Turnover Limit for Tax Audit Applicability for FY 2022-23:

Tax audit, as the name implies, is an inspection or review of the accounts of any business or profession carried out by taxpayers from an income tax standpoint.

Tax Audit Applicability

Table of Contents

Turnover Limit for Tax Audit Applicability for FY 2022-23

Tax Audit Applicability: Tax audit, as the name implies, is an inspection or review of the accounts of any business or profession carried out by taxpayers from an income tax standpoint. It simplifies the process of calculating income for the purpose of submitting income tax returns.

If a taxpayer's sales, turnover, or gross revenues surpass Rs.1 crore in a fiscal year, he or she is obligated to have a tax audit performed. However, in some other cases, a taxpayer may be forced to have their accounts audited.

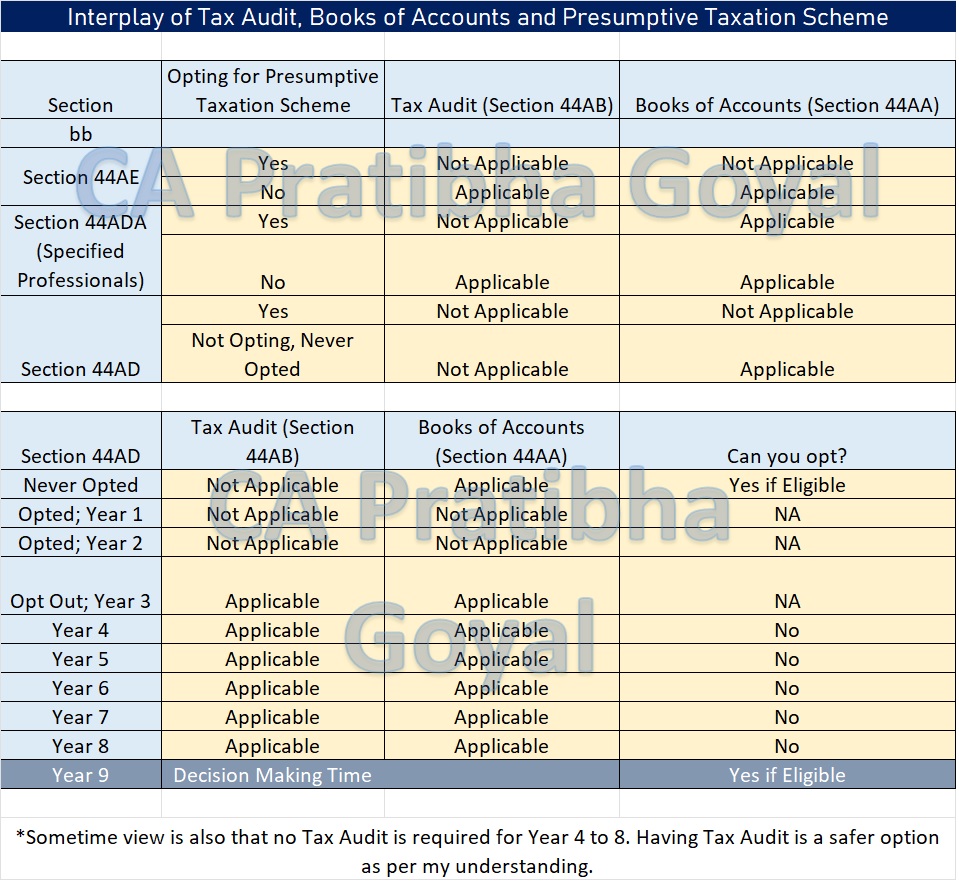

I have made another chart for understanding the Applicability of Tax Audit in case of Presumptive Taxation Scheme.

I have made another chart for understanding the Applicability of Tax Audit in case of Presumptive Taxation Scheme.

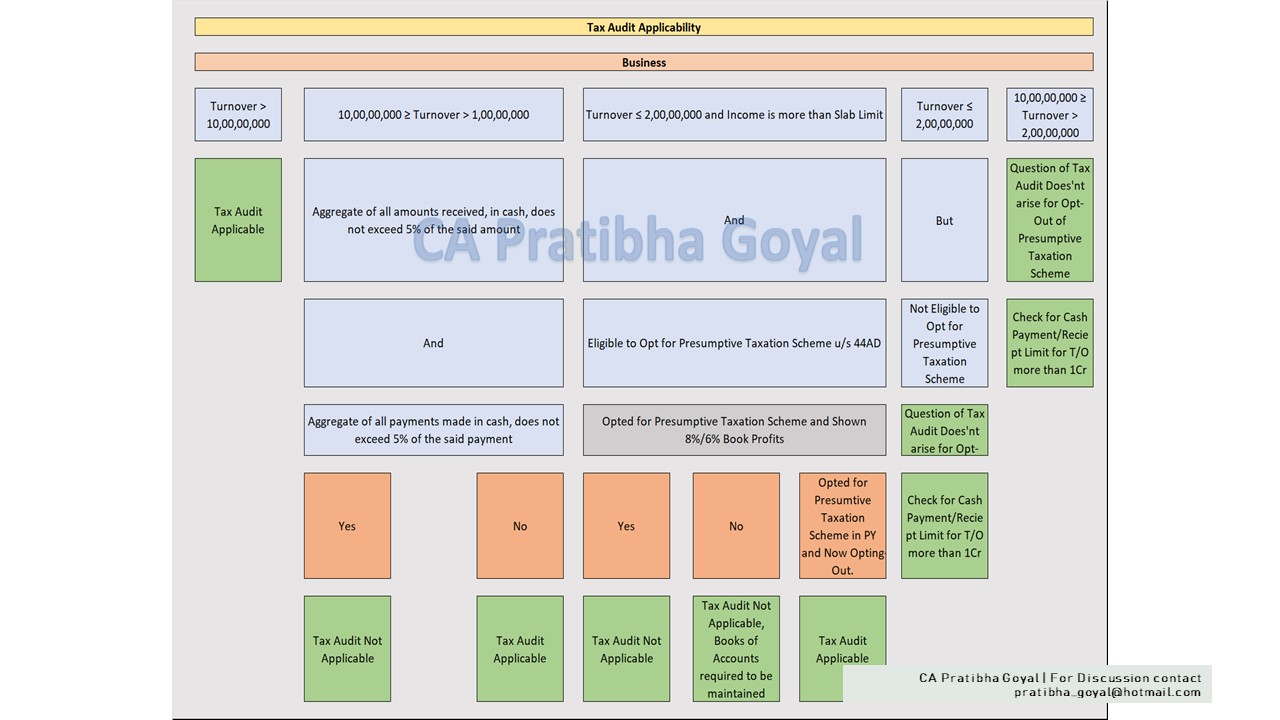

Tax Audit Applicability in case of Business

Case 1: If Turnover > 10,00,00,000 Tax Audit Applicable. Case 2. Turnover Range: 10,00,00,000 ≥ Turnover > 1,00,00,000 The below given conditions needs to be satisfied: The aggregate of all amounts received, in cash, does not exceed 5% of the said amount. And The aggregate of all payments made in cash does not exceed 5% of the said payment. If yes, Tax Audit Not Applicable. If No, Tax Audit Applicable. Case 3. If Turnover ≤ 2,00,00,000 and Taxpayer is Eligible to Opt for Presumptive Taxation Scheme Taxpayer Opted for Presumptive Taxation Scheme and Shown 8%/ 6% Book Profits- If Yes, Tax Audit Not Applicable.

- If No, Tax Audit Not Applicable, Books of Accounts required to be maintained.

I have made another chart for understanding the Applicability of Tax Audit in case of Presumptive Taxation Scheme.

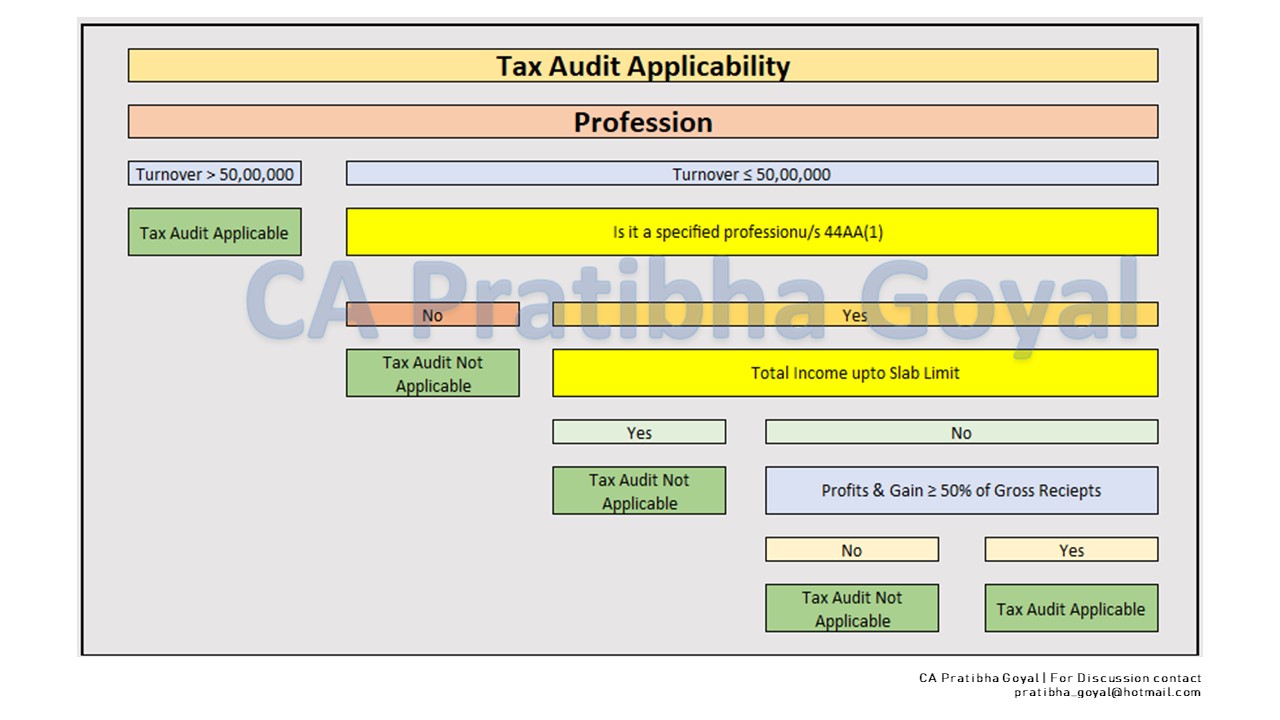

Tax Audit Applicability in Case of Profession

Case 1: If Turnover > 50,00,000 Tax Audit Applicable. Case 2: If Turnover ≤ 50,00,000 And Profits & Gain ≥ 50% of Gross Receipts If Yes, Tax Audit Not Applicable. If No, then check that, if Total Income is upto Slab Limit. Then: If Total Income is upto Slab Limit, then Tax Audit Not Applicable. If Total Income is not upto Slab Limit, then Tax Audit Applicable.About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts