Restriction in Input tax credit availment : New Rule 36(4) of CGST Rule, 2017

Restriction in Input tax credit availment : New Rule 36(4) of CGST Rule, 2017 As per New Rule 36(4) of CGST Rule, 2017 Input tax credit to b

Table of Contents

Restriction in Input tax credit availment : New Rule 36(4) of CGST Rule, 2017

As per New Rule 36(4) of CGST Rule, 2017 Input tax credit to be availed by a registered person in respect of invoices or debit notes, the details of which have not been uploaded by the suppliers in their GSTR-1 under section 37(1), shall not exceed 20 per cent of the eligible credit available in respect of invoices or debit notes the details of which have been uploaded by the suppliers under section 37(1).

Rule 36(4) is given below for reference:

36(4) Input tax credit to be availed by a registered person in respect of invoices or debit notes, the details of which have not been uploaded by the suppliers under sub-section (1) of section 37, shall not exceed 20 per cent. of the eligible credit available in respect of invoices or debit notes the details of which have been uploaded by the suppliers under sub-section (1) of section 37.

You May Also Refer : 20% ITC restrictions : Understanding Circular No. 123/2019 dated 11.11.2019

• However, concerns were raised in the Notification no. 49/ 2019, dated 09.10.19, over the method of calculating this 20% amount, the cut-off date and also whether it was to be calculated supplier-wise or on a consolidated basis. Therefore, the circular clarifies all these aspects.

You May Also Refer : Consequences if 20% ITC RULE 36 (4) is not followed

Please use the below mentioned example to understand the above mentioned formula

You May Also Refer : Consequences if 20% ITC RULE 36 (4) is not followed

Please use the below mentioned example to understand the above mentioned formula

Disclaimer : The Above Formula and method is based on understanding of Author and is subject to reconciliation of GSTR-2A and Books.

Click Here to Buy CA Final Pendrive Classes at Discounted Rate

For Regular Updates Join : https://t.me/Studycafe

Tags : GST, Rule 36(4), 20% ITC Restriction

• The restriction is not imposed through the common portal and it is the responsibility of the taxpayer that credit is availed in terms of the said rule and therefore, the availment of restricted ITC should be done only on self-assessment basis by the tax payers.

• The 20% cap on the eligible Input Tax Credit will not be calculated supplier-wise and not on on a consolidated basis.

• The provisions is applicable from 9th October, 2019.

Restriction in Input tax credit availment : New Rule 36(4) of CGST Rule, 2017

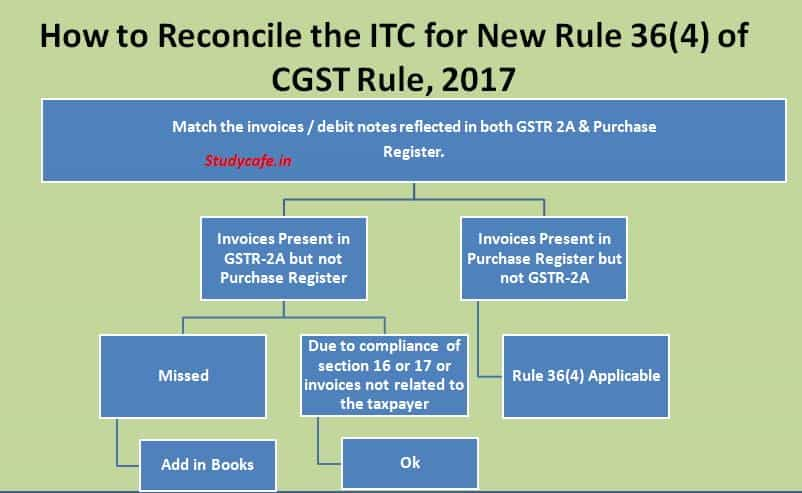

Monthly reconciliation not a easy job : It is not an easy job to reconcile GSTR-2A and Books on monthly basis in the very short time frame that is provided to the tax payer. Also GSTR-2A is a dynamic form. It changes when invoices are corrected , added or omitted. This makes the reconciliation process even more difficult. You May Also Refer : Calculation of Input tax credit as per new GST Rule 36(4) Ineligible credit reflected in GSTR-2A : It is not hundred percent guaranteed that all the credits reflecting in GSTR-2A are eligible. It may contain ineligible and even incorrect credits which can be reconciled only after deep scruitney of books. For computing the eligible credit, the following may be considered as ineligible credit: a) Credit restricted u/s 17(5) or Blocked Credits. b) Inwards Supplies used exclusively in providing the exempt supply. c) Inward Supplies partly used for exempt supply. d) Inward Supplies partly used for non-business purpose. You May Also Refer : Changes in GST ITC Availment ConditionsHow to Reconcile the ITC for New Rule 36(4) of CGST Rule, 2017

- Match the invoices / debit notes reflected in both GSTR 2A & Purchase Register.

- Now There would be Two Scenarios:

- Invoices Present in GSTR-2A but not Purchase Register

- If it is due to compliance of section 16 or 17 or invoices not related to the taxpayer then it is okay.

- If some of the invoices are missed by Accountant, then please Add them.

- Invoices Present in Purchase Register but not GSTR-2A

- This would be Dealt as per Rule 36(4) of CGST Rules.

- Invoices Present in GSTR-2A but not Purchase Register

- How to Calculated availability of ITC as per new GST Rule 36(4)

- Eligible ITC can be calculated as follows : 120% of ITC as per GSTR-2A or ITC as per Books whichever is lowerSo

- Ineligible ITC will be follows : (ITC as per Books-120% of ITC as per GSTR-2A) or Zero whichever is Higher

Please use the below mentioned example to understand the above mentioned formula

| Particulars | ITC as Per Books | ITC as per GSTR-2A | Eligible ITC | Ineligible ITC |

| Case -1 | 100 | 60 | 72 | 28 |

| Case - 2 | 100 | 90 | 100 | 0 |

About Author

Pratibha Goyal

Admin

This Account belongs to Admistrator of Studycafe.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 1080

1080My Recent Articles

- Chartered Accountants Association Embraces Income Tax Faceless Proceedings

- CBDT condones delay in filing form 10IC for AY 20-21: Know upto when to file the form to take concessional tax benefit

- ICAI Announced date of Live Coaching Classes for CA Intermediate Nov 2022 Exam

- ICAI Announced Registration Date for Online Home-Based Practical Training Assessment

- ICAI Released Mock Test Papers Series for May 2022 CA Exam

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts