What is IND AS

What is IND AS INTRODUCTION Indian Accounting Standard (abbreviated asInd-AS) is theAccounting standardadopted by companies in India and iss

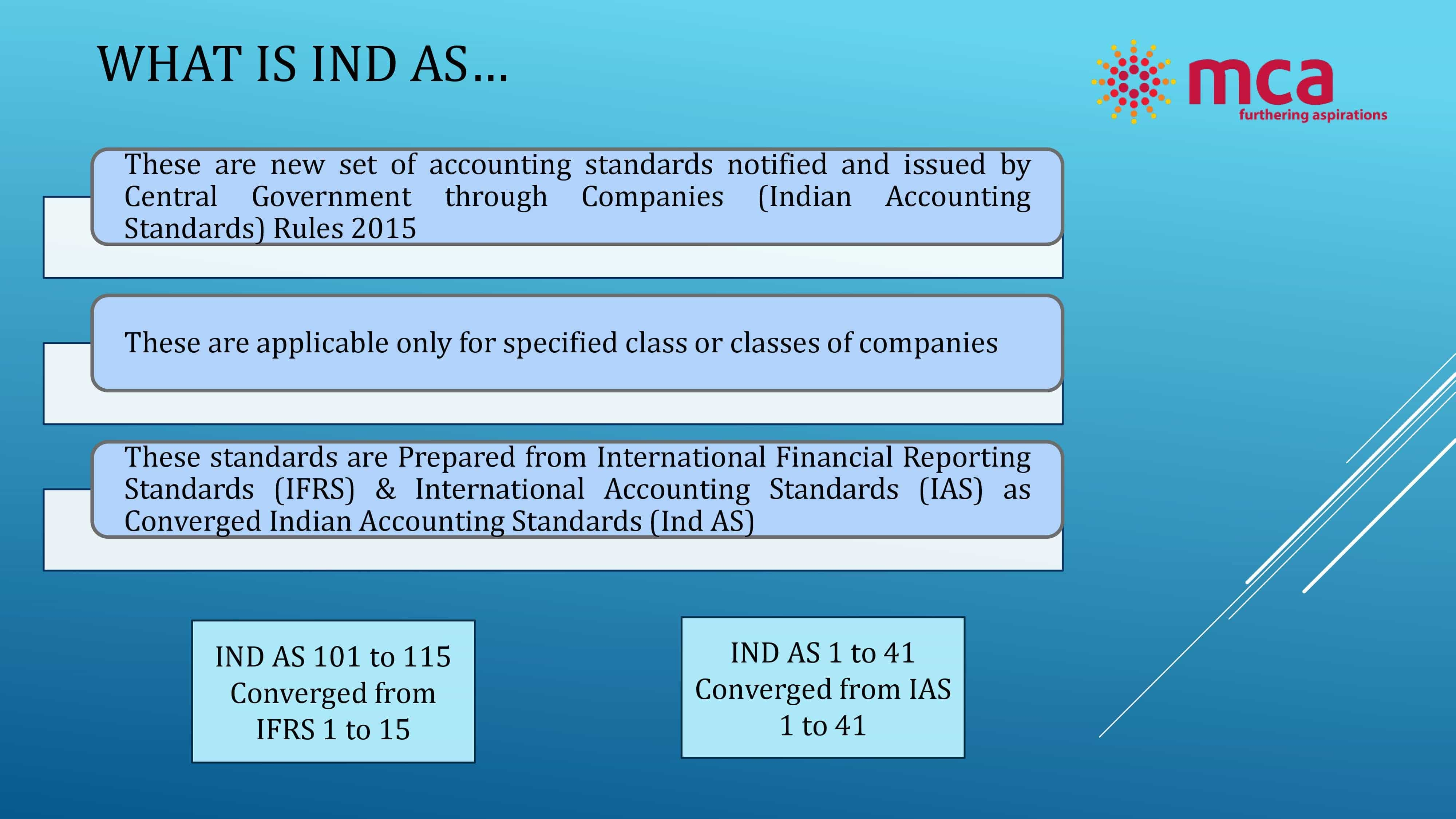

What is IND AS

INTRODUCTION

Indian Accounting Standard(abbreviated asInd-AS) is theAccounting standardadopted by companies in India and issued under the supervision and control of Accounting Standards Board (ASB), which was constituted as a body in the year 1977. ASB is a committee underInstitute of Chartered Accountants of India(ICAI) which consists of representatives from government department, academicians, other professional bodies viz. ICAI, representatives from ASSOCHAM, CII, FICCI, etc.

The Ind AS are named and numbered in the same way as the correspondingInternational Financial Reporting Standards(IFRS).National Advisory Committee on Accounting Standards(NACAS) recommend these standards to theMinistry of Corporate Affairs(MCA). MCA has to spell out the accounting standards applicable for companies in India. As on date MCA has notified 39 Ind AS. This shall be applied to the companies of financial year 2015-16 voluntarily and from 2016-17 on a mandatory basis.

BACKGROUND TO IND AS

Ind AS the new set of accounting standards was notified by the Ministry of Corporate Affairs (MCA) on February 19, 2015. As of date, there are 39 Ind AS notified by the MCA. The Ind AS are named and numbered in the same way as the corresponding IFRS. The application of Ind AS is based on the listing status and net worth of a company.

Applicability

The Council of the ICAI, at its meeting, held on March 20-22, 2014, has finalized the roadmap. As per this roadmap, the first set of accounting standards i.e. converged accounting standards (Ind AS) shall be applied to the following specified class of companies for preparing their first Indian Accounting Standards (Ind AS) consolidated financial statements for the accounting period beginning on or after April 1, 2016, with comparatives for the year ending 31stMarch 2016 or thereafter.

The specified class of companies includes,

(a) Whose equity and/or debt securities are listed or are in the process of listing company stock exchange in India or Outside India or

(b) Companies other than those covered in (a) above, having net worth ofRs. 500 crore or more

(c) Holding, Subsidiary, Joint Venture or associate companies covered under (a) or (b) above

Voluntary adoption

Companies can voluntarily adopt Ind AS for accounting periods beginning on or after 1 April 2015 with comparatives for period ending 31 March 2015 or thereafter. However, once they have chosen this path, they cannot switch back.

Mandatory Applicability

Phase I

Ind AS will be mandatorily applicable to the following companies for periods beginning on or after1 April 2016, with comparatives for the period ending31 March 2016or thereafter:

Companies whose equity and/or debt securities are listed or are in the process of listing on any stock exchange in India or outside India and having net worth of 500 crore INR or more.

Companies having net worth of 500 crore INR or more other than those covered above.

Holding, subsidiary, joint venture or associate companies of companies covered above.

Phase II

Ind AS will be mandatorily applicable to the following companies for periods beginning on or after1 April 2017, with comparatives for the period ending31 March 2017or thereafter:

Companies whose equity and/or debt securities are listed or are in the process of being listed on any stock exchange in India or outside India and having net worth of less than rupees 500 Crore.

Unlisted companies other than those covered in Phase I and Phase II whose net worth are more than 250 crore INR but less than 500 crore INR.

The Companies not covered under the Ind AS notification, would continue to apply with existing accounting standards under Companies (Accounting Standard) Rules, 2006.

Conceptual difference of Indian GAAP with IND AS

The volume and breadth of differences between Indian GAAP and Ind AS is enormous. Further, its impact will vary by industry and for each company. Ind AS will cover every area comprising reported revenues, expenses, assets, liabilities and equity. In our view, companies will have to devote substantial amount of their time especially in the following areas while preparing for Ind AS adoption.

The application of Ind AS is based on the listing status and net worth of a company. Ind AS will first apply to companies with a net worth equal to or exceeding 500 crore INR beginning 1 April 2016. Listed companies as well as others having a net worth equal to or exceeding 250 crore INR will follow 1 April 2017 onwards. From April 2015 companies impacted in the first phase will have to take a closer look at the details of the 39 new Ind AS currently notified. Ind AS will also apply to subsidiaries, joint ventures, associates as well as holding companies of the entities covered by the roadmap.

Functional Money Concept

Unlike in current accounting practices in India, there is a need to identify Functional Currency for every entity whose financial statements are being prepared underIND-AS/ IFRSwhenever it is applicable to them (based on the roadmap suggested by MCA for convergence of IND-AS in India).

How to identify functional currency

As per the standard, there are some primary indicators and secondary indicators which have to be looked at while assessing functional currency of any entity-

1) PRIMARY INDICATORS

Standard defines that there are broadly two conditions which need to be looked into.

The FIRSTone related to the currency in which the sales and cash that comes to the entity which essentially means that the currency in which good or services are Denominated and Settled and the currency of the country whose competitive forces and regulations determine the sale prices of goods/ services.

Secondly,the currency which mainly influences labour, material and other cost of providing such goods/ services which essentially means that if the significant portion of such costs which are being paid in a currency can be concluded as the entitys functional currency subject to consider other factors as well

2)SECONDARY INDICATORS

Standard defines some secondary indicators which need to be analyzed once an entity is not able to conclude evidently based on the primary indicators as mentioned above. These are currency in which financing activities are being undertaken e.g. fund raising in foreign denominated currencyANDthe currency in which working capital are usually maintained.

These financing and working capital indicators could be secondary to decide functional currency for an entity and one can argue that the entitys main business is not to lend the money hence financing activities should not be considered in isolation while analyzing functional currency of any entity.

Time value of Money

IND AS stresses on the time value of money as against historical cost methods in Indian GAAP. TVM concept has been used in many standards E.G. PPE, financial Instruments, financial liabilities, employee benefit expenses etc.

It is basically used to discount the Cash Flow to arrive at Present value, which is also useful to calculate Future Value of asset.

Other Comprehensive Income

Other comprehensive income (OCI) is defined as comprising items of income and expense (including reclassification adjustments) that are not recognized in profit or loss as required or permitted by other IFRSs. Total comprehensive income is defined as the change in equity during a period resulting from transactions and other events, other than those changes resulting from transactions with owners in their capacity as owners.

It is a myth, and simply incorrect, to state that only realized gains are included in profit or loss (P/L) and that only unrealized gain and losses are included in the OCI.

Example

Gains on the revaluation of land and buildings accounted for in accordance with IAS 16,Property Plant and Equipment(IAS 16 PPE), are recognised in OCI and accumulate in equity in Other Components of Equity (OCE). On the other hand, gains on the revaluation of land and buildings accounted for in accordance with IAS 40,Investment Properties, are recognised in P/L and are part of the Retained Earnings (RE). Both such gains are unrealised. The same point could be made with regard to the gains and losses on the financial asset of equity investments. If such financial assets are designated in accordance with IFRS 9,Financial Instruments(IFRS 9), at inception as Fair Value through Other Comprehensive Income (FVTOCI) then the gains and losses are recognised in OCI and accumulated in equity in OCE. Whereas if management decides not to make this election, then the investment will by default be designated and accounted for as Fair Value Through Profit or Loss (FVTP&L) and the gains and losses are recognised in P/L and become part of RE.

Basic EPS

The objective of this Standard is to prescribe principles for the determination and presentation of earnings per share, so as to improve performance comparisons between different entities in the same reporting period and between different reporting periods for the same entity. Even though earnings per share data have limitations because of the different accounting policies that may be used form determining earnings, a consistently determined denominator enhances financial reporting. The focus of this Standard is on the denominator of the earnings per share calculation.

This Indian Accounting Standard shall apply to companies that have issued ordinary shares1 to which Indian Accounting Standards notified under Part I of the Companies (Accounting Standards) Rules

An entity that discloses earnings per share shall calculate and disclose earnings per share in accordance with this Standard.

CONCLUSION

The policy makers in India have now realized the need to follow IND AS and it is expected that a large companies would be required to follow IND AS from 2013.There are a no. of challenges that India is likely to face while dealing with convergence with IND AS. The Indian Standard remains sensitive to local conditions, including the legal and economic environment.

The IND AS require fair valuation of assets and financial instrument for bringing transparency between book value and fair value the challenges arises that it will be a hectic work for Co. to compute fair value of assets.

This article has been prepared by Neha Goyal

Click Here to Buy CA Final Pendrive Classes at Discounted Rate

Tags: ind assummary pdf,ind aspdfind aslist,ind asppt,,ind asapplicability,whyind as isrequired, list of indian accounting standards,ind asmca

| Comparatives for period ending | 31 March 2015 or thereafter | 31 March 2016 or thereafter | 31 March 2017 or thereafter |

| 1 April 2015 | 1 April 2016 | 1 April 2017 | |

| Mandatorily applicable for the following companies | |||

| Applicable to companies | Voluntary adoption | Companies whose net worth is 500 crore INR or more | Companies whose equity and /or debt securities are listed or in the process of being listed on any stock exchange in India or outside India and having Net worth of less than 500 crore INR. |

| Holding, subsidiary, joint venture or associates companies of above companies. | Unlisted companies having net worth of 250 crore INR or more. | ||

| Holding, subsidiary, joint venture or associates companies of above companies | |||

About Author

CA Deepak Gupta

Co Founder

CA Deepak Gupta,is Co-founder of Studycafe. He is Microsoft Office Specialist and Corporate Trainer of AI Tools, Microsoft Excel.

He is Finance Influencer having more than 250K followers on Social Media. CA Deepak Gupta, is Having more than 14 plus years of experience, and he has Worked with best brands Like, Hero, Wipro, Ericsson before Starting Studycafe. He has Trained more than 20000 Persons in Microsoft Excel, PowerPoint, Power BI, Google Sheet, Google Forms and Other Tools.

CA Deepak Gupta,is Co-founder of Studycafe. He is Microsoft Office Specialist and Corporate Trainer of AI Tools, Microsoft Excel.

He is Finance Influencer having more than 250K followers on Social Media. CA Deepak Gupta, is Having more than 14 plus years of experience, and he has Worked with best brands Like, Hero, Wipro, Ericsson before Starting Studycafe. He has Trained more than 20000 Persons in Microsoft Excel, PowerPoint, Power BI, Google Sheet, Google Forms and Other Tools.

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 3423

3423My Recent Articles

- UltraTech Cement slapped with Rs. 808.78 Cr Income Tax Demand

- GST: High Court upheld constitutional validity of Section 16(2)(c), asks government to address ITC issues of genuine purchasers

- Old vs New Tax Regime for Tax Year 2026-27

- High court criticizes Income Tax Department for not releasing ITR Utilities despite 11 years of directions

- Fino Payments Bank CEO Rishi Gupta Gets Bail in GST Case, Bank Clarifies No Direct Link

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.