioner No.1 has not been finalized so far because appeals together with stay applications under the VAT Act and the Central Act, for the periods for which bank accounts have been attached, are pending before the appellate authorities including VAT Tribunal.

Further, it is submitted that without following procedure prescribed under Section 44 of the VAT Act the respondent No.3 has initiated recovery proceedings under the said section and threatened the bank managers of the said banks to issue Demand Draft of Rs. 49,80,05,122/- + interest in favour of “SBI VAT A/C” from account of the writ applicant Appellant.

(i) The respondent No.3 has initiated coercive third party recovery proceedings under Section 44(1)(b) of the VAT Act against the writ applicant No.1 during the pendency of its appeals and stay application filed therein under the VAT Act and the Central Act.

(ii) The respondent No.3 has not served copy of notices dated 31.07.2021 and 02.08.2021 to the writ applicant No.1 though it is a mandatory requirement under Section 44(1) of the VAT Act.

(iii) The respondent No.3 has failed to provide the calculation on the basis of which he has determined dues of Rs.49,80,05,122/- + interest for the period 2006-07 (VAT), 2008-09 (VAT), 2011-12 (VAT/CST), 2012-13(CST), 2013-14(VAT/CST), 2014-15(VAT).”

Mr. Tushar Hemani, the learned counsel of Appellant Wipro Ltd. made the following submissions:

“(i) Indisputably, the respondent No.3 has not invoked the power under Section 45 of the VAT Act to attach the bank accounts of the writ applicant No.1 during the pendency of any proceedings of assessment or reassessment of turnover escaping assessment.

(ii) The respondent No.3 has failed to frame an opinion for the purpose of protecting the interest of the government revenue by attaching the bank accounts of the writ applicant no.1.

(iii) Further, the respondent No.3 has not brought on record any tangible material on the basis of which he would have framed an opinion that the writ applicant No.1 is likely to defeat the demand and therefore attachment is necessary for protecting the interest of government revenue.

(iv) The respondent No.3 has not served copy of order of attachment to the writ applicant No.1.

(v) Further, a final demand or liability against the petitioner No.1 has not been finalized so far because appeals together with stay applications under the VAT Act and the Central Act, for the periods for which bank accounts have been attached, are pending before the appellate authorities including VAT Tribunal.

Further, it is submitted that without following procedure prescribed under Section 44 of the VAT Act the respondent No.3 has initiated recovery proceedings under the said section and threatened the bank managers of the said banks to issue Demand Draft of Rs. 49,80,05,122/- + interest in favour of “SBI VAT A/C” from account of the writ applicant Appellant.

(i) The respondent No.3 has initiated coercive third party recovery proceedings under Section 44(1)(b) of the VAT Act against the writ applicant No.1 during the pendency of its appeals and stay application filed therein under the VAT Act and the Central Act.

(ii) The respondent No.3 has not served copy of notices dated 31.07.2021 and 02.08.2021 to the writ applicant No.1 though it is a mandatory requirement under Section 44(1) of the VAT Act.

(iii) The respondent No.3 has failed to provide the calculation on the basis of which he has determined dues of Rs.49,80,05,122/- + interest for the period 2006-07 (VAT), 2008-09 (VAT), 2011-12 (VAT/CST), 2012-13(CST), 2013-14(VAT/CST), 2014-15(VAT).”

Order of Court

In the absence of any debtor–creditor relationship, the department could not have asked the bank to debit the accounts of the writ applicant – company and credit a particular amount as specified in the notices to the treasury of the State Government. 18 We may also observe that ordinarily, when appeals are pending before the first appellate authority or the Tribunal, as the case may be, with an application seeking stay towards the recovery of the tax, then, in such circumstances, the department should not proceed to take coercive steps for the recovery of the amount incurred by the dealer under the GVAT Act. This statement of ours should not be construed as an absolute proposition of law, but, the department is expected to at least wait for the final outcome of the appeals on their own merits, more particularly, when the appeals are already admitted. 19 The Administrative directions for fulfilling recovery targets for the collection of revenue should not be at the expense of foreclosing the remedies which are available to assessees for challenging the correctness of a demand. The sanctity of the rule of law must be preserved. The remedies which are legitimately open in law to an assessee to challenge a demand cannot be allowed to be foreclosed by a hasty recourse to coercive powers. Assessing Officers and appellate authorities perform quasi-judicial functions under the GVAT Act, 2003. To Read Judgement Download PDF Given Below:About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts