TCS Rate Chart FY 2025-26 | AY 2026-27:

TCS Rate Chart FY 2025-26 | AY 2026-27 as updated by Finance Bill 2025 TCS Rate Chart TCS Rate Chart FY 2025-26 | AY 2026-27 as updated by Finance Bill 2025

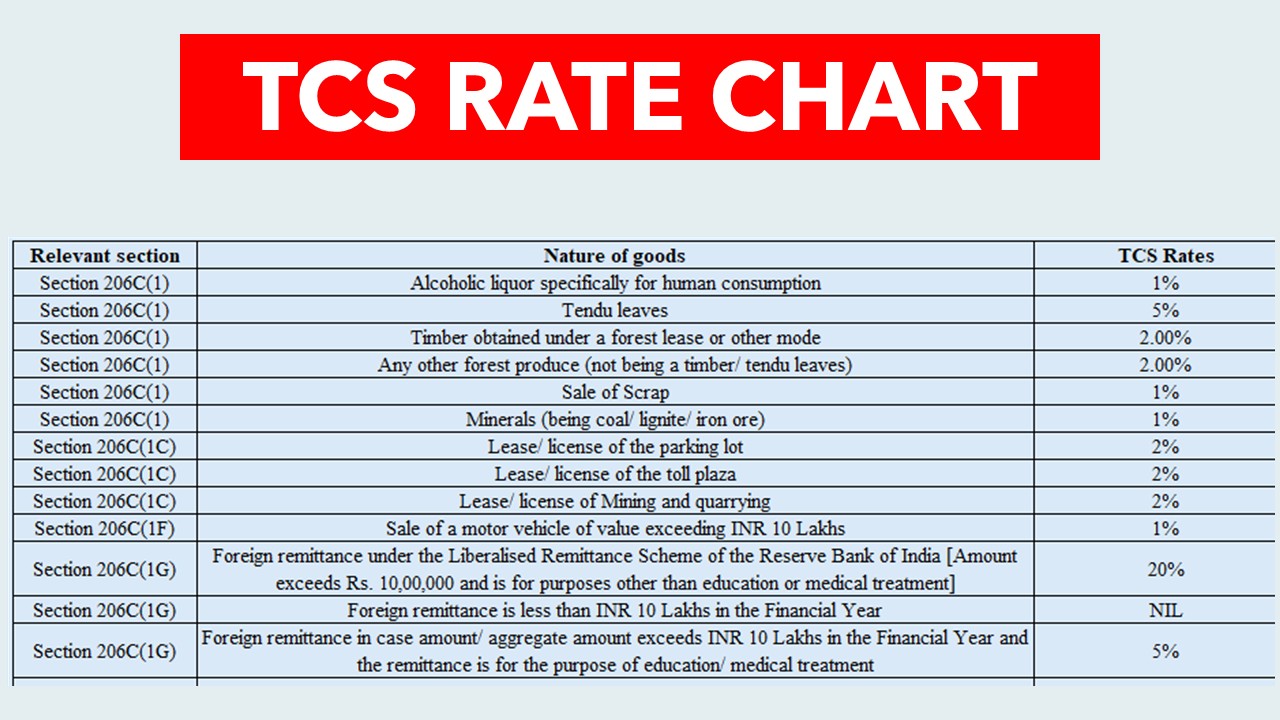

TCS Rate Chart

TCS Rate Chart FY 2025-26 | AY 2026-27

Here is the TCS rate chart for Financial Year 2025-26 or Assessment Year 2026-27. This Rate Chart incorporates proposals of the Finance Bill 2025 as well. Readers can also download the chart in pdf from the Download Tab given at the end.

Please note that readers can also download the chart in Pdf from the Download Tab given below.

| Relevant section | Nature of goods | TCS Rates |

| Section 206C(1) | Alcoholic liquor specifically for human consumption | 1% |

| Section 206C(1) | Tendu leaves | 5% |

| Section 206C(1) | Timber obtained under a forest lease or other mode | 2.00% |

| Section 206C(1) | Any other forest produce (not being a timber/ tendu leaves) | 2.00% |

| Section 206C(1) | Sale of Scrap | 1% |

| Section 206C(1) | Minerals (being coal/ lignite/ iron ore) | 1% |

| Section 206C(1C) | Lease/ license of the parking lot | 2% |

| Section 206C(1C) | Lease/ license of the toll plaza | 2% |

| Section 206C(1C) | Lease/ license of Mining and quarrying | 2% |

| Section 206C(1F) | Sale of a motor vehicle of value exceeding INR 10 Lakhs | 1% |

| Section 206C(1G) | Foreign remittance under the Liberalised Remittance Scheme of the Reserve Bank of India [Amount exceeds Rs. 10,00,000 and is for purposes other than education or medical treatment] | 20% |

| Section 206C(1G) | Foreign remittance is less than INR 10 Lakhs in the Financial Year | NIL |

| Section 206C(1G) | Foreign remittance in case amount/ aggregate amount exceeds INR 10 Lakhs in the Financial Year and the remittance is for the purpose of education/ medical treatment | 5% |

| Section 206C(1G) | Foreign remittance in case amount/ aggregate amount exceeds INR 10 Lakhs and if the remitted amount is out of the loan that is obtained from Financial Institution u/s 80E for pursuing any education | NIL |

| Section 206C(1G) | Overseas tour program package [Amount upto Rs. 10,00,000] | 5% |

| Section 206C(1G) | Overseas tour program package [Amount exceeds Rs. 10,00,000] | 20% |

| Section 206C(1H) | Sale of any goods of the value/ aggregate of such value exceeding INR 50 Lakhs [applicable only if total sales/ gross receipts/ turnover of the seller exceeds INR 10 Crores during the preceding Financial Year] | Abolished |

| Section 206CC(1) | Non-furnishing of Permanent Account Number (PAN) by the collectee to the collector | Higher of the following – -At twice of the rates as prescribed in the relevant provision; or -5%Notably, the maximum rate of TCS should not exceed 20%. |

| Section 206CCA(1) | Applicable when all of the following conditions are satisfied – - The person has not furnished ITR for the Assessment Year (relevant to the previous year) immediately preceding the Financial Year in which TCS was required to be collected; - The time limit for submitting a return under section 139(1) of the Income Tax Act is expired; and - The total of TDS and TCS is INR 50,000 or more in the respective previous year. | Abolished |

About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.