West Bengal GST Department implemented Document Identification Number System:

The Directorate of Commercial Taxes of West Bengal has notified Generation and quoting of Document Identification Number (DIN) on communications issued under GST by the officers of the Directorate to tax payers and other concerned persons via issuing Trade Circular.

Document Identification Number System

(i) when any such communication is made through the GSTN portal containing a unique reference number;

(ii) when any communication is made from the offices under the Directorate of Commercial Taxes other than any Charge/Circle/Large Taxpayer Unit/Unit or Zone under Bureau of Investigation;

(iii) when FORM GST MOV-01 and FORM GST MOV-02 are issued manually by the authorized officer who is outside the office while discharging his official duties.

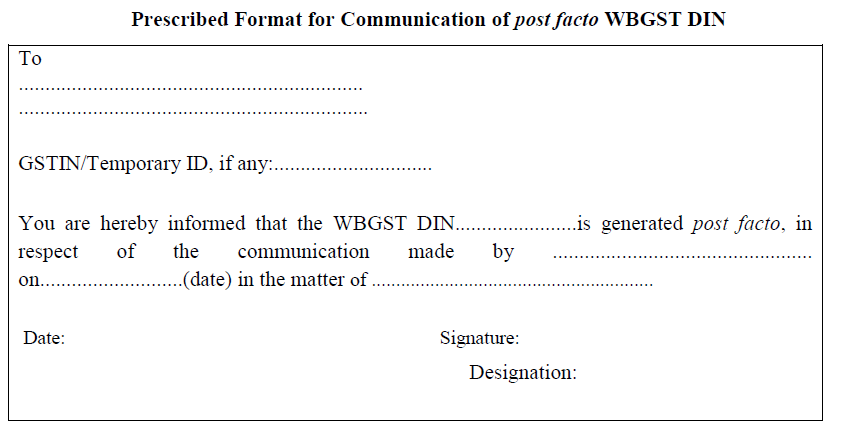

(b) WBGST DIN so generated shall be quoted prominently on the body of communications like summons, arrest memos, search authorizations, inspection notices, recovery proceedings and such other communications relating to a tax payer/taxable person/any person, as the case may be. (c) when the communication is made by e-mail then the WBGST DIN shall be quoted on th body of the e-mail. Notwithstanding anything mentioned in para 2 of this circular, in exceptional cases mentioned below, communications will be made without WBGST DIN:– (a) when there are technical difficulties in generation of WBGST DIN electronically; or (b) when communication regarding investigation/inquiry, verification etc. is required to be issued in short notice or in urgent situations and the authorized officer is outside the office while discharging his official duties: Provided that where the WBGST DIN could not be generated due to reasons specified in clause (a) above, the officer shall generate the corresponding WBGST DIN post facto within three working days from the date when such difficulties are overcome, and communicate such WBGST DIN to the recipient in the prescribed format given below. Provided further that where the WBGST DIN could not be generated due to reasons specified in clause (b) above, the officer shall generate WBGST DIN post facto within three working days from the date of issue of such communication and such WBGST DIN should also be communicated to the recipient in the prescribed format given below. The Commissioner also directs that, subject to para 3 above, any communication, specified in para 2, which does not bear the electronically generated WBGST DIN shall be treated as invalid and shall be deemed to have never been issued.

The WBGST DIN will be generated for the following categories of communication, viz.,

i) Summons

ii) Arrest Memos

iii) Search authorisations

iv) Inspection notices

v) Other communications, such as:

The Commissioner also directs that, subject to para 3 above, any communication, specified in para 2, which does not bear the electronically generated WBGST DIN shall be treated as invalid and shall be deemed to have never been issued.

The WBGST DIN will be generated for the following categories of communication, viz.,

i) Summons

ii) Arrest Memos

iii) Search authorisations

iv) Inspection notices

v) Other communications, such as:

(a) Notice for return default

(b) Notice for interest default

(c) Notice for physical appearance

(d) Notice/request against any mismatch for reconciliation

(e) Intimation for recovery

(f) Intimation for bank garnishee

(g) Request for production of documents/ books of accounts

(h) Any other communication

To Read More Download PDF Given Below:About Author

Reetu

Content Manager

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts