Whether interest paid u/s 201(1A) on late payment of TDS is an allowable expenses

Whether interest paid u/s 201(1A) on late payment of TDS is an allowable expenses Whether interest paid u/s 201(1A) of the Income Tax Act, 1

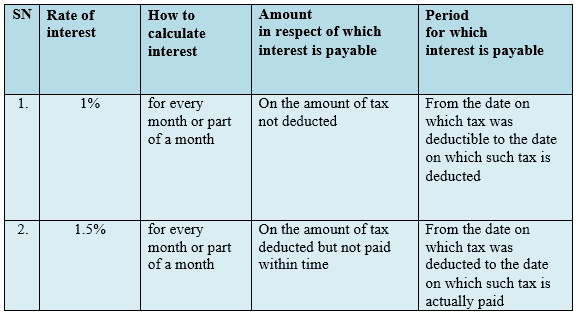

5. Word “interest” is defined section 2(28A) of the Act, as follows:

"interest" means interest payable in any manner in respect of any moneys borrowed or debt incurred (including a deposit, claim or other similar right or obligation) and includes any service fee or other charge in respect of the moneys borrowed or debt incurred or in respect of any credit facility which has not been utilised;

Profits or gains of business or profession

6. Section 28 of the Act provides incomes which shall be chargeable to income-tax under the head “Profits and gains of business or profession”.

7. Clause (i) of section 28 provides “the profits and gains of any business or profession which was carried on by the assessee at any time during the previous year” as one of such income.

8. Section 28 being the charging section under Chapter IV-D of the Act, such income needs to be first computed in terms of the provisions of section 2(45) r/w section 14 of the Act before the same is charged to income-tax u/s 4(1) of the Act.

9. Section 29 provides that “the income referred to in section 28 shall be computed in accordance with the provisions contained in section 30 to 43D”.

10. It means that before any business or professional income is included in “total income” in terms of section 14 r/w section 28 of the Act, it is to be computed in accordance with the provisions of section 30 to 43D, which provides the manner in which income chargeable under the head “Profits and gains of business or profession” is to be computed, as envisaged in section 2(45) of the Act.

11. In the context of “interest” following sections are relevant:

5. Word “interest” is defined section 2(28A) of the Act, as follows:

"interest" means interest payable in any manner in respect of any moneys borrowed or debt incurred (including a deposit, claim or other similar right or obligation) and includes any service fee or other charge in respect of the moneys borrowed or debt incurred or in respect of any credit facility which has not been utilised;

Profits or gains of business or profession

6. Section 28 of the Act provides incomes which shall be chargeable to income-tax under the head “Profits and gains of business or profession”.

7. Clause (i) of section 28 provides “the profits and gains of any business or profession which was carried on by the assessee at any time during the previous year” as one of such income.

8. Section 28 being the charging section under Chapter IV-D of the Act, such income needs to be first computed in terms of the provisions of section 2(45) r/w section 14 of the Act before the same is charged to income-tax u/s 4(1) of the Act.

9. Section 29 provides that “the income referred to in section 28 shall be computed in accordance with the provisions contained in section 30 to 43D”.

10. It means that before any business or professional income is included in “total income” in terms of section 14 r/w section 28 of the Act, it is to be computed in accordance with the provisions of section 30 to 43D, which provides the manner in which income chargeable under the head “Profits and gains of business or profession” is to be computed, as envisaged in section 2(45) of the Act.

11. In the context of “interest” following sections are relevant:

(i) Section 36 : Other deductions

(ii) Section 37 : General

(iii) Section 40 : Amounts not deductible

(iv) Section 40A : Expenses or payments not deductible in certain circumstances

(v) Section 43B : Certain deductions to be allowed on actual payment

12. Section 30 to 38 provides deductions in respect of specific expenses and allowances incurred for the purpose of business, the income of which is chargeable u/s 28 of the Act, e.g.(i) u/s 30 : for rent, rates, taxes, repairs and insurance for buildings;

(ii) u/s 31 : for repairs and insurance of machinery, plant and furniture;

(iii) u/s 32 : depreciation

(iv) u/s 36 : other deductions

(a) u/s 36(1)(i) : insurance premium of stocks and stores;

(b) u/s 36(1)(ib) : health insurance premium of employees;

(c) u/s 36(1)(iii) : interest on borrowed capital;

(d) u/s 36(1)(vii) : bad debts;

(e) u/s 36(1)(xiii) : banking cash transaction tax;

(f) u/s 36(1)(xv) : securities transaction tax;

(g) u/s 36(1)(xvi) : commodities transaction tax etc.

(v) u/s 37 : general

(vi) u/s 38 : Building etc., partly used for business, etc. or not exclusively so used.

13. Section 40, section 40A and section 43B are the sections of disallowances. These sections either deny or restrict the allowance of deductions allowable under section 30 to 38 or imposes condition for such allowance. 14. Section 40 provides disallowance in respect of certain expenses. It starts with non obstante clause and provides that “notwithstanding anything to the contrary in section 30 to 38, the following amounts shall not be deducted in computing the income chargeable under the head “profits an and gains of business or profession” 15. It means that if any expense is allowable u/s 30 to 38, it may be disallowed u/s 40 of the Act, as provided therein. 16. Section 40A provides disallowances in certain circumstances. Sub-section (1) provides that the provisions of this section shall have the effect notwithstanding anything to the contrary contained in any other provision of this Act relating to the computation of income under the head “Profits and gains of business or profession”. 17. It means that if any expense is otherwise allowable under the provisions of this Act, it may be disallowed u/s 40A o the Act, as provided therein. 18. Section 43B provides deductions of certain expenses only on actual payment. It starts with non obstante clause and provides that “notwithstanding anything contained in any other provision of this Act, a deduction otherwise allowable under this Act in respect of - 19. It means that if any expense is otherwise allowable under the provisions of this Act, it may be disallowed u/s 43B o the Act, as provided therein. 20. Section 36(iii) provides that following deduction shall be allowed in respect of computing the income referred to in section 28:

20. Section 36(iii) provides that following deduction shall be allowed in respect of computing the income referred to in section 28:

“the amount of the interest in respect of capital borrowed for the purposes of the business or profession.”

“Provided that any amount of the interest paid, in respect of capital borrowed for acquisition of an asset (whether capitalised in the books of account or not); for any period beginning from the date on which the capital was borrowed for acquisition of the asset till the date on which such asset was first put to use, shall not be allowed as deduction.”

21. We need to examine, whether simple interest paid u/s 201(1A) of the Act for non deduction of tax at source under the provisions of the Act or after deduction is not paid within the time allowed in or under the Act, is interest on capital borrowed for the purpose of business or profession? 22. The answer lies in the ratio of law decided by the Apex Court in the case of In the case of Bharat Commerce and Industries [1998] 230 ITR 733 (SC) as follows: Questions referred in C.A. No. 5509 of 1985 "Whether on the facts and in the circumstances of the case the claim for deduction of interest levied under Section 139 to the extent of Rs. 11,470/- and interest levied under Section 215 to the extent of Rs. 1,04,339/- was rightly rejected as not allowable under Section 37 of the Income-Tax Act, 1961 for the assessment year 1972-73?" Order The Apex Court rejected the contention of the assessee that the taxes which were payable were delayed and to that extent the assessee's financial resources increased. These increased resources became available for business purposes. Hence the interest which is paid to the Government under Section 139 and 215 represent, in effect, interest on capital that would have been borrowed by the assessee otherwise. Hence, these amounts should be allowed as deduction under Section 37 as expenses incurred wholly and exclusively for the purpose of its business. Questions referred in C.A. Nos. 3355-56 of 1993

"Whether on facts and circumstances of the case and in law the Tribunal was right in holding that the assessee was not entitled to the deduction of Rs. 2,94,082 in assessment year 1977-78 and Rs. 43,142/- assessment year 1978-79 being the interest payable on account of additional liability for income-tax and surtax on account of the disclosure of income made under the Voluntary Disclosure of Income and Wealth Act, 1976 u/s 37 or 36(1)(iii) of the Income-tax Act, 1961?."

Order

Apart from section 37, the assessee has also pressed into service Section 36(1)(iii) which permits deduction in respect of the amount of interest paid in respect of capital borrowed for the purposes of the assessee's business or profession. For the reasons set out earlier, the claim for deduction under section 36(1)(iii) is also misconceived just as the assessee's claim under section 37 is misconceived.

23. Following the above ratios of law in the case of Bharat Commerce and Industries (1998) 230 ITR 733 (SC) the Madras High Court in the case of Chennai Properties and Investment Ltd., 239 ITR 435 (Mad)} held as follow:

Facts of the case

The assessee had, in the course of assessment proceedings for the assessment year 1981-82, claimed deduction of Rs. 10,542 which amount had been paid by it to the Income-tax Department as interest under Section 201(1A) of the Income-tax Act, 1961. The claim so made was rejected by the Income-tax Officer and that rejection affirmed in appeal by the Commissioner of Income-tax. The Income-tax Appellate Tribunal, however, on a further appeal by the assessee, held that the interest so paid was incidental to the business of the assessee and allowed the amount as deduction under Section 37 of the Income-tax Act,

Issue

“Interest under Section 201(1A) paid by the assessee was an expenditure incidental to the business and allowed as a deduction from the profits and gains of the business for the assessment year 1981-82.”

Held

The amount not deducted and remitted has the character of tax and has to be remitted to the State and cannot be utilised by the assessee for its own business. The Supreme Court in the case of Bharat Commerce and Industries [1998] 230 ITR 733, rejected the argument advanced by the assessee that retention of money payable to the State as tax or income-tax would augment the capital of the assessee and the expenditure incurred, namely, interest paid for the period of such retention would assume character of business expenditure. The court held that an assessee could not possibly claim that it was borrowing from the State, the amounts payable by it as income-tax, and utilising the same as capital in its business, to contend that the interest paid for the period of delay in payment of tax amounted to business expenditure.

24. In view of above judgments, the amount of income tax due to be paid to the Government but not paid or the amount of tax deducted at source but not retained and not paid in time cannot be equated with and treated as capital borrowed from the Government in terms of section 36(1)(iii) of the Act. Hence interest paid on such amount cannot be allowed as deduction u/s 36(1)(iii) of the Act.

25. Therefore, in view of the decision of the Apex Court in the case of Bharat Commerce and Industries [1998] 230 ITR 733 (SC), such interest is not allowable as deduction u/s 36(1)(iii) of the Act. The judgment of the Apex Court to this extent is law of the land by virtue of Article 141 of the Constitution of India.

Questions referred in C.A. Nos. 3355-56 of 1993

"Whether on facts and circumstances of the case and in law the Tribunal was right in holding that the assessee was not entitled to the deduction of Rs. 2,94,082 in assessment year 1977-78 and Rs. 43,142/- assessment year 1978-79 being the interest payable on account of additional liability for income-tax and surtax on account of the disclosure of income made under the Voluntary Disclosure of Income and Wealth Act, 1976 u/s 37 or 36(1)(iii) of the Income-tax Act, 1961?."

Order

Apart from section 37, the assessee has also pressed into service Section 36(1)(iii) which permits deduction in respect of the amount of interest paid in respect of capital borrowed for the purposes of the assessee's business or profession. For the reasons set out earlier, the claim for deduction under section 36(1)(iii) is also misconceived just as the assessee's claim under section 37 is misconceived.

23. Following the above ratios of law in the case of Bharat Commerce and Industries (1998) 230 ITR 733 (SC) the Madras High Court in the case of Chennai Properties and Investment Ltd., 239 ITR 435 (Mad)} held as follow:

Facts of the case

The assessee had, in the course of assessment proceedings for the assessment year 1981-82, claimed deduction of Rs. 10,542 which amount had been paid by it to the Income-tax Department as interest under Section 201(1A) of the Income-tax Act, 1961. The claim so made was rejected by the Income-tax Officer and that rejection affirmed in appeal by the Commissioner of Income-tax. The Income-tax Appellate Tribunal, however, on a further appeal by the assessee, held that the interest so paid was incidental to the business of the assessee and allowed the amount as deduction under Section 37 of the Income-tax Act,

Issue

“Interest under Section 201(1A) paid by the assessee was an expenditure incidental to the business and allowed as a deduction from the profits and gains of the business for the assessment year 1981-82.”

Held

The amount not deducted and remitted has the character of tax and has to be remitted to the State and cannot be utilised by the assessee for its own business. The Supreme Court in the case of Bharat Commerce and Industries [1998] 230 ITR 733, rejected the argument advanced by the assessee that retention of money payable to the State as tax or income-tax would augment the capital of the assessee and the expenditure incurred, namely, interest paid for the period of such retention would assume character of business expenditure. The court held that an assessee could not possibly claim that it was borrowing from the State, the amounts payable by it as income-tax, and utilising the same as capital in its business, to contend that the interest paid for the period of delay in payment of tax amounted to business expenditure.

24. In view of above judgments, the amount of income tax due to be paid to the Government but not paid or the amount of tax deducted at source but not retained and not paid in time cannot be equated with and treated as capital borrowed from the Government in terms of section 36(1)(iii) of the Act. Hence interest paid on such amount cannot be allowed as deduction u/s 36(1)(iii) of the Act.

25. Therefore, in view of the decision of the Apex Court in the case of Bharat Commerce and Industries [1998] 230 ITR 733 (SC), such interest is not allowable as deduction u/s 36(1)(iii) of the Act. The judgment of the Apex Court to this extent is law of the land by virtue of Article 141 of the Constitution of India.

26. We need to examine, whether simple interest paid u/s 201(1A) of the Act for non deduction of tax at source under the provisions of the Act or after deduction is not paid within the time allowed in or under the Act, is allowable under section 37(1) of the Act being incurred for the purpose of business or profession?

27. Section 37(1) provides for deduction of any expenditure laid out or expended wholly and exclusively for the purpose of “the” business or profession.

28. Section 37(1) envisages following conditions for allowance of deduction:

(i) the amount being claimed should be an expenditure;

(ii) it should be laid of expended wholly and exclusively for the purpose of the business or profession.

29. Use of word “the” before the expression “business or profession” signifies the “business or profession”, income of which is being computed u/s 29 and which is chargeable to income-tax u/s 28 of the Act.

30. Section 37(1) r.w. its Explanation 1 makes certain exclusions. The relevant exclusions made by the section along with the Explanation 1 are the following:

26. We need to examine, whether simple interest paid u/s 201(1A) of the Act for non deduction of tax at source under the provisions of the Act or after deduction is not paid within the time allowed in or under the Act, is allowable under section 37(1) of the Act being incurred for the purpose of business or profession?

27. Section 37(1) provides for deduction of any expenditure laid out or expended wholly and exclusively for the purpose of “the” business or profession.

28. Section 37(1) envisages following conditions for allowance of deduction:

(i) the amount being claimed should be an expenditure;

(ii) it should be laid of expended wholly and exclusively for the purpose of the business or profession.

29. Use of word “the” before the expression “business or profession” signifies the “business or profession”, income of which is being computed u/s 29 and which is chargeable to income-tax u/s 28 of the Act.

30. Section 37(1) r.w. its Explanation 1 makes certain exclusions. The relevant exclusions made by the section along with the Explanation 1 are the following:

(i) expenditure in the nature of capital nature,

(ii) expenditure in the nature of personal expenses of the assessee,

(iii) expenditure incurred for any purpose which is an offence,

(iv) expenditure incurred for any purpose which is prohibited by law,

(v) expenditure, not being expenditure of the nature described in section 30 to 36

31. Interest on delayed payment of TDS squarely falls within the ambit of section 37(1) and the question of its deductibility or allowability depends on the fact whether such interest can be regarded as expenditure laid out or expended wholly and exclusively for the purpose of the business or profession or hit by the exclusions provided. 32. The exclusions (i) and (ii) above are not applicable to the question in hand. Such interest is neither expenditure in the nature of capital nature nor expenditure in the nature of personal expenses of the assessee. 33. Further, the exclusion (iii) and (iv) are applicable only if the purpose of the expenditure is an offence or is prohibited by law. 34. Such interest is not paid for the purpose which is an offence or prohibited by law. In fact such interest is paid for the purpose of the compliance with the provisions of the Income Tax Act, which is related to an activity occurring in the course of carrying on business or profession, as the case may be. 35. Such interest is paid due to delay in payment of TDS, which an assessee is obliged to deduct. He is required to make the payment of such TDS within the stipulated time, so that he may furnish statement of TDS, consequent to which credit of such TDS may be allowed to the deductee . The deductor is allowed delayed payment of TDS but subject to payment of interest. It is not the law that delayed payment is prohibited by law. The delayed payment is allowed subject to payment of simple interest u/s 201(1A). 36. Therefore, the exclusions (iii)and (iv) are also not applicable to such interest, as it is not incurred for any offence or prohibition of law. 37. The exclusions (v) is also not applicable to the question in hand. Such interest is not covered under section 36(1)(iii) of the Act, as it is not paid in respect of capital borrowed. 38. It may be concluded by saying that as per the provisions of section 29, the incomes referred to in section 28 shall be computed in accordance with the provisions of sections 30 to 43D. Section 37(1) provides that “any expenditure laid out or expended wholly and exclusively for the purpose of the business or profession shall be allowed in computing the income chargeable under the head “Profits and Gains of business or profession”. Any expenditure incurred in relation to any business activity shall be treated as laid out or expended for the purposes of the business or profession, as the case may be. Making payments of the nature to which the provisions of Chapter XVII-B of the Act applies, deducting tax in accordance with the provisions of the said chapter and payment of TDS are the activities which relates to the business or profession, as the case may be. As the interest takes its colour from the principal amount with regards to which it is paid, therefore, interest on late payment of TDS also relates to the activity of deduction of TDS and payment thereof, thus a business activity and business expenditure. 39. Such interest also does not fall in the trap of section 40(b)(ii). 40. Section 40 is the section of disallowance. It imposes variable conditions on allowability of deduction of expenses and allowances otherwise allowable under section 30 to 38 in computing “the” income chargeable under the head “Profits and gains of business or profession”.

41. Section 40(a)(ii) specifically disallows rate or tax paid as a deductible expenditure.

42. However, interest paid u/s 201(1A) for delayed payment of TDS does not falls within the ambit of this section.

43. Section 40(a)(ii) is reproduced hereunder for ready reference:

"any sum paid on account of any rate or tax levied on “the” profits or gains of any business or profession or assessed at a proportion of, or otherwise on the basis of, any such profits or gains"

44. For the better understanding of the provision, it is being dissected as follows:

40. Section 40 is the section of disallowance. It imposes variable conditions on allowability of deduction of expenses and allowances otherwise allowable under section 30 to 38 in computing “the” income chargeable under the head “Profits and gains of business or profession”.

41. Section 40(a)(ii) specifically disallows rate or tax paid as a deductible expenditure.

42. However, interest paid u/s 201(1A) for delayed payment of TDS does not falls within the ambit of this section.

43. Section 40(a)(ii) is reproduced hereunder for ready reference:

"any sum paid on account of any rate or tax levied on “the” profits or gains of any business or profession or assessed at a proportion of, or otherwise on the basis of, any such profits or gains"

44. For the better understanding of the provision, it is being dissected as follows:

• any sum paid

• on account of

• any

• rate

• or

• “tax”

• levied

• on

• the “profits or gains of any business or profession”

• or assessed at a proportion of, or otherwise on the basis of, any “such profits or gains”

Tax & Tax on the Profits or gains of any business or profession 45. Under the Act the definition of “tax” u/s 2(43) of the Act does not include penalty or interest and that the concepts of tax, penalty and interest are different concepts under the Act. 46. This interpretation in reply to question No. 5 finds favour from the decision of Apex Court in the case of Harshad Shantilal Mehta vs. Custodian 231 ITR 871, 890 (SC), as follows:“whether‘taxes’ under Section 11(2)(a) would include interest or penalty as well? We are concerned in the present case with penalty and interest under the Income Tax Act. Tax, penalty and interest are different concepts under the Income Tax Act. The definition of "tax" under Section 2(43) does not include penalty or interest. Similarly, under Section 156, it is provided that when any tax, interest, penalty, fine or any other sum is payable in consequence of any order passed under this Act, the Assessing Officer shall serve upon the assessee a notice of demand as prescribed. Provisions for imposition of penalty and interest are distinct from the provisions for imposition of tax.”

47. The expression "profits or gains of any business or profession" which is employed in section 40(a)(ii) can, in the context, have reference only to “the” profits or gains as referred to in section 28 and to be computed under 29 of the Act and cannot cover the net profits or gains arrived at or determined in a manner other than that provided by the said sections. 48. It is the business of the assessee who makes payments of income and claim the same as expense in his computation of total income. Such payment of expense is subjected to TDS under the provisions of the Act. Such TDS cannot be equated with the tax on profits or gains of business of the deductor which is computed u/s 29 of the Act and which is chargeable u/s 28 of the Act. 49. The expression the profits or gains of any business or profession” used in section 40(a)(ii) and the expression “allowable under section 30 to 38 in computing the income chargeable under the head “Profits and gains of business” used in the long lines of section 40 very clearly states that the “tax” to be disallowed u/s 40(a)(ii) is the “tax” on profits and gains of business, which is chargeable u/s 28 and which is to be computed u/s 29 with the aid of sections 30 to 43D. Therefore, the tax here can notbe equated with TDS. 50. The above proposition finds support from the decision of Apex Court in the case of Jaipuria Samla Amalgamated Collieries Ltd. vs. CIT 82 ITR 580 (SC)“it can be said that tax deduction at source is not the income-tax which is required to be paid on income chargeable to tax u/s 28, but is the tax to be deducted on payment being made to other party.”

51. In the case of Arthur Anderson & Co. vs. ACIT (2010) 190 Taxman 279 (Bombay) in its return of income, assessee disclosed certain interest income as income from other sources. In notes to computation of income, it was disclosed that said interest income represented difference between interest received u/s. 244A and interest paid u/s. 220. During the course of assessment, AO had raised a query regarding said income and after considering assessee’s reply, passed an assessment order. Later AO had issued a notice u/s. 148 on the ground that entire interest u/s. 244A was required to be offered for taxation. On writ, it was held that, since assessee has disclosed fully and truly all material facts, reopening of assessment could not be sustained. Further, referring to SC decision in the case of Harshad Shantilal Mehta vs. Custodian 231 ITR 871 (SC), it was held that interest paid u/s. 220(2) could not be considered as tax for the purpose of business disallowances in view of the following observations:“9. Apart from the fact that there has been no failure on the part of the assessee to make a full and true disclosure of all material facts, it will be necessary to advert to the decision of the Supreme Court in Harshad Shantilal Mehta v. Custodian (1998) 231 ITR 871. The Supreme Court, in the course of its judgment observed that under the Income- tax Act, 1961 the definition of tax under section 2(43) does not include penalty or interest and that the concepts of tax, penalty and interest are different concepts under the Act. Justice Sujata Manohar speaking for a Bench of three Learned Judges of the Supreme Court observed thus:

“We are concerned in the present case with penalty and interest under the Income-tax Act. Tax, penalty and interest are different concepts under the Income-tax Act. The definition of “tax” under section 2(43) does not include penalty or interest. Similarly, under section 156, it is provided that when any tax, interest, penalty, fine or any of other sum is payable in consequence of any order passed under this Act, the Assessing Officer shall serve upon the assessee a notice of demand as prescribed. The provisions for imposition of penalty and interest are distinct from the provisions for imposition of tax.”

10. The decision of the Supreme Court was delivered in an appeal which arose out of the Special Court (Trial of Offences relating to Transaction in Securities) Act, 1992. The interpretation which has been placed on the provisions of section 2(43) and the observations of the Supreme Court noted earlier, however, bind this Court as regards the ground on which the reopening of the assessment has been sought in this case."

52. In nut shell, the point of discussion is that what kind of tax is required to be disallowed;• tax which is required to be paid on own income of the assessee

or

• the tax which is required to be deducted by the assessee, which is nothing but the obligation of the assessee to deduct tax on payment being made to other assessee.

53. Interest on late payment of TDS is in compensatory nature. 54. Therefore, the tax deducted at source can never be considered “tax” u/s 40(a)(ii) and once if TDS cannot be considered, certainly interest on late payment of TDS cannot be considered for disallowance u/s 40(a)(ii) of the Act. 55. Therefore, in view of the above analysis of the law, interest on late payment of TDS is allowable as expenditure u/s 37(1) of the Act because –

55. Therefore, in view of the above analysis of the law, interest on late payment of TDS is allowable as expenditure u/s 37(1) of the Act because –

(i) it is an expenditure;

(ii) it is not in the nature of capital expenditure;

(iii) it is not in the nature of personal expenditure;

(iv) it is not an expense in relation to borrowed capital, therefore, outside the ambit of section 36(1)(iii). Hence, eligible u/s 37(1);

(v) it is not an expense in relation to rate or tax on the profits and gains of business or profession chargeable u/s 28. Therefore, it is not related to personal income tax of the assessee (deductor), which is otherwise not allowable u/s 40(a)(ii);

(vi) it is not incurred for any offence or any legal prohibition. Making delayed payment of TDS is not prohibited, rather it is allowed coupled with payment of interest for the delay;

(vii) it is not penalty, as under the Act, tax, interest, penalty, fee, fine are used and treated differently. One example is section 156, wherein tax, interest, penalty, fine or any other sum are used mutually exclusively.

{DCIT vs. M/s. Narayani Ispat Pvt. Ltd., ITAT Kalkata}

(viii) it is not penal in nature;

{Lachmandas Mathuradas vs. CIT 254 ITR 799 (SC)} {DCIT vs. M/s. Narayani Ispat Pvt. Ltd., ITAT Kalkata}

(ix) it is, rather, compensatory in nature;

{Lachmandas Mathuradas vs. CIT 254 ITR 799 (SC)} {Mahalakshmi Sugar Mills Co. vs. CIT (1980) 123 ITR 429 (SC)} {Prakash Cotton Mills (P) Ltd. vs. CIT (1993) 201ITR 684 (SC)} {Malwa Vanaspati & Chemical Co. vs. CIT (1997) 225 ITR 383 (SC)} {CIT vs. Ahmedabad Cotton Manufacturing Co. Ltd. (1994) 205 ITR 163 (SC)} {DCIT vs. M/s. Narayani Ispat Pvt. Ltd., ITAT Kalkata}

(x) it is incurred for the purpose of the business or profession, as the case may be, because it relates to business or professional activities:

(a) incurring of expenses like salary, wages, interest, commission, brokerage, fee for professional services, fee for technical services, royalty, rent, carrying out any work in pursuance of a contract etc. are for the purpose of business or profession;

(b) deduction of tax at source there from under chapter XVII-B is inextricably an activity for the purpose of business of profession;

(c) payment of TDS is again inextricably an activity for the purpose of business of profession;

(d) default in deduction of tax is inextricably business or professional activity, therefore, interest payable for such default is for the purpose of business of profession;

(e) default in payment TDS or delay in payment of TDS after deduction is also inextricably business or professional activity, therefore, interest payable for such default is for the purpose of business of profession;

(xi) it is not an expense of the assessee (deductor). Rather, it is an obligation, which he is required to discharge;

(xii) it is incurred in relation to tax of the other person (deductee), which has direct nexus with the expense incurred and claimed by the assessee (deductor), e.g. salary, wages, interest, commission, brokerage, fee for professional services, fee for technical services, royalty, rent, carrying out any work in pursuance of a contract etc. Therefore, it will partake its colour and character from such expense;

(xiii) it is akin to interest on sales tax, central sales tax, value added tax, service tax, excise duty, commercial cess etc.;

(xiv) it is not specifically disallowable under any provision of the Act.

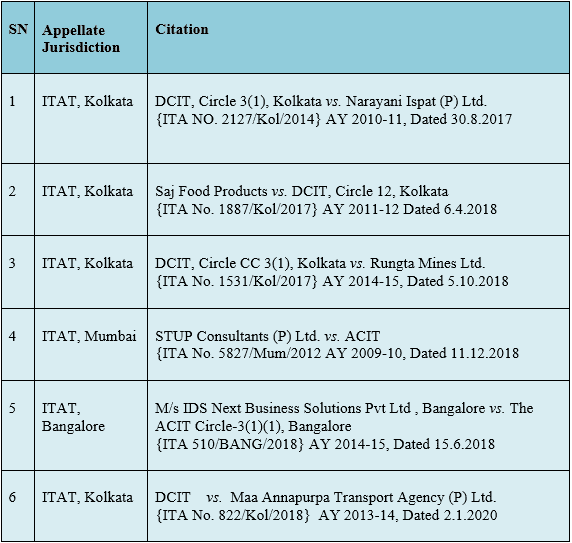

56. In support of the above propositions reliance may be placed on the following judicial pronouncements, wherein interest paid u/s 201(1A) on delayed payment of TDS has been allowed as business expenditure u/s 37(1) of the Act: 57. The above judgments are being discussed hereunder one by one.

57. The above judgments are being discussed hereunder one by one.

Held

The above principles can be applied to the interest expenses levied on account of delayed payment of TDS as it relates to the expenses claimed by the assessee which are subject to the TDS provisions. The assessee claims the specified expenses of certain amount in its profit & loss account and thereafter the assessee from the payment to the party deducts certain percentage as specified under the Act as TDS and pays to the Government Exchequer. The amount of TDS represents the amount of income tax of the party on whose behalf the payment was deducted & paid to the Government Exchequer. Thus the TDS amount does not represent the tax of the assessee but it is the tax of the party which has been paid by the assessee. Thus any delay in the payment of TDS by the assessee cannot be linked to the income tax of the assessee and consequently the principles laid down by the Hon’ble Apex Court in the case of Bharat Commerce Industries Ltd. Vs. CIT (1998) reported in 230 ITR 733 cannot be applied to the case on hand.

Thus, in our considered view, the principle laid down by the Hon'ble Supreme Court in the case of Bharat Commerce Industries Ltd. (supra) is not applicable in the instant facts of the case. Thus, we hold that the Assessing Officer in the instant case has wrongly applied the principle laid down by the Hon'ble Supreme Court in the case of Bharat Commerce Industries Ltd.(supra). We also find that the Hon'ble Supreme Court in the case of Lachmandas Mathura (Supra) has allowed the deduction on account of interest on late deposit of sales tax u/s 37(1) of the Act. In view of the above, we conclude that the interest expenses claimed by the assessee on account of delayed deposit of service tax as well as TDS liability are allowable expenses u/s 37(1) of the Act. In this view of the matter, we find no reason to interfere in the order of Ld. CIT(A) and we uphold the same. Hence, this ground of Revenue is dismissed.

Held

The above principles can be applied to the interest expenses levied on account of delayed payment of TDS as it relates to the expenses claimed by the assessee which are subject to the TDS provisions. The assessee claims the specified expenses of certain amount in its profit & loss account and thereafter the assessee from the payment to the party deducts certain percentage as specified under the Act as TDS and pays to the Government Exchequer. The amount of TDS represents the amount of income tax of the party on whose behalf the payment was deducted & paid to the Government Exchequer. Thus the TDS amount does not represent the tax of the assessee but it is the tax of the party which has been paid by the assessee. Thus any delay in the payment of TDS by the assessee cannot be linked to the income tax of the assessee and consequently the principles laid down by the Hon’ble Apex Court in the case of Bharat Commerce Industries Ltd. Vs. CIT (1998) reported in 230 ITR 733 cannot be applied to the case on hand.

Thus, in our considered view, the principle laid down by the Hon'ble Supreme Court in the case of Bharat Commerce Industries Ltd. (supra) is not applicable in the instant facts of the case. Thus, we hold that the Assessing Officer in the instant case has wrongly applied the principle laid down by the Hon'ble Supreme Court in the case of Bharat Commerce Industries Ltd.(supra). We also find that the Hon'ble Supreme Court in the case of Lachmandas Mathura (Supra) has allowed the deduction on account of interest on late deposit of sales tax u/s 37(1) of the Act. In view of the above, we conclude that the interest expenses claimed by the assessee on account of delayed deposit of service tax as well as TDS liability are allowable expenses u/s 37(1) of the Act. In this view of the matter, we find no reason to interfere in the order of Ld. CIT(A) and we uphold the same. Hence, this ground of Revenue is dismissed.

The above principles can be applied to the interest expenses levied on account of delayed payment of TDS as it relates to the expenses claimed by the assessee which are subject to the TDS provisions. The assessee claims the specified expenses of certain amount in its profit & loss account and thereafter the assessee from the payment to the party deducts certain percentage as specified under the Act as TDS and pays to the Government Exchequer. The amount of TDS represents the amount of income tax of the party on whose behalf the payment was deducted & paid to the Government Exchequer. Thus the TDS amount does not represent the tax of the assessee but it is the tax of the party which has been paid by the assessee. Thus any delay in the payment of TDS by the assessee cannot be linked to the income tax of the assessee and consequently the principles laid down by the Hon'ble Apex Court in the case of Bharat Commerce Industries Ltd. vs. CIT (1998) reported in 230 ITR 733 cannot be applied to the case on hand.

Thus, in our considered view, the principle laid down by the Hon'ble Supreme Court in the case of Bharat Commerce Industries Ltd. (supra) is not applicable in the instant facts of the case. Thus, we hold that the Assessing Officer in the instant case has wrongly applied the principle laid down by the Hon'ble Supreme Court in the case of Bharat Commerce Industries Ltd.(supra). We also find that the Hon'ble Supreme Court in the case of Lachmandas Mathura (Supra) has allowed the deduction on account of interest on late deposit of sales tax u/s 37(1) of the Act. In view of the above, we conclude that the interest expenses claimed by the assessee on account of delayed deposit of service tax as well as TDS liability are allowable expenses u/s 37(1) of the Act. In this view of the matter, we find no reason to interfere in the order of Ld. CIT(A) and we uphold the same. Hence, this ground of Revenue is dismissed.

13. In view of above, we are of the view that the CIT-A was not correct in confirming the impugned disallowance of Rs.1230/- made by the AO on account of interest on late deposit of TDS. The order of the CIT-A on this issue is set aside and the AO is directed to allow the same. Ground no. 2 raised by the assessee is allowed.

The above principles can be applied to the interest expenses levied on account of delayed payment of TDS as it relates to the expenses claimed by the assessee which are subject to the TDS provisions. The assessee claims the specified expenses of certain amount in its profit & loss account and thereafter the assessee from the payment to the party deducts certain percentage as specified under the Act as TDS and pays to the Government Exchequer. The amount of TDS represents the amount of income tax of the party on whose behalf the payment was deducted & paid to the Government Exchequer. Thus the TDS amount does not represent the tax of the assessee but it is the tax of the party which has been paid by the assessee. Thus any delay in the payment of TDS by the assessee cannot be linked to the income tax of the assessee and consequently the principles laid down by the Hon'ble Apex Court in the case of Bharat Commerce Industries Ltd. vs. CIT (1998) reported in 230 ITR 733 cannot be applied to the case on hand.

Thus, in our considered view, the principle laid down by the Hon'ble Supreme Court in the case of Bharat Commerce Industries Ltd. (supra) is not applicable in the instant facts of the case. Thus, we hold that the Assessing Officer in the instant case has wrongly applied the principle laid down by the Hon'ble Supreme Court in the case of Bharat Commerce Industries Ltd.(supra). We also find that the Hon'ble Supreme Court in the case of Lachmandas Mathura (Supra) has allowed the deduction on account of interest on late deposit of sales tax u/s 37(1) of the Act. In view of the above, we conclude that the interest expenses claimed by the assessee on account of delayed deposit of service tax as well as TDS liability are allowable expenses u/s 37(1) of the Act. In this view of the matter, we find no reason to interfere in the order of Ld. CIT(A) and we uphold the same. Hence, this ground of Revenue is dismissed.

13. In view of above, we are of the view that the CIT-A was not correct in confirming the impugned disallowance of Rs.1230/- made by the AO on account of interest on late deposit of TDS. The order of the CIT-A on this issue is set aside and the AO is directed to allow the same. Ground no. 2 raised by the assessee is allowed.

Ld.AR submits that the issue in hand is covered in favour of assesse on identical facts and issue by the order dt. 06-04-2018 of this Coordinate Bench, ITAT, Bench-D in assessee’s own case, ITA No. 1887/Kol/2016 for the A.Y 2011-12, copy of the same is on record and referred to paras 12 & 13 of the said order.

9. After hearing both the parties and on perusal of record including the order dt. 06-04- 2018 as relied on by the ld. AR of assesse. We find that the facts and circumstances of the case as relied on by the ld.AR are similar and identical with the facts and circumstances of the case in hand. We also find that the Co-ordinate Bench, ITAT, ‘D‘ Bench, Kolkata in the case of supra has discussed the issue thoroughly analyzing with facts of the case laws of the Hon’ble Supreme Court in the case of Bharat Commerce Industries

Ltd reported in (1998) 230 ITR 733(SC) & Lachmandas Mathura reported in 254 ITR 799(SC), wherein it was held interest paid on late deposit of sales tax is an allowable deduction u/s. 37(1) of the Act. Relevant portion of tribunal order is reproduced herein below:-

Ld.AR submits that the issue in hand is covered in favour of assesse on identical facts and issue by the order dt. 06-04-2018 of this Coordinate Bench, ITAT, Bench-D in assessee’s own case, ITA No. 1887/Kol/2016 for the A.Y 2011-12, copy of the same is on record and referred to paras 12 & 13 of the said order.

9. After hearing both the parties and on perusal of record including the order dt. 06-04- 2018 as relied on by the ld. AR of assesse. We find that the facts and circumstances of the case as relied on by the ld.AR are similar and identical with the facts and circumstances of the case in hand. We also find that the Co-ordinate Bench, ITAT, ‘D‘ Bench, Kolkata in the case of supra has discussed the issue thoroughly analyzing with facts of the case laws of the Hon’ble Supreme Court in the case of Bharat Commerce Industries

Ltd reported in (1998) 230 ITR 733(SC) & Lachmandas Mathura reported in 254 ITR 799(SC), wherein it was held interest paid on late deposit of sales tax is an allowable deduction u/s. 37(1) of the Act. Relevant portion of tribunal order is reproduced herein below:-

“12. Heard both the parties and perused the record including the order dt. 30-08- 2017 as relied on by the assessee before us. We find that the issue in hand is covered in favour of assessee by the said order dt. 30-08-2017 of this Tribunal in the case of (supra), which held that interest paid on delayed deposit of TDS is an allowable deduction by placing reliance on the decisions of Hon’ble Supreme Court in the case of Bhara Commerce Industries Ltd Vs. CIT reported in (1998) 230 ITR 733 (SC). The Co-ordinate Bench also referred to the decision of Hon’ble Supreme Court in the case of Lachmandas Mathura vs. CIT reported in 254 ITR 799 (SC), which held interest paid on late deposit of sales tax is an allowable deduction u/s 37(1) of the Act. Relevant portion of order dt.30- 08- 2017 is reproduced herein below for better understanding:-

The issue of delay in the payment of service tax is directly covered by the judgment of Hon’ble Apex Court in the case of Lachmandas Mathura vs. CIT reported (1998) reported in 230 ITR 733 cannot be applied to the case on hand. Thus, in our considered view, the principle laid down by the Hon'ble Supreme Court in the case of Bharat Commerce Industries Ltd. (supra) is not applicable in the instant facts of the case. Thus, we hold that the Assessing Officer in the instant case has wrongly applied the principle laid down by the Hon'ble Supreme Court in the case of Bharat Commerce Industries Ltd.(supra). We also find that the Hon'ble Supreme Court in the case of Lachmandas Mathura (Supra) has allowed the deduction on account of interest on late deposit of sales tax u/s 37(1) of the Act. In view of the above, we conclude that the interest expenses claimed by the assessee on account of delayed deposit of service tax as well as TDS liability are allowable expenses u/s 37(1) of the Act. In this view of the matter, we find no reason to interfere in the order of Ld. CIT(A) and we uphold the same. Hence, this ground of Revenue is dismissed.

13. In view of above, we are of the view that the CIT-A was not correct in confirming the impugned disallowance of Rs.1230/- made by the AO on account of interest on late deposit of TDS. The order of the CIT-A on this issue is set aside and the AO is directed to allow the same. Ground no. 2 raised by the assessee is allowed. “

10. In view of above, we find no infirmity in the impugned order of the CIT-A and it is justified. Thus, ground no. 2 raised by the revenue is dismissed. For Futher Details - Download PDF Tags: Income Tax, TDSAbout Author

Reetu

Content Manager

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts