Renting of residential premises: RCM Applicability on service received by registered person from registered person:

CBIC vide NN. 05/2022-CTR dated 13 July 2022 service by way of renting residential dwelling to registered person will attract GST under Reverse charge mechanism

GST on Renting of residential premises

Table of Contents

Renting of residential premises: RCM Applicability on service received by registered person from registered person

The Applicant has taken on rent certain premises at New Delhi and Jajpur in Odisha, as guest house. The guest houses are used to provide food and accommodation for the employees of the company who visit New Delhi for official purpose and also for the employees who visit mining office at Jajpur. While one of the apartments is taken on rent from a registered person, other is taken from unregistered person. In both the cases the houses taken on rent for guest house purpose are in the residential area and used by the Applicant Company for guest house of its employees.

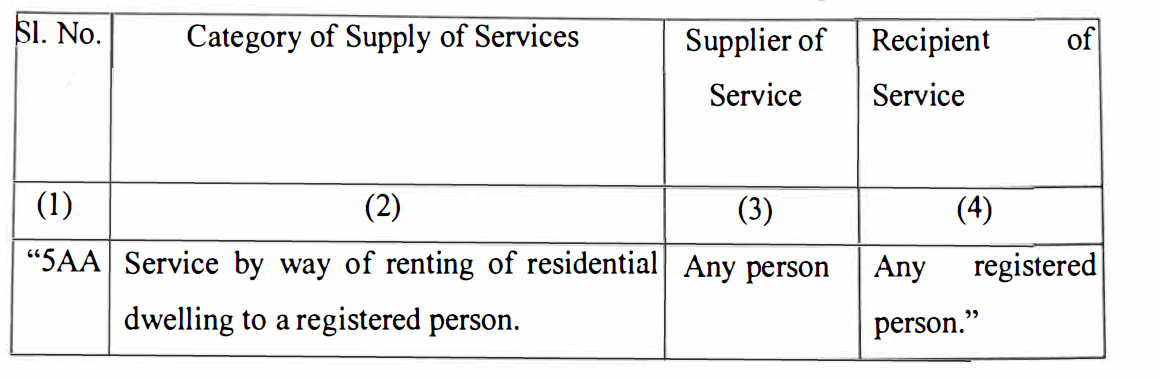

From the above, it is clear that GST will be applicable even if the residential property is rented out to a registered person w.e.f. 18th July 2022. Liability to pay GST @ 18% under the reverse charge mechanism will arise on the recipient (tenant), if he is a registered person under GST with no other condition.

Further, It may be noted that type or nature/purpose of use of residential dwelling i.e. for residence or otherwise by the recipient, has not been a condition in the said RCM notification. Hence, service of renting of residential dwelling to a registered person, would attract RCM irrespective of the nature of use.

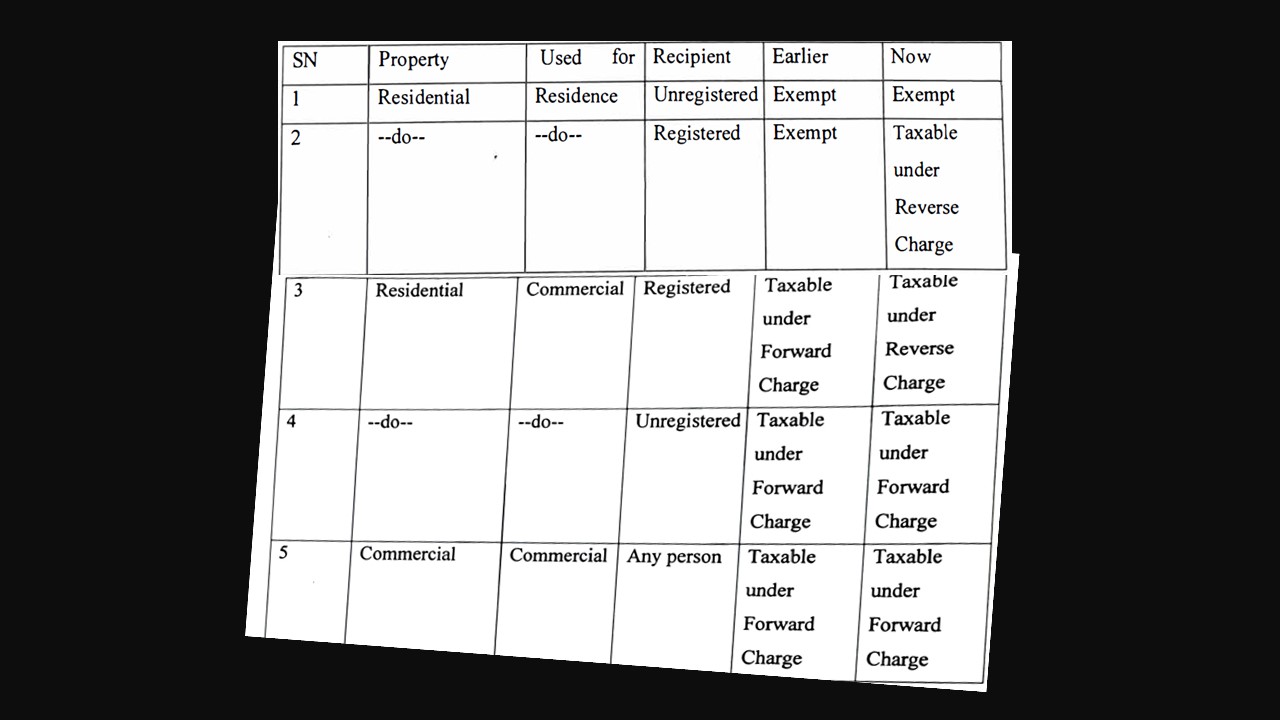

For an easy understanding, the above-mentioned implications have been tabulated below.

From the above, it is clear that GST will be applicable even if the residential property is rented out to a registered person w.e.f. 18th July 2022. Liability to pay GST @ 18% under the reverse charge mechanism will arise on the recipient (tenant), if he is a registered person under GST with no other condition.

Further, It may be noted that type or nature/purpose of use of residential dwelling i.e. for residence or otherwise by the recipient, has not been a condition in the said RCM notification. Hence, service of renting of residential dwelling to a registered person, would attract RCM irrespective of the nature of use.

For an easy understanding, the above-mentioned implications have been tabulated below.

Question:

Whether Service Received by a registered person by way of renting of residential premises used as guesthouse of the registered person is subject to GST under Forward Charge Mechanism, (FCM) or Reverse Charge Mechanism? The CBIC, vide notification No. 05/2022-Central Tax (Rate) dated the 13th July, 2022 notified that with effect from 18th July 2022, service by way of renting of residential dwelling to a registered person shall be attracting GST under RCM (Reverse charge mechanism). The relevant extract of the instant notification is reproduced here under:

From the above, it is clear that GST will be applicable even if the residential property is rented out to a registered person w.e.f. 18th July 2022. Liability to pay GST @ 18% under the reverse charge mechanism will arise on the recipient (tenant), if he is a registered person under GST with no other condition.

Further, It may be noted that type or nature/purpose of use of residential dwelling i.e. for residence or otherwise by the recipient, has not been a condition in the said RCM notification. Hence, service of renting of residential dwelling to a registered person, would attract RCM irrespective of the nature of use.

For an easy understanding, the above-mentioned implications have been tabulated below.

About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.