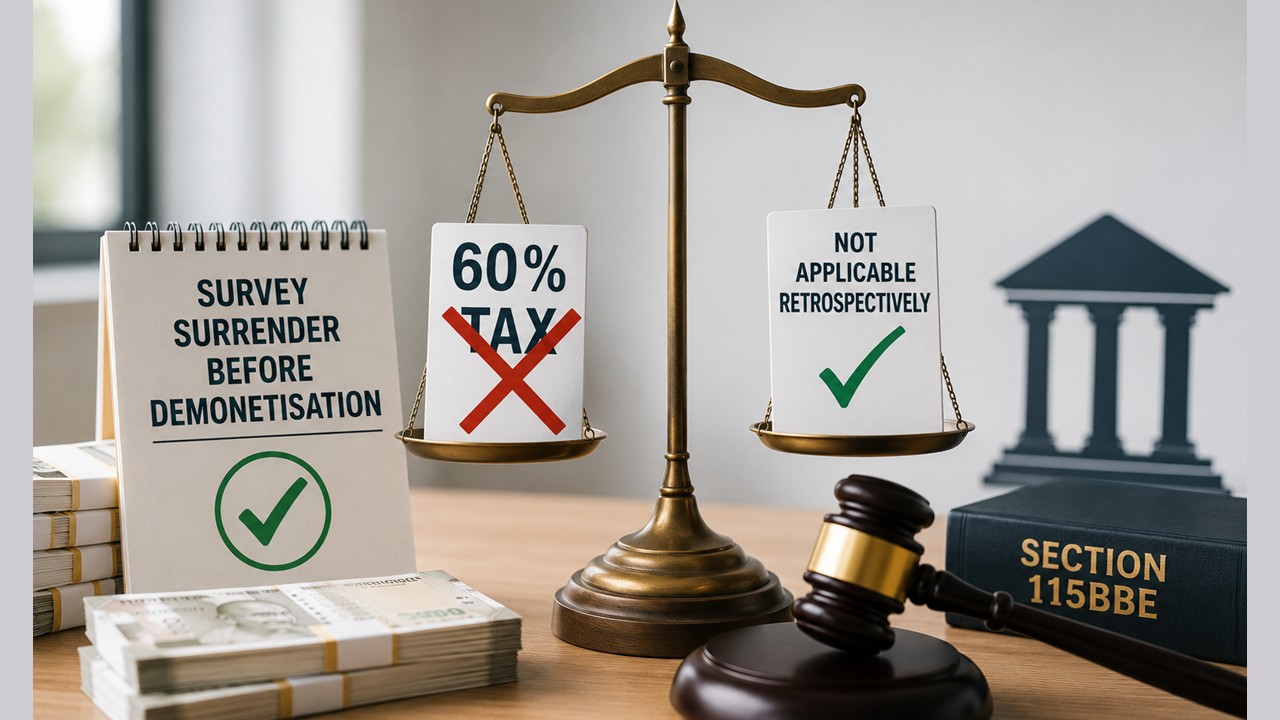

Survey Surrender Made Before Demonetisation; ITAT Rules Higher 60% Tax Under Amended Section 115BBE Cannot Be Applied Retrospectively:

ITAT holds enhanced Section 115BBE tax rate cannot apply to pre-amendment survey disclosures.

Higher tax rate applicable only to post-April 2017 transactions.

The Delhi Bench of the Income Tax Appellate Tribunal (ITAT) partly allowed the appeal of Vijay Kumar Bansal, proprietor of M/s Vishnu Laxmi Marbel, holding that income surrendered during a survey conducted before 1 April 2017 could not be subjected to the enhanced tax rate under Section 115BBE introduced by the Taxation Laws (Second Amendment) Act, 2016.

A survey under Section 133A was conducted at the assessee’s business premises on 16 September 2016. During the survey, excess stock worth Rs.41.29 lakh and excess cash of Rs.9.69 lakh were found. The assessee surrendered Rs.51 lakh, comprising Rs.41.30 lakh on account of stock discrepancy and Rs.9.70 lakh on account of excess cash, subject to no penal action. The surrendered income was duly included in the return of income filed for AY 2017-18.

During assessment proceedings, the Assessing Officer accepted the returned income but treated the surrendered amount as deemed income and taxed it under Section 115BBE at 60%. The CIT(A) upheld the action.

Before the Tribunal, the assessee challenged the assessment on jurisdictional grounds, contending that the scrutiny notice under Section 143(2) was issued by a non-jurisdictional officer, the case was transferred without an order under Section 127, and the notice was not in the prescribed format.

The Tribunal rejected these objections. It noted that the assessee had filed the return before the ITO, Jind and had participated in the assessment proceedings without raising any objection regarding jurisdiction. Relying on the Supreme Court’s decision in Deputy Commissioner of Income-tax (Exemption) v. Kalinga Institute of Industrial Technology, the Tribunal held that Section 124(3)(a) barred the assessee from challenging jurisdiction after participating in the proceedings. It further observed that both the ITO, Jind and DCIT, Bhiwani were under the same administrative charge, making a transfer order under Section 127 unnecessary.

The Tribunal also rejected the argument that the Section 143(2) notice was invalid because it was not issued in the CBDT-prescribed format, noting that the issue stood covered against the assessee by the Delhi High Court's ruling in Bharat Bansal v. National Faceless Assessment Centre.

However, on the issue of taxation under Section 115BBE, the Tribunal accepted the assessee’s plea. Referring to the decision of the S.M.I.L.E. Microfinance Ltd. v. ACIT, it held that the enhanced provisions of Section 115BBE would apply only to transactions occurring on or after 1 April 2017. Since the excess stock and cash were discovered during a survey conducted on 16 September 2016, the surrendered income related to a period prior to the amendment.

Thus, the Tribunal directed the Assessing Officer to tax the surrendered income under the normal provisions of the Income-tax Act without invoking the enhanced tax rate under Section 115BBE. While the jurisdictional and other legal challenges were dismissed, relief was granted on the issue of taxation of the surrendered income.

To Read Full Order, Download PDF Given Below.

About Author

Meetu Kumari

Content Manager

Studycafe

Studycafe Jodhpur, Rajasthan, India

Jodhpur, Rajasthan, India 2264

2264My Recent Articles

- ITAT Condones 302-Day Delay, Restores Salary Assessment for Fresh VerificationPremium

- ITAT Condones Delay After Tax Consultant's Death, Restores Appeals for Fresh HearingPremium

- ITAT Remands Salary Addition, Says Taxability Depends on Salary Becoming Due, Not Mere ReceiptPremium

- ITAT Deletes TP Royalty Adjustment, Orders Fresh Review of Commission BenchmarkingPremium

- ITAT Quashes Reassessment Over Unsigned Section 148 Notice Issued to AssesseePremium

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts