Valuation report by CA based only on basic information provided by management cannot be accepted: ITAT

Valuation report by CA based only on basic information provided by management cannot be accepted: ITAT ITAT in matter of ITO vs LNB Renewable Energy …

Valuation report by CA based only on basic information provided by management cannot be accepted: ITAT

ITAT in matter of ITO vs LNB Renewable Energy (P.) Ltd. observed that during the course of assessment proceedings a valuation report obtained from a Chartered Accountant was filed in support of the said valuation which was not accepted and the matter was referred to the District Valuation Officer. But surprisingly District Valuation Officer denied to have any expertise in the field of valuation of equity shares and ld. AO framed the assessment during the period when the matter was pending before the first appellate authority. The assessee obtained a valuation report from registered valuer dated 14.03.2018 prepared as per Rule 11UA(2)(b) of the I.T Rules justifying the charging of said share premium. The same was considered by ld. CIT(A) and accepted the claim of the assessee.

Further ITAT said that, on perusal of the said valuation report dated 14.03.2018 prepared by registered valuer, we find that brief structure of the company shown in page 2 of the said report of Chapter 1 it is stated that the assessee company has two wholly owned subsidiary companies namely a) LNB Solar Energy Private Limited & b) LNB Wind Energy Private Limited. Further, there are two step down subsidiary of the assessee, in other words LNB Solar Energy Private Limited which is a wholly owned subsidiary of the assessee company, also has two wholly owned subsidiary companies namely a) Palimarwar Solar Projects Private Limited&b) Manifold Agricrops Private Limited.

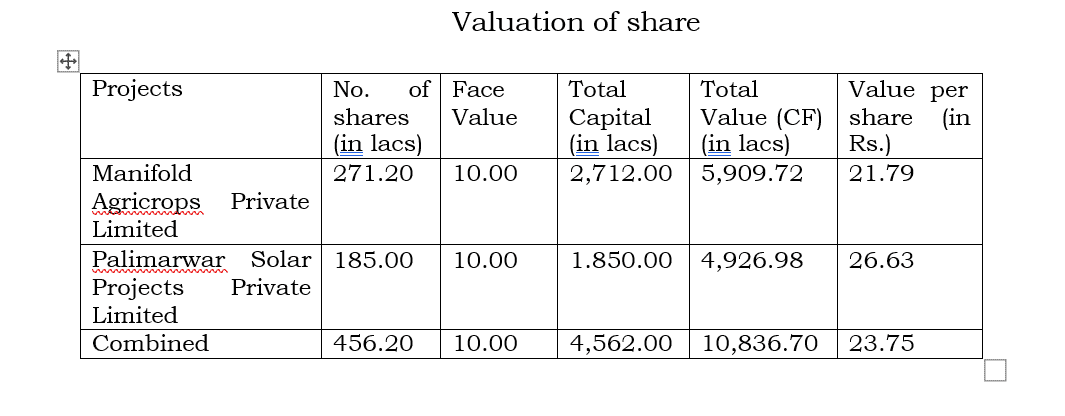

11. Further, from perusal of the said valuation report, we find that the said valuation of assessee company is calculated after considering the net worth of two step down subsidiaries namely

a) Palimarwar Solar Projects Private Limited & b) Manifold Agricrops Private Limited. All throughout the proceedings, the contention of the ld. Counsel for the assessee referring to various judgments is that once there is a report prepared as per Rule 11UA(2)(b) of the I.T Rules, then it has to be accepted and the valuation process so adopted and the results arrived at should not be doubted.

As per ITAT, so far as the preparation of the valuation report and its technical aspects are concerned, we refrain from making any comments. However, it is an admitted fact that for the preparation of such valuation reports by the experts which in this case is a Chartered Accountant, the basic information is supplied by the management and based on such information the valuation reports are prepared. In case wrong information or an incorrect information is inadvertently given, the results so arrived cannot be accepted.

13. In the instant case valuation report prepared by the Chartered Accountant is dated 14.03.2018 and the fair market value of equity share and preference share at Rs.23.75 and 237.50 respectively has been arrived at mainly after considering the net-worth of two step down subsidiaries namely a) Palimarwar Solar Projects Private Limited & b) Manifold Agricrops Private Limited in following manner.

Now, before us the Revenue has pointed out the fact that the assessee company was incorporated on 07.11.2012 and the cut off date for the valuation of share was 16.11.2012. Further, the fact has been placed before us by the Revenue through its grounds of appeal is that the subsidiary companies were acquired on 29.12.2012 & 10.01.2013 which was after the valuation date i.e. 16.11.2012. This fact of acquiring the wholly owned subsidiaries/step down subsidiaries after the cut off date of valuation of share remains uncontroverted by the assessee and there is no whisper about controverting this fact at any stage during the course of assessment proceedings/appellate proceedings both before Ld. CIT(A) and before us.

Based on these facts, we are of the considered view that since the input needed for preparing the valuation report dated 14.03.2018 were not supplied correctly to the expert (CA), the results arrived at in the said valuation report dated 14.03.2018 cannot be accepted. Under these given facts and circumstances of the case we are of the considered view that since the company was incorporated on 07.11.2012 and cut off date of valuation of share was 16.11.2012 and the said acquisition of wholly owned subsidiary and step down subsidiary companies was after the cut off date of valuation of share, therefore as on 16.11.2012, the fair market value of the equity share capital remains at Rs. 10/- and that of the preference share capital remains at Rs. 100/-. Therefore, share premium of Rs. 2.50 per share on issue of equity share capital totalling to Rs. 5 lakh and share premium of Rs. 8 Cr received on issue of preference share capital at Rs. 25 per share along with face value of each equity share at Rs. 10/- and each preference share at Rs.100/- is in excess of the fair market value of Rs. 10/- per equity share and Rs. 100/- per preference share for preference and therefore, provisions of Section 56(2)(viib) of the Act have rightly been invoked by ld. AO for making the addition of Rs. 8.05 Cr received towards share premium in the hands of the assessee. Thus, the finding of ld. CIT(A) is reversed, addition at Rs.8.05 Cr. made by ld. AO is confirmed and ground nos. 1, 2, 3 & 4 of the Revenue’s appeal are allowed.

Click here to read the Order

Now, before us the Revenue has pointed out the fact that the assessee company was incorporated on 07.11.2012 and the cut off date for the valuation of share was 16.11.2012. Further, the fact has been placed before us by the Revenue through its grounds of appeal is that the subsidiary companies were acquired on 29.12.2012 & 10.01.2013 which was after the valuation date i.e. 16.11.2012. This fact of acquiring the wholly owned subsidiaries/step down subsidiaries after the cut off date of valuation of share remains uncontroverted by the assessee and there is no whisper about controverting this fact at any stage during the course of assessment proceedings/appellate proceedings both before Ld. CIT(A) and before us.

Based on these facts, we are of the considered view that since the input needed for preparing the valuation report dated 14.03.2018 were not supplied correctly to the expert (CA), the results arrived at in the said valuation report dated 14.03.2018 cannot be accepted. Under these given facts and circumstances of the case we are of the considered view that since the company was incorporated on 07.11.2012 and cut off date of valuation of share was 16.11.2012 and the said acquisition of wholly owned subsidiary and step down subsidiary companies was after the cut off date of valuation of share, therefore as on 16.11.2012, the fair market value of the equity share capital remains at Rs. 10/- and that of the preference share capital remains at Rs. 100/-. Therefore, share premium of Rs. 2.50 per share on issue of equity share capital totalling to Rs. 5 lakh and share premium of Rs. 8 Cr received on issue of preference share capital at Rs. 25 per share along with face value of each equity share at Rs. 10/- and each preference share at Rs.100/- is in excess of the fair market value of Rs. 10/- per equity share and Rs. 100/- per preference share for preference and therefore, provisions of Section 56(2)(viib) of the Act have rightly been invoked by ld. AO for making the addition of Rs. 8.05 Cr received towards share premium in the hands of the assessee. Thus, the finding of ld. CIT(A) is reversed, addition at Rs.8.05 Cr. made by ld. AO is confirmed and ground nos. 1, 2, 3 & 4 of the Revenue’s appeal are allowed.

Click here to read the Order

Now, before us the Revenue has pointed out the fact that the assessee company was incorporated on 07.11.2012 and the cut off date for the valuation of share was 16.11.2012. Further, the fact has been placed before us by the Revenue through its grounds of appeal is that the subsidiary companies were acquired on 29.12.2012 & 10.01.2013 which was after the valuation date i.e. 16.11.2012. This fact of acquiring the wholly owned subsidiaries/step down subsidiaries after the cut off date of valuation of share remains uncontroverted by the assessee and there is no whisper about controverting this fact at any stage during the course of assessment proceedings/appellate proceedings both before Ld. CIT(A) and before us.

Based on these facts, we are of the considered view that since the input needed for preparing the valuation report dated 14.03.2018 were not supplied correctly to the expert (CA), the results arrived at in the said valuation report dated 14.03.2018 cannot be accepted. Under these given facts and circumstances of the case we are of the considered view that since the company was incorporated on 07.11.2012 and cut off date of valuation of share was 16.11.2012 and the said acquisition of wholly owned subsidiary and step down subsidiary companies was after the cut off date of valuation of share, therefore as on 16.11.2012, the fair market value of the equity share capital remains at Rs. 10/- and that of the preference share capital remains at Rs. 100/-. Therefore, share premium of Rs. 2.50 per share on issue of equity share capital totalling to Rs. 5 lakh and share premium of Rs. 8 Cr received on issue of preference share capital at Rs. 25 per share along with face value of each equity share at Rs. 10/- and each preference share at Rs.100/- is in excess of the fair market value of Rs. 10/- per equity share and Rs. 100/- per preference share for preference and therefore, provisions of Section 56(2)(viib) of the Act have rightly been invoked by ld. AO for making the addition of Rs. 8.05 Cr received towards share premium in the hands of the assessee. Thus, the finding of ld. CIT(A) is reversed, addition at Rs.8.05 Cr. made by ld. AO is confirmed and ground nos. 1, 2, 3 & 4 of the Revenue’s appeal are allowed.

Click here to read the OrderAbout Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts