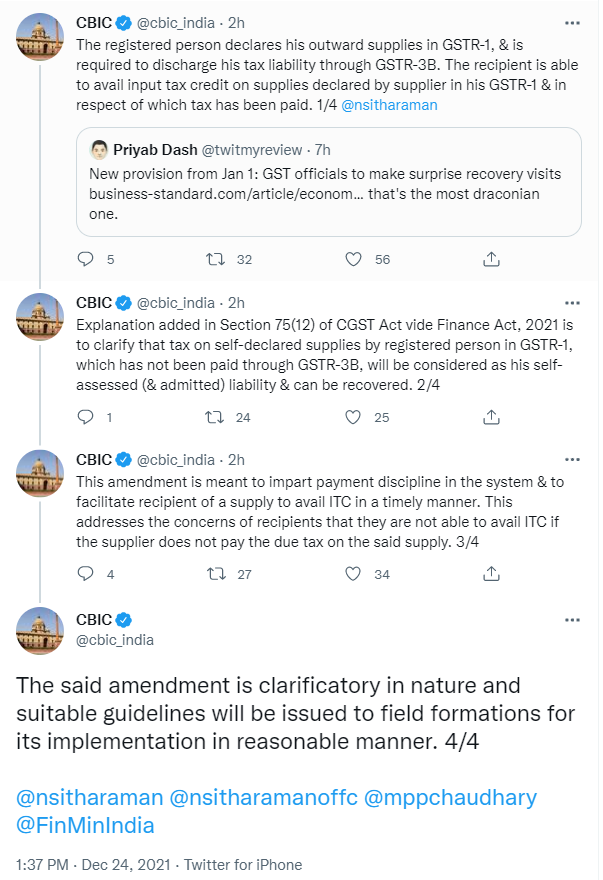

To avail ITC on supplies declared by supplier in his GSTR-1 Registered Person is required to discharge his tax liability through GSTR-3B

To avail ITC on supplies declared by supplier in his GSTR-1 Registered Person is required to discharge his tax liability through GSTR-3B GSTR-1 is us…

To avail ITC on supplies declared by supplier in his GSTR-1 Registered Person is required to discharge his tax liability through GSTR-3B

GSTR-1 is used to declare outbound supplies, while GSTR-3B is used to discharge the registered person's tax liability. On supplies disclosed by the provider in his GSTR-1 and for which tax has been paid, the recipient is eligible to claim input tax credit.

The Finance Act of 2021 added an explanation to Section 75(12) of the CGST Act to clarify that tax on self-declared supply by a registered person in GSTR-1 that has not been paid through GSTR-3B will be deemed his self-assessed (and accepted) responsibility and can be reclaimed.

This amendment is intended to improve payment discipline in the system and make it easier for recipients of supplies to receive ITC in a timely way. This alleviates receivers' concerns that they will be unable to claim ITC if the supplier fails to pay the applicable tax.

The said amendment is clarifying in nature, and appropriate guidance would be supplied to field formations for its reasonable implementation.

About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts