Distribution of RCM Input Tax Credit by Input Service Distributor:

The Process of Distribution of RCM Input Tax Credit by Input Service Distributor and the major problem associated.

Distribution of RCM ITC by ISD

Claiming Input Tax Credit (ITC) under the Goods and Services Tax (GST) Act is not as seamless as seen in government advertisements. Recently, the government has made the Input Service Distribution (ISD) concept on the distribution of common credit compulsory. Cross-charge for common billing, has been done away with.

Distribution of RCM ITC in ISD

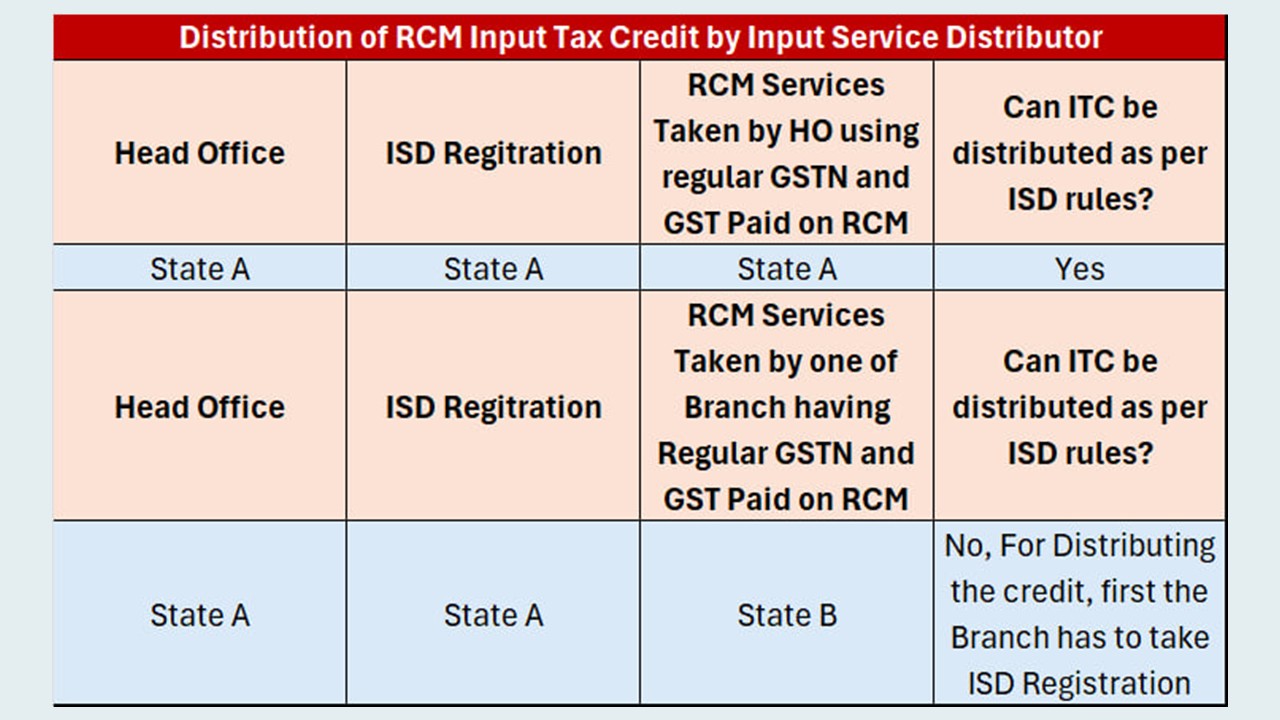

Input Tax Credit (ITC) can be distributed for invoices in respect of services liable to tax under subsection 3 or 4 of section 9.

ISD can also distribute ITC of GST paid under reverse charge if it is first paid by a distinct person and then distributed.

A Registered person in which GST under RCM has been paid on the input services received at multiple recipient locations, having the same PAN and State code as an ISD, is required to issue an invoice or a credit or debit note to transfer the credit of such common input services to the ISD [Rule 39(1A)].

Rule 39(1A) Relevant Text

For the distribution of credit in respect of input services, attributable to one or more distinct persons, subject to levy of tax under sub-section (3) or (4) of section 9, a registered person, having the same PAN and State code as an Input Service Distributor, may issue an invoice or, as the case may be, a credit or debit note as per the provisions of sub-rule(1A) of rule 54 to transfer the credit of such common input services to the Input Service Distributor, and such credit shall be distributed by the said Input Service Distributor in the manner as provided in sub-rule (1).

The invoice/DN/CN issued by a registered person to ISD for the transfer of GST paid under RCM shall contain the details as per Rule 54(1)(A)(a).

Rule 54(1)(A)(a) Relevant Text

(1A) (a) A registered person, having the same PAN and State code as an Input Service Distributor, may issue an invoice or, as the case may be, a credit or debit note to transfer the credit of common input services to the Input Service Distributor, which shall contain the following details:-

i. name, address and Goods and Services Tax Identification Number of the registered person having the same PAN and same State code as the Input Service Distributor;

ii. a consecutive serial number not exceeding sixteen characters, in one or multiple series, containing alphabets or numerals or special characters -hyphen or dash and slash symbolised as "-'' and "/" respectively, and any combination thereof, unique for a financial year;

iii. date of its issue;

iv. Goods and Services Tax Identification Number of supplier of common service and original invoice number whose credit is sought to be transferred to the Input Service Distributor;

v. name, address and Goods and Services Tax Identification Number of the Input Service Distributor;

vi. taxable value, rate and amount of the credit to be transferred; and

vii. signature or digital signature of the registered person or his authorised representative.

Let us understand this with the help of an example:

Lawyer Services Taken by Organization in Head Office in State A. However, the subject matter of litigation pertains to all the branches in the country. The Organization has a Regular GST Number in State A. The organization also has ISD registration in State A. In this case:

- First, GST will be paid under RCM Using Regular GSTN

- Regular GSTN will then raise Invoice to ISD GSTN

- The GST then can be distributed by ISD GSTN to various branches in whole organization.

About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.