Show Cause Notice without Factual allegation is Vague:

The Allahabad HC in the matter of Hindustan Paper Machinery Industries Vs. Commissioner Cgst has held that Show Cause Notice without Factual allegation is Vague.

Show Cause Notice

Show Cause Notice without Factual allegation is Vague

The High Court of Allahabad in the matter of Hindustan Paper Machinery Industries Vs. Commissioner Cgst has held that Show Cause Notice without Factual allegation is Vague.

Present writ petition has been filed against the order dated 9.8.2023 passed by the Superintendent, CGST Range14, Division IIIrd, Ghaziabad. By that order the said authority has cancelled the registration of the petitioner under the Central Goods and Services Tax Act, 2017 (hereinafter referred to as ‘the Act’).

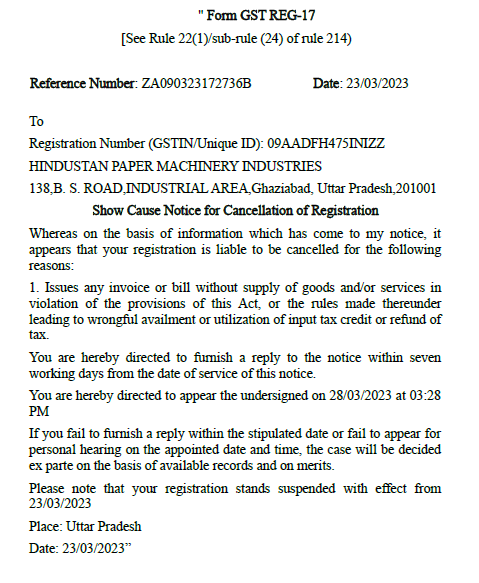

Admittedly the petitioner had obtained registration under the Act. He was issued a show-cause notice dated 23.3.2023 seeking to cancel that registration. For ready reference that notice reads as below:-

The petitioner responded to the notice vide its reply dated 28.3.2023. On such notice and reply furnished thereto, the impugned order dated 9.8.2023 has been passed.

From a bare reading of the notice, reply furnished thereto and the impugned order it transpires, in the first place a wholly non-speaking show-cause notice was issued to the petitioner. Besides making reference to the statutory requirement/ obligation on a registered person to issue a tax invoice only against actual business transaction, no fact allegation was made in that notice of any violation/ infringement of that statutory requirement, committed by the petitioner. Neither the date or detail of the tax invoice nor the goods involved nor their value etc. nor the purchaser were disclosed. Even the period during which the law may have been allegedly infringed by the petitioner, was not specified in the show-cause notice. At the same time, the said communication suspended the registration of the petitioner.

Seen in that light, though the petitioner's reply dated 28.3.2023 may also be described as vague at the same time it is difficult to accept that an adverse conclusion may have been drawn against the petitioner solely on that basis. Unless the show-cause notice had made any fact allegation against the petitioner, the vagueness of the reply may remain inconsequential.

Cancellation of registration has serious impact on a business entity. It causes a direct effect of closure of business. Unless the registration survives, no tax invoice may be issued and no return may easily be filed.

In any case, the order impugned dated 9.8.2023 assigns no reason whatsoever to cancel the petitioner's registration.

In view of the discussion made above, such an order may not survive the test of law. Relegating the petitioner to the forum of alternative remedy in face of undisputed facts noted above may be of no real use or purpose. The writ court regularly relegates petitioners specifically in tax matters, to the forum of the statutory remedy of appeal where minimum compliances of law have been made. However on lack of jurisdiction or violation of principle of natural justice, the writ Court is equally inclined to offer interference to ensure due adherence to the rule of law both by the assessee as also the revenue authority.

Accordingly, in the facts noted above, the objection of the maintainability of the present writ petition is over ruled.

The writ petition is disposed of with a direction, that the suspension of the registration of petitioner may remain in force for a period of one month, in the first place. In the meanwhile, the respondent no.5 may issue a fresh show-cause notice to the petitioner, if so advised within a period of one week from today. The petitioner undertakes to furnish reply thereto within a period of ten days. Upon such reply being filed the respondent no.5 may pass appropriate reasoned order within a period of one week. The rights of the parties shall abide by the final order to be passed in terms of the present order.

If however respondent fails to issue any fresh show-cause notice, the suspension order shall come to an end at the end of one month.

For Official Judgment Download PDF Given Below:

The petitioner responded to the notice vide its reply dated 28.3.2023. On such notice and reply furnished thereto, the impugned order dated 9.8.2023 has been passed.

From a bare reading of the notice, reply furnished thereto and the impugned order it transpires, in the first place a wholly non-speaking show-cause notice was issued to the petitioner. Besides making reference to the statutory requirement/ obligation on a registered person to issue a tax invoice only against actual business transaction, no fact allegation was made in that notice of any violation/ infringement of that statutory requirement, committed by the petitioner. Neither the date or detail of the tax invoice nor the goods involved nor their value etc. nor the purchaser were disclosed. Even the period during which the law may have been allegedly infringed by the petitioner, was not specified in the show-cause notice. At the same time, the said communication suspended the registration of the petitioner.

Seen in that light, though the petitioner's reply dated 28.3.2023 may also be described as vague at the same time it is difficult to accept that an adverse conclusion may have been drawn against the petitioner solely on that basis. Unless the show-cause notice had made any fact allegation against the petitioner, the vagueness of the reply may remain inconsequential.

Cancellation of registration has serious impact on a business entity. It causes a direct effect of closure of business. Unless the registration survives, no tax invoice may be issued and no return may easily be filed.

In any case, the order impugned dated 9.8.2023 assigns no reason whatsoever to cancel the petitioner's registration.

In view of the discussion made above, such an order may not survive the test of law. Relegating the petitioner to the forum of alternative remedy in face of undisputed facts noted above may be of no real use or purpose. The writ court regularly relegates petitioners specifically in tax matters, to the forum of the statutory remedy of appeal where minimum compliances of law have been made. However on lack of jurisdiction or violation of principle of natural justice, the writ Court is equally inclined to offer interference to ensure due adherence to the rule of law both by the assessee as also the revenue authority.

Accordingly, in the facts noted above, the objection of the maintainability of the present writ petition is over ruled.

The writ petition is disposed of with a direction, that the suspension of the registration of petitioner may remain in force for a period of one month, in the first place. In the meanwhile, the respondent no.5 may issue a fresh show-cause notice to the petitioner, if so advised within a period of one week from today. The petitioner undertakes to furnish reply thereto within a period of ten days. Upon such reply being filed the respondent no.5 may pass appropriate reasoned order within a period of one week. The rights of the parties shall abide by the final order to be passed in terms of the present order.

If however respondent fails to issue any fresh show-cause notice, the suspension order shall come to an end at the end of one month.

For Official Judgment Download PDF Given Below:

The petitioner responded to the notice vide its reply dated 28.3.2023. On such notice and reply furnished thereto, the impugned order dated 9.8.2023 has been passed.

From a bare reading of the notice, reply furnished thereto and the impugned order it transpires, in the first place a wholly non-speaking show-cause notice was issued to the petitioner. Besides making reference to the statutory requirement/ obligation on a registered person to issue a tax invoice only against actual business transaction, no fact allegation was made in that notice of any violation/ infringement of that statutory requirement, committed by the petitioner. Neither the date or detail of the tax invoice nor the goods involved nor their value etc. nor the purchaser were disclosed. Even the period during which the law may have been allegedly infringed by the petitioner, was not specified in the show-cause notice. At the same time, the said communication suspended the registration of the petitioner.

Seen in that light, though the petitioner's reply dated 28.3.2023 may also be described as vague at the same time it is difficult to accept that an adverse conclusion may have been drawn against the petitioner solely on that basis. Unless the show-cause notice had made any fact allegation against the petitioner, the vagueness of the reply may remain inconsequential.

Cancellation of registration has serious impact on a business entity. It causes a direct effect of closure of business. Unless the registration survives, no tax invoice may be issued and no return may easily be filed.

In any case, the order impugned dated 9.8.2023 assigns no reason whatsoever to cancel the petitioner's registration.

In view of the discussion made above, such an order may not survive the test of law. Relegating the petitioner to the forum of alternative remedy in face of undisputed facts noted above may be of no real use or purpose. The writ court regularly relegates petitioners specifically in tax matters, to the forum of the statutory remedy of appeal where minimum compliances of law have been made. However on lack of jurisdiction or violation of principle of natural justice, the writ Court is equally inclined to offer interference to ensure due adherence to the rule of law both by the assessee as also the revenue authority.

Accordingly, in the facts noted above, the objection of the maintainability of the present writ petition is over ruled.

The writ petition is disposed of with a direction, that the suspension of the registration of petitioner may remain in force for a period of one month, in the first place. In the meanwhile, the respondent no.5 may issue a fresh show-cause notice to the petitioner, if so advised within a period of one week from today. The petitioner undertakes to furnish reply thereto within a period of ten days. Upon such reply being filed the respondent no.5 may pass appropriate reasoned order within a period of one week. The rights of the parties shall abide by the final order to be passed in terms of the present order.

If however respondent fails to issue any fresh show-cause notice, the suspension order shall come to an end at the end of one month.

For Official Judgment Download PDF Given Below:About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts