Vivad se Vishwas Bill, 2020 : Brief Analysis & Discussion

Vivad se Vishwas Bill, 2020 : Brief Analysis & Discussion Honable Finance Minister has introduced, vivad se Vishwas Scheme, in Budget 20

Vivad se Vishwas Bill, 2020 : Brief Analysis & Discussion

Honable Finance Minister has introduced, vivad se Vishwas Scheme, in Budget 2020 in consideration of amount of disputed tax arrears as on 30th November 2019 of Rs.9.32 Lakh crores. This bill will not only help the taxpayer to resolve their disputed tax matters, but also help Govt to collect disputed tax arrears.

Majority of taxpayers whose cases are pending with various Income tax Authorities can avail the benefit of this scheme, subject to certain exceptions.

Applicability of this Scheme

The provisions of this bill are applicable to settle disputes in the cases where the appeals are filed by the taxpayers or the income tax authority, before the Commissioner (Appeals) or Income Tax tribunal or High Court or Supreme Court as on 31 Jan 2020.

The appeal may be against disputed tax, interest or penalty or against the determination of tax amount on default in respect of TDS or TCS.

The cases resolved though this scheme shall be considered final and such cases will not be reopened in any other proceeding of the Income tax act.

Benifit of this Scheme

[caption id="attachment_87268" align="alignnone" width="803"] An Analysis of Vivad se Vishwas Bill, 2020[/caption]

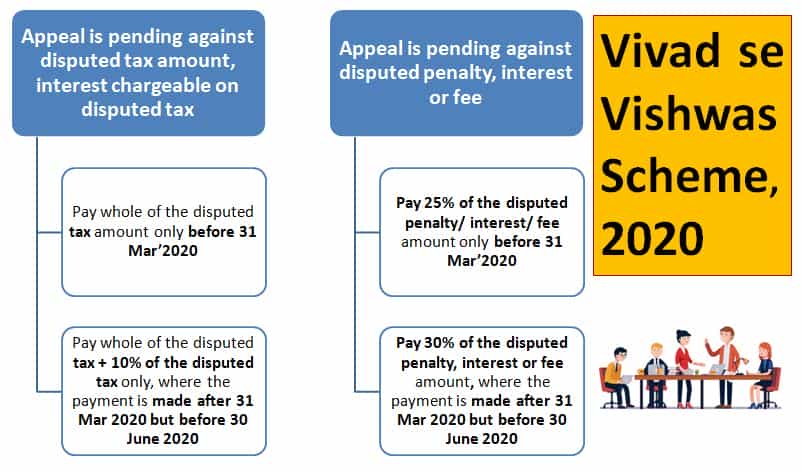

This bill will give a one time opportunity to those taxpayer in whose case an appeal is pending against disputed tax amount, interest chargeable on disputed tax.

1. To pay whole of the disputed tax amount only before 31 Mar’2020 without requiring them to pay interest, fee or fine on it.

Or

2. To pay whole of the disputed tax plus 10% of the disputed tax only, where the payment is made after 31 Mar 2020 but before 30 June 2020 without requiring them to pay interest, fee or fine on it.

This bill will give an opportunity to those taxpayer as well in whose case an appeal is pending against disputed penalty, interest or fee amount

1. To pay 25% of the disputed penalty, interest or fee amount before 31 Mar’2020

or

2. To pay 30% of the disputed penalty, interest or fee amount, where the payment is made after 31 Mar 2020 but before 30 June 2020.

Note that any amount paid by the tax payer in pursuance of this bill will not be refunded back to the taxpayer under any circumstances.

How this Scheme will work?

1. The taxpayers are required to file declaration before the designated authority in such form and manner, as may be prescribed by the Central Government to implement this bill Upon filing the declaration, any appeal pending before Commissioner (Appeals) or Income Tax Tribunal shall be deemed to have withdrawn from the date of receipt of certificate under section 5(1) of this Act from designated authority, where the taxpayer has filed an appeal or petition before the High Court or Supreme Court then he shall withdraw the same.

2. On receipt of the declaration, the designated Authority will determine the amount payable within 15 days of receipt of declaration and grant a certificate containing particulars of the tax arrier and the amount payable

3. The declaration shall pay the amount so determined within 15 days of receipt of the certificate and intimate the details of such payment to the designated Authority.

4. There upon the designated Authority shall pass an order stating that the declarant has paid the amount.

Following tax matters are ineligible for consideration under this scheme

An Analysis of Vivad se Vishwas Bill, 2020[/caption]

This bill will give a one time opportunity to those taxpayer in whose case an appeal is pending against disputed tax amount, interest chargeable on disputed tax.

1. To pay whole of the disputed tax amount only before 31 Mar’2020 without requiring them to pay interest, fee or fine on it.

Or

2. To pay whole of the disputed tax plus 10% of the disputed tax only, where the payment is made after 31 Mar 2020 but before 30 June 2020 without requiring them to pay interest, fee or fine on it.

This bill will give an opportunity to those taxpayer as well in whose case an appeal is pending against disputed penalty, interest or fee amount

1. To pay 25% of the disputed penalty, interest or fee amount before 31 Mar’2020

or

2. To pay 30% of the disputed penalty, interest or fee amount, where the payment is made after 31 Mar 2020 but before 30 June 2020.

Note that any amount paid by the tax payer in pursuance of this bill will not be refunded back to the taxpayer under any circumstances.

How this Scheme will work?

1. The taxpayers are required to file declaration before the designated authority in such form and manner, as may be prescribed by the Central Government to implement this bill Upon filing the declaration, any appeal pending before Commissioner (Appeals) or Income Tax Tribunal shall be deemed to have withdrawn from the date of receipt of certificate under section 5(1) of this Act from designated authority, where the taxpayer has filed an appeal or petition before the High Court or Supreme Court then he shall withdraw the same.

2. On receipt of the declaration, the designated Authority will determine the amount payable within 15 days of receipt of declaration and grant a certificate containing particulars of the tax arrier and the amount payable

3. The declaration shall pay the amount so determined within 15 days of receipt of the certificate and intimate the details of such payment to the designated Authority.

4. There upon the designated Authority shall pass an order stating that the declarant has paid the amount.

Following tax matters are ineligible for consideration under this scheme

- Tax matters pending under section 153A or 153C for any assessment year in relation to Search or assessment of income of any other person

- Where matters in respect of an assessment year where prosecution has been instituted on or before the date of filing declaration

- Where matters related to undisclosed income from any source or undisclosed assets located outside India

- Where matters relating to an assessment of reassessment made on the basis of information received under an agreement referred to in Section 90 or 90A of Income Tax Act.

About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.