10 Important changes in new Income Tax Forms (ITR) for FY 2022-23

10 Important changes in new Income Tax Forms (ITR) for FY 2022-23 This article discusses the Relevant changes in new Income Tax Forms (ITR) for FY 20…

10 Important changes in new Income Tax Forms (ITR) for FY 2022-23

This article discusses the Relevant changes in new Income Tax Forms (ITR) for FY 2022-23. Please note that the list is inclusive and not exclusive.

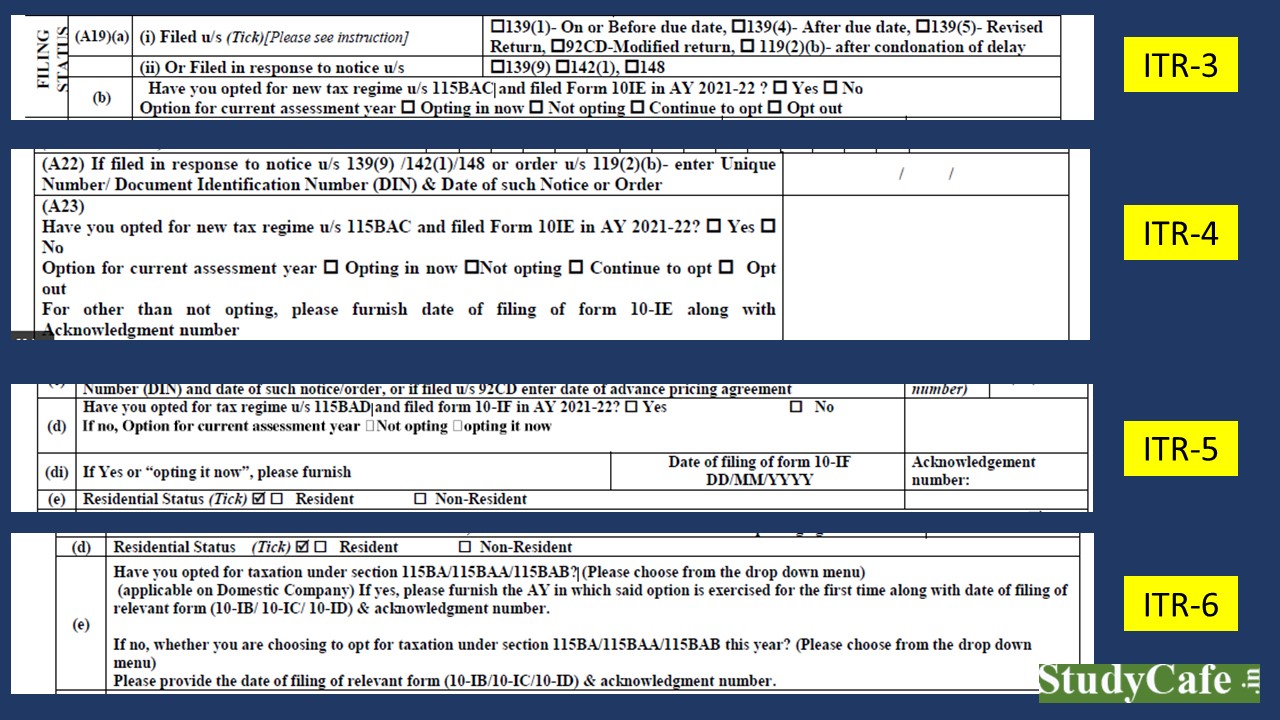

1. Businesses to disclose in which tax regime they are paying tax, opted before, opted now or not opting

[ITR 3, 4, 5 & 6]

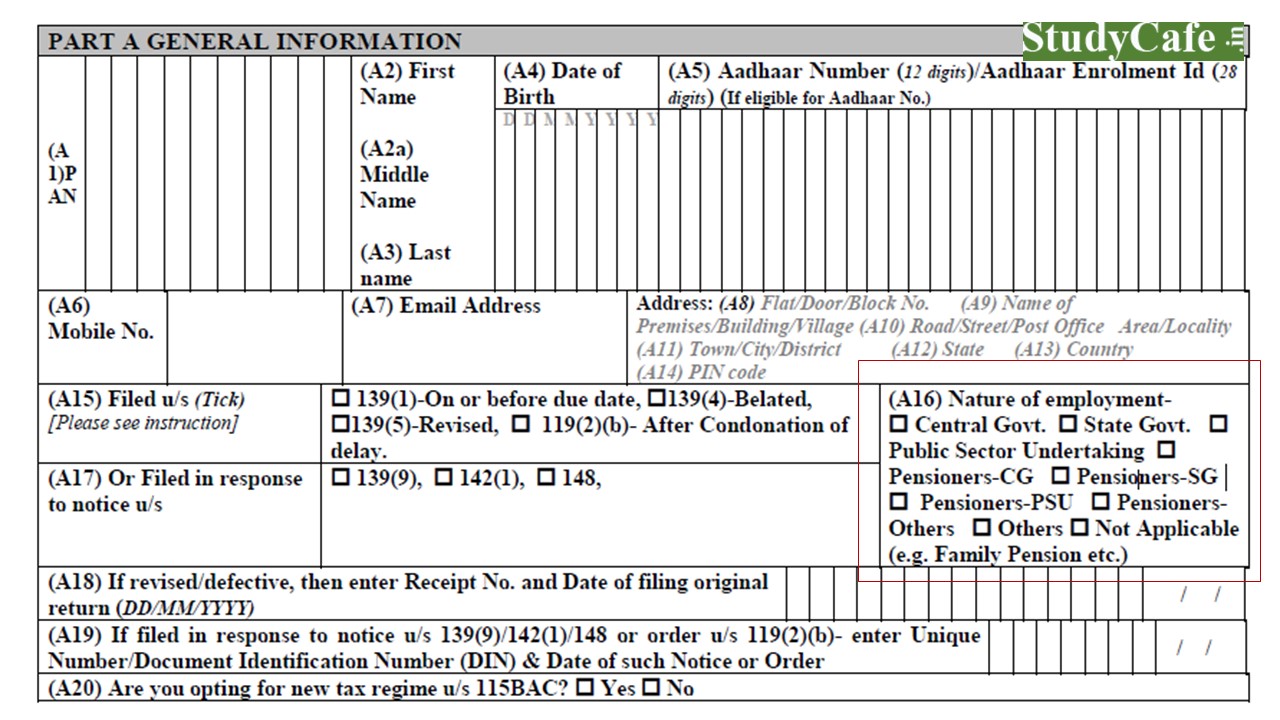

2. Pensioners need to disclose their income is from Central Government, State Government, Public Sector Units (PSU), or others

[ITR 1, 2, 3 & 4]

2. Pensioners need to disclose their income is from Central Government, State Government, Public Sector Units (PSU), or others

[ITR 1, 2, 3 & 4]

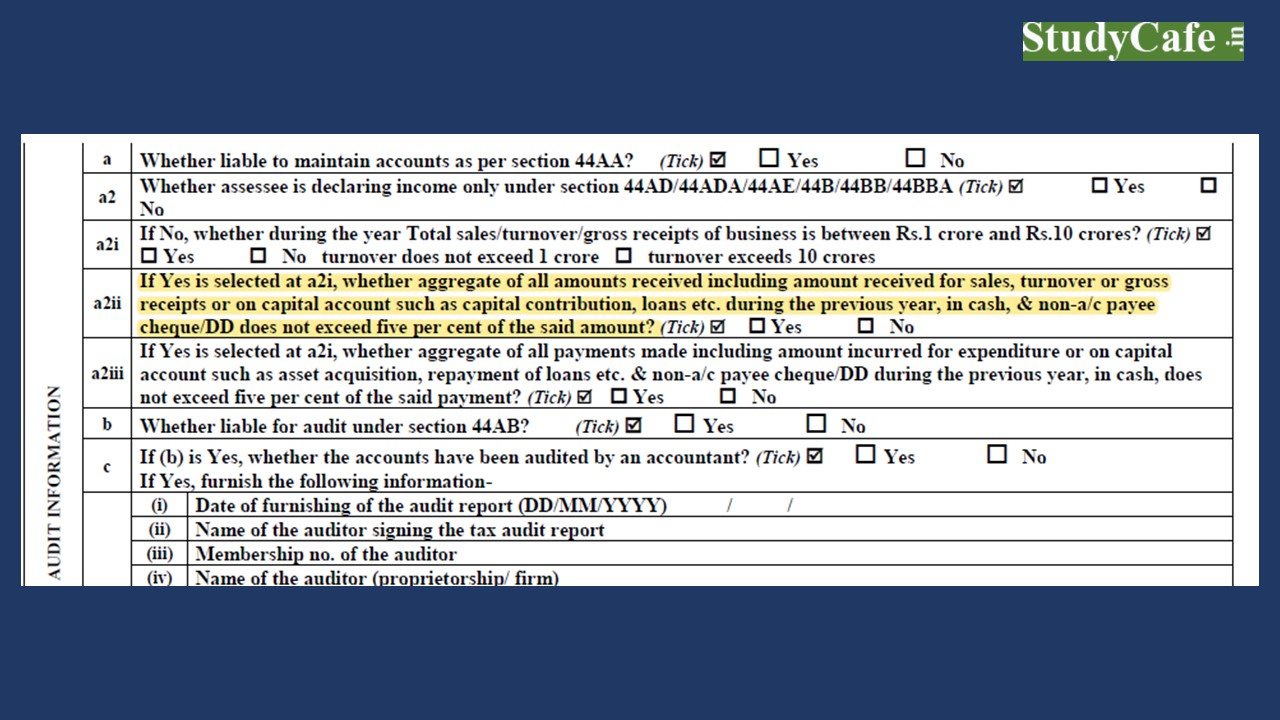

3. Additional Information is required for Businesses not opting for Presumptive Taxation

[ITR 3, 5, & 6]

Taxpayer not opting for Presumptive Taxation has to disclose the receipt and payment in cash. Now they have to disclose Payment received from a Non-account payee cheque or Demand Draft.

This amendment is related to Finance Act 2021. Watch this video for more clarification: REDUCTION IN TAX AUDIT LIMIT TO 1 CR FROM 10 CR?

3. Additional Information is required for Businesses not opting for Presumptive Taxation

[ITR 3, 5, & 6]

Taxpayer not opting for Presumptive Taxation has to disclose the receipt and payment in cash. Now they have to disclose Payment received from a Non-account payee cheque or Demand Draft.

This amendment is related to Finance Act 2021. Watch this video for more clarification: REDUCTION IN TAX AUDIT LIMIT TO 1 CR FROM 10 CR?

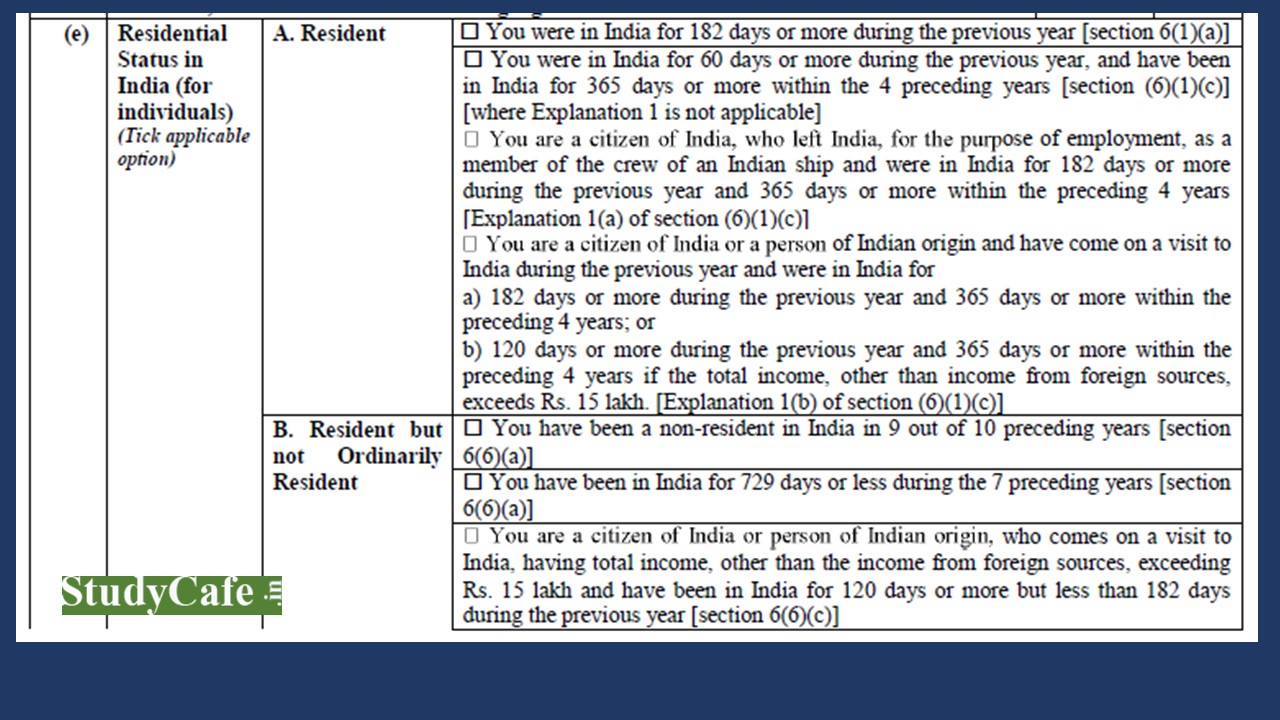

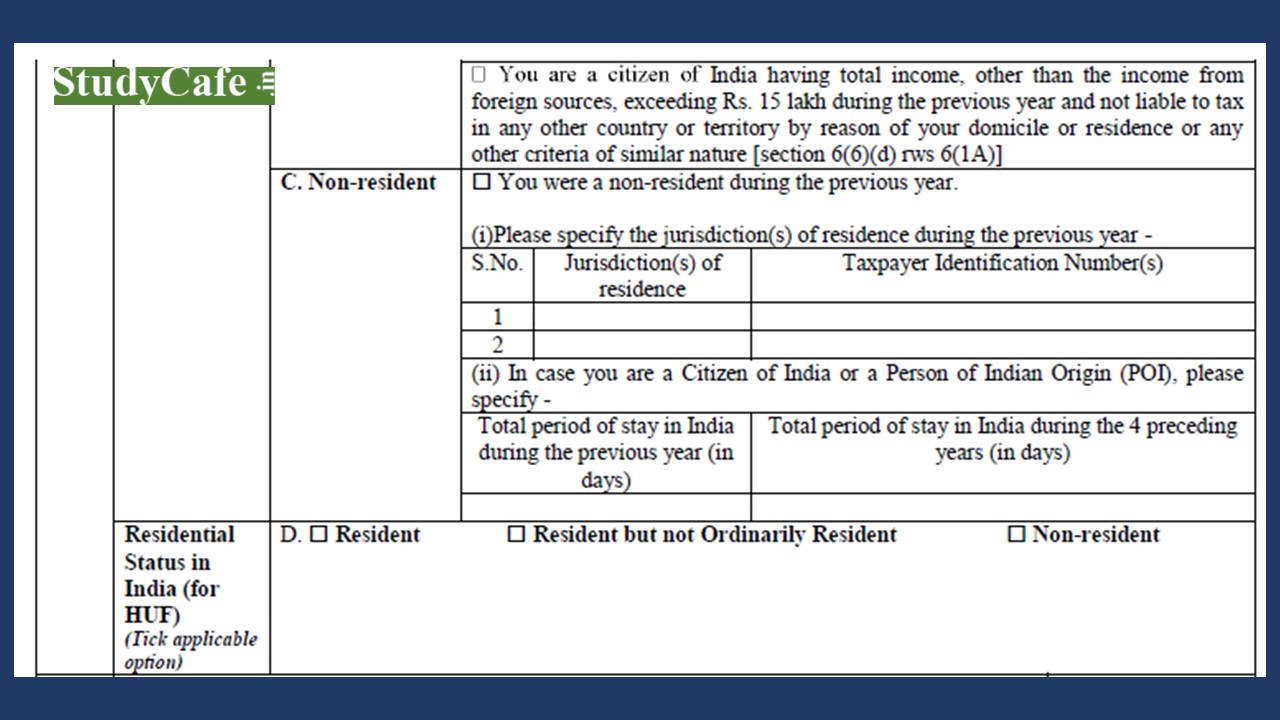

4. Resident Status in India: suitable description of different clauses

[ITR 2 & 3]

Changes have been made in ITR clause related to the Residential Status of Individual so that the status can be correctly determined.

4. Resident Status in India: suitable description of different clauses

[ITR 2 & 3]

Changes have been made in ITR clause related to the Residential Status of Individual so that the status can be correctly determined.

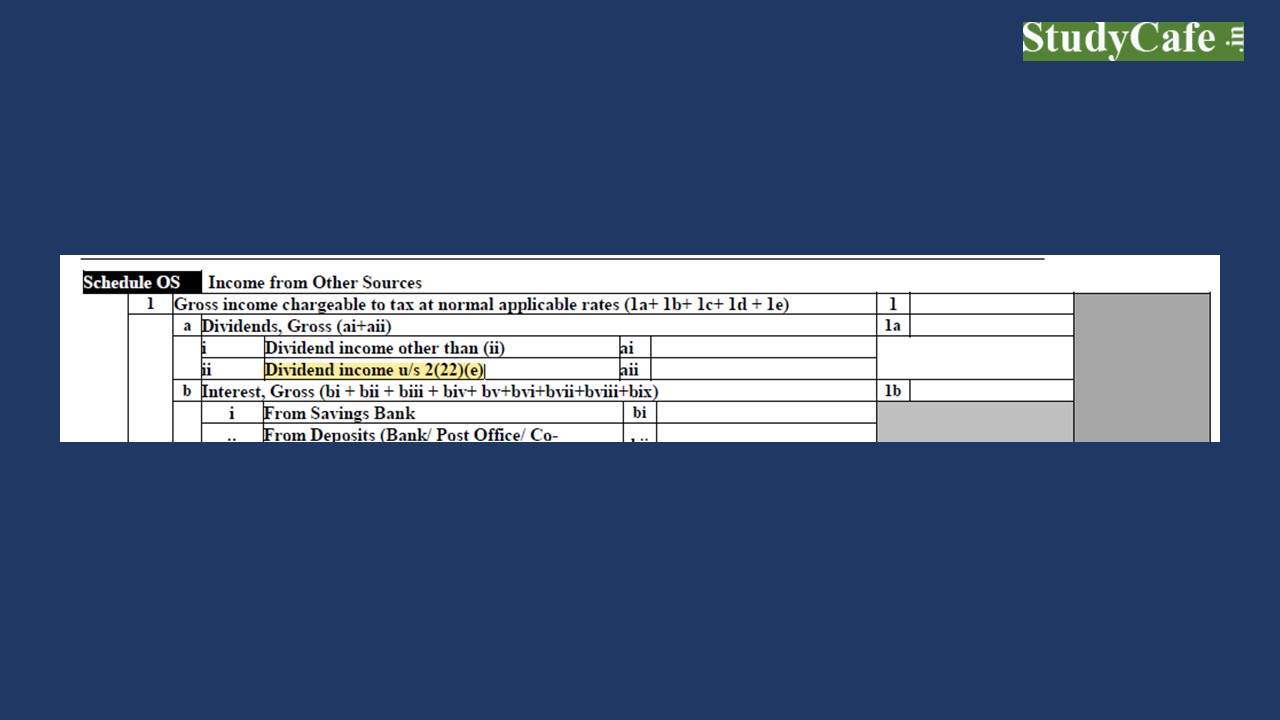

5. Dividend Income taxable as per section 2(22)(e) to be reported separately

[ITR 2, 3, 5 & 6]

Deemed Dividend Income as per Section 2(22)(e) is now required to be reported separately. Upto Last year there was no such specific disclosure. Deemed Dividend Income is Taxable in head other sources.

5. Dividend Income taxable as per section 2(22)(e) to be reported separately

[ITR 2, 3, 5 & 6]

Deemed Dividend Income as per Section 2(22)(e) is now required to be reported separately. Upto Last year there was no such specific disclosure. Deemed Dividend Income is Taxable in head other sources.

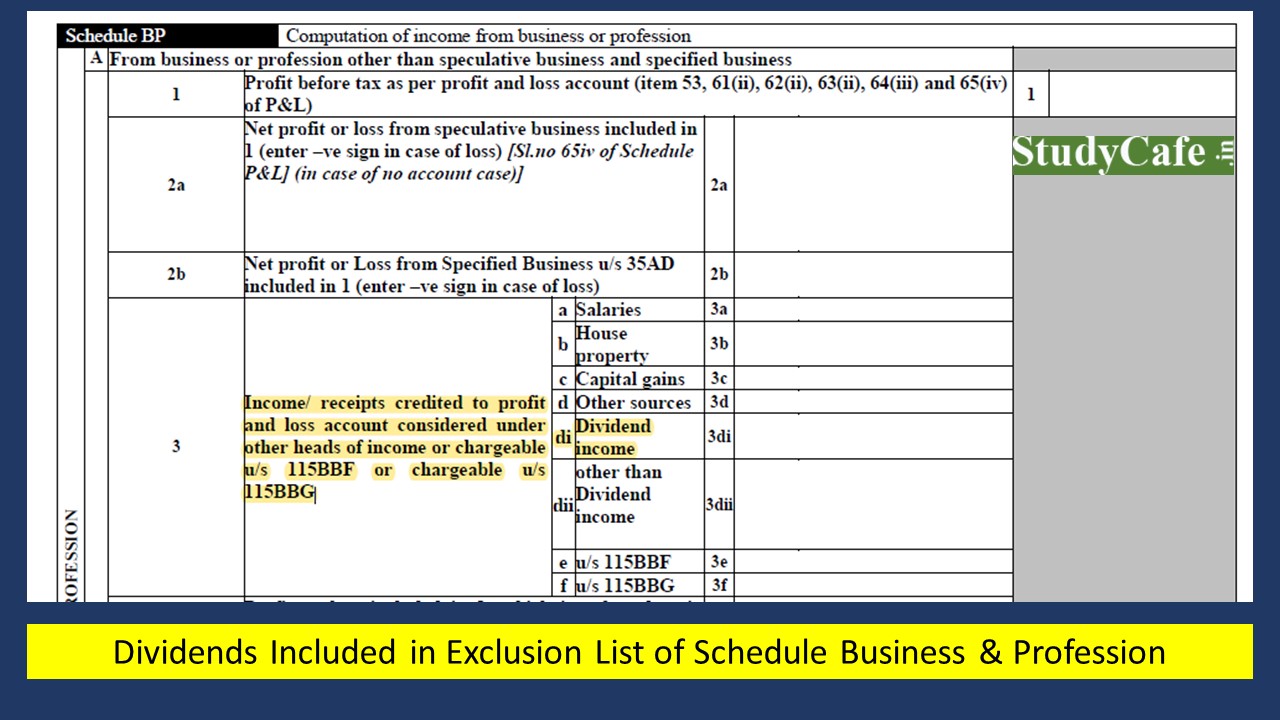

6) Dividend Income to be disclosed in Income from Other Source and not in Schedule BP.

[ITR 3, 5 & 6]

Dividends Included in Exclusion List of Schedule Business & Profession.

6) Dividend Income to be disclosed in Income from Other Source and not in Schedule BP.

[ITR 3, 5 & 6]

Dividends Included in Exclusion List of Schedule Business & Profession.

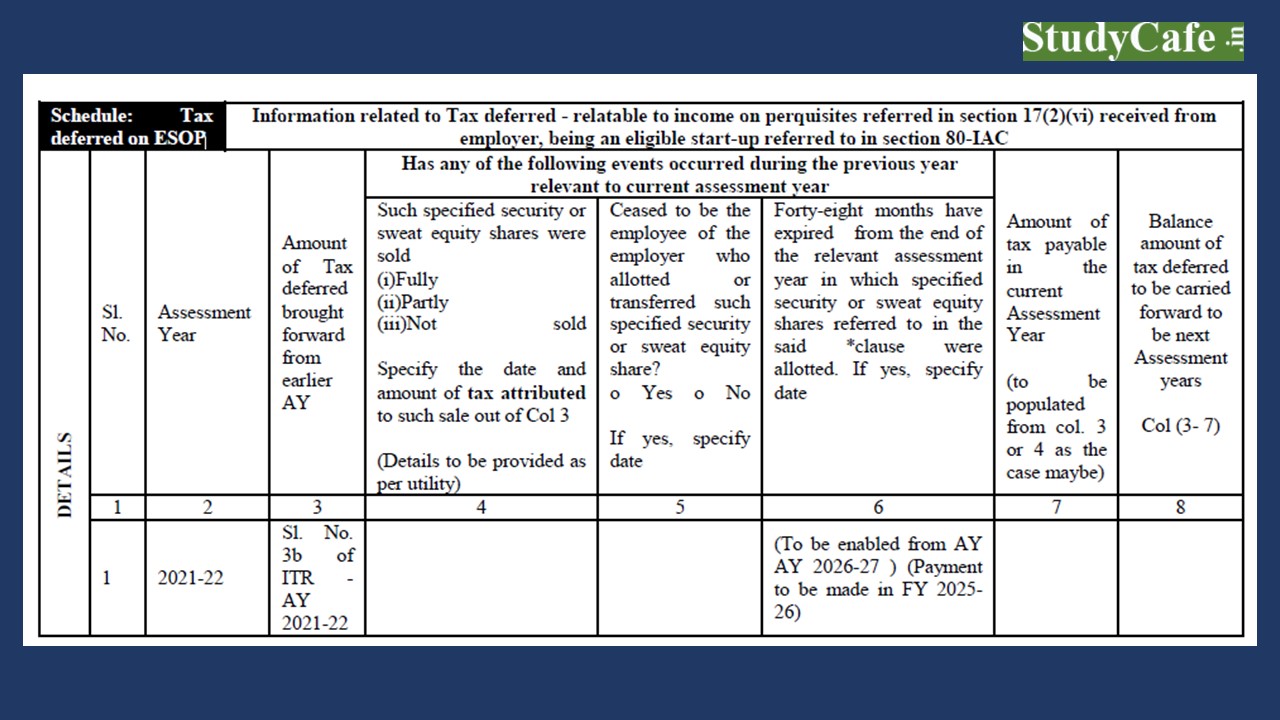

7) Deffered Tax on ESOP Schedule updated

[ITR 2 & 3]

7) Deffered Tax on ESOP Schedule updated

[ITR 2 & 3]

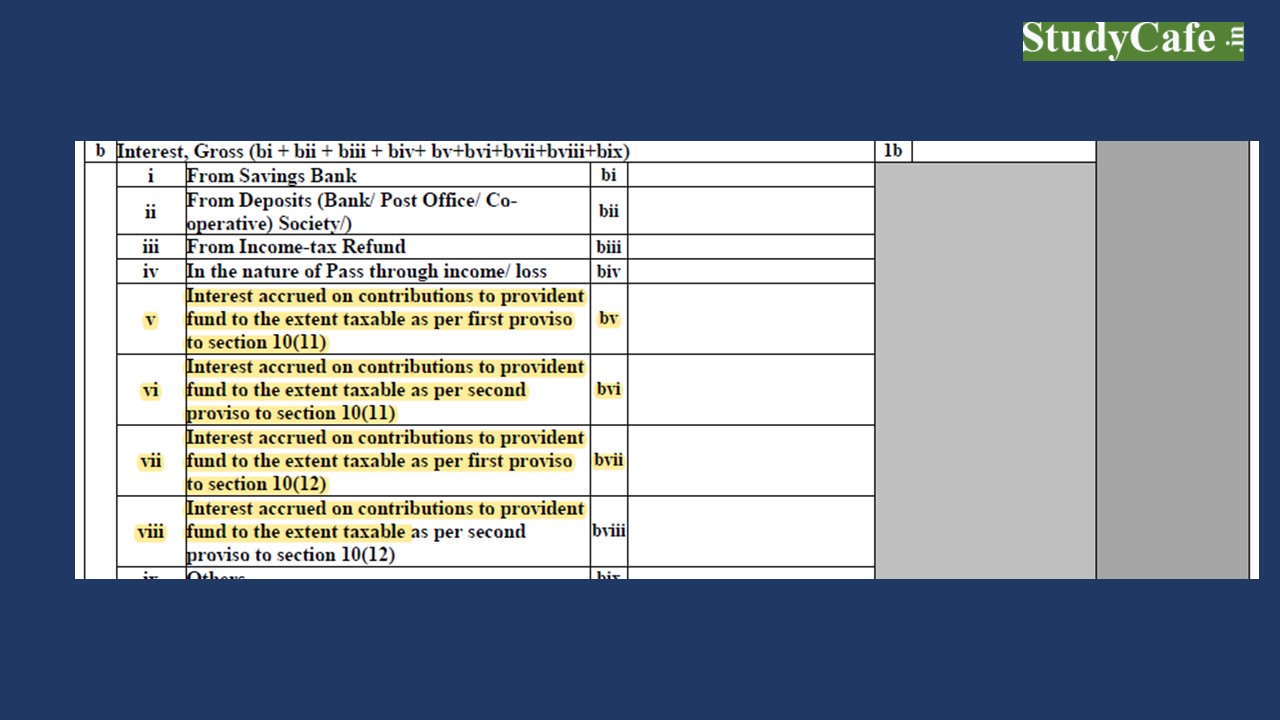

8) Disclosure for Taxation of Interest accrued on (PF) Provident Fund to which no exemption is available

[ITR 2 & 3]

8) Disclosure for Taxation of Interest accrued on (PF) Provident Fund to which no exemption is available

[ITR 2 & 3]

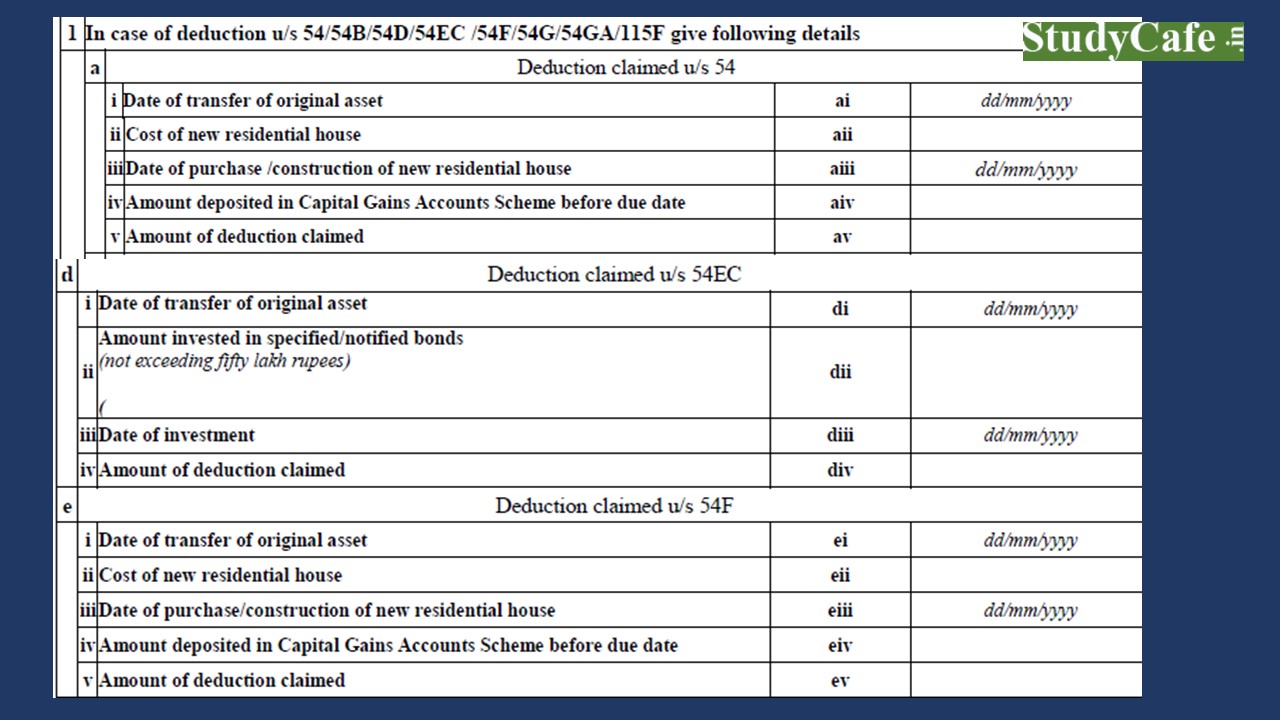

9) Additional Disclosure in Capital Gain Schedule

[ITR 2, 3, 5 & 6]

9) Additional Disclosure in Capital Gain Schedule

[ITR 2, 3, 5 & 6]

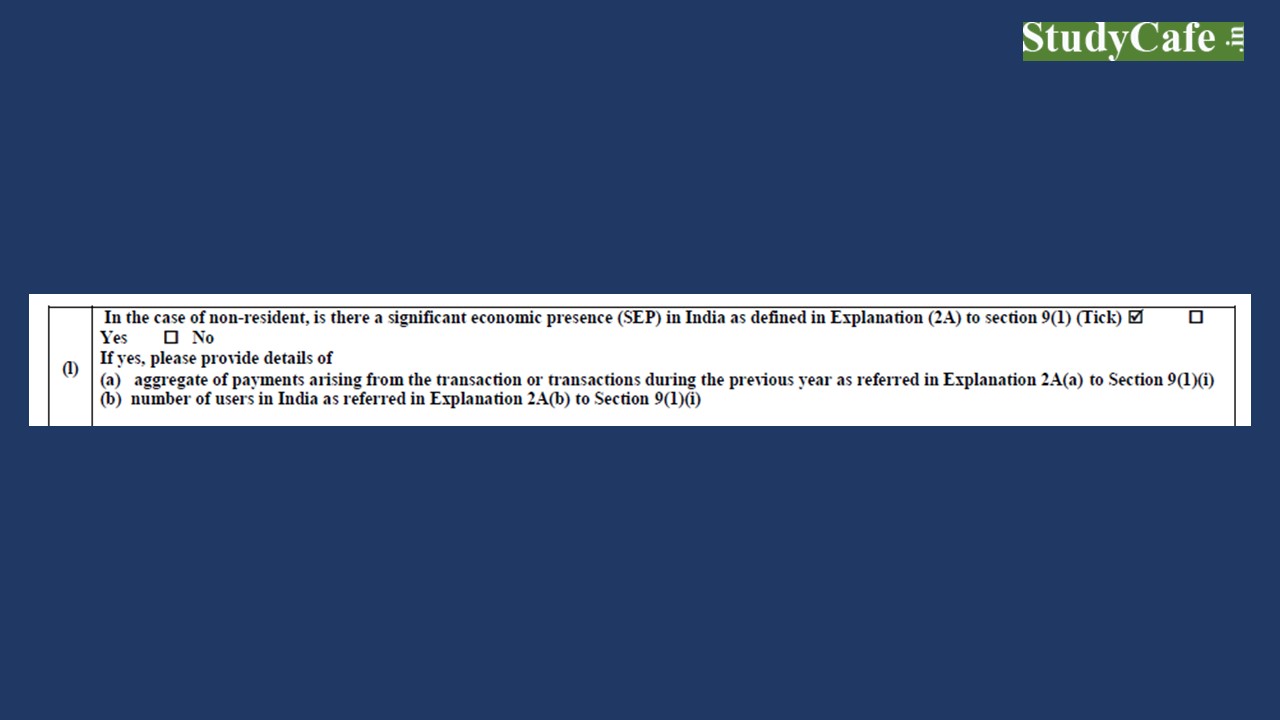

10) Disclosure related to Significant Economic Presence

In the new ITR forms, the non-resident has to confirm if there is a Significant Economic Presence (SEP) in India or not.

10) Disclosure related to Significant Economic Presence

In the new ITR forms, the non-resident has to confirm if there is a Significant Economic Presence (SEP) in India or not.

- In ITR-6 disclosure in respect of the alternative tax regime of Section 115BA/115BAA/115BAB is required.

- In ITR-5 disclosure in respect of the alternative tax regime of Section 115BAD is required.

- In ITR-3 & ITR-4 disclosure in respect of the alternative tax regime of Section 115BAC is required.

2. Pensioners need to disclose their income is from Central Government, State Government, Public Sector Units (PSU), or others

[ITR 1, 2, 3 & 4]

- In the Old Income Tax Return (ITR) Form, the only disclosure was if you are a pensioner or not.

- Now you need to specify if you get the Pension from Central Govt, State Govt, PSU or other

3. Additional Information is required for Businesses not opting for Presumptive Taxation

[ITR 3, 5, & 6]

Taxpayer not opting for Presumptive Taxation has to disclose the receipt and payment in cash. Now they have to disclose Payment received from a Non-account payee cheque or Demand Draft.

This amendment is related to Finance Act 2021. Watch this video for more clarification: REDUCTION IN TAX AUDIT LIMIT TO 1 CR FROM 10 CR?

4. Resident Status in India: suitable description of different clauses

[ITR 2 & 3]

Changes have been made in ITR clause related to the Residential Status of Individual so that the status can be correctly determined.

5. Dividend Income taxable as per section 2(22)(e) to be reported separately

[ITR 2, 3, 5 & 6]

Deemed Dividend Income as per Section 2(22)(e) is now required to be reported separately. Upto Last year there was no such specific disclosure. Deemed Dividend Income is Taxable in head other sources.

6) Dividend Income to be disclosed in Income from Other Source and not in Schedule BP.

[ITR 3, 5 & 6]

Dividends Included in Exclusion List of Schedule Business & Profession.

7) Deffered Tax on ESOP Schedule updated

[ITR 2 & 3]

- ESOP Information related to Tax-deferred is required to be reported.

- This is relatable to income on perquisites referred in section 17(2)(vi) received from the employer, being an eligible start-up referred to in section 80-IAC

8) Disclosure for Taxation of Interest accrued on (PF) Provident Fund to which no exemption is available

[ITR 2 & 3]

- Sections 10(11) and 10(12) have been amended by Finance Act 2021 so as to provide that No interest Exemption is available on Employee contributions to PF Fund exceeding two lakh and fifty thousand rupees.

- In case there is no Employer contribution the Limit is five lakh rupees.

9) Additional Disclosure in Capital Gain Schedule

[ITR 2, 3, 5 & 6]

- If you are selling any property in Foreign Country, you need to mention the Country and Pin Code in ITR forms

- If you are buying the property, you need to mention the date of transactions so as to avail the benefit of deduction in Section 54, 54EC & 54F.

- The taxpayer is required to give year-wise Cost of improvement, Year of improvement; and Cost of improvement with indexation.

- Separate disclosure of capital gains on transfer of asset of partnership firm in case of dissolution

10) Disclosure related to Significant Economic Presence

In the new ITR forms, the non-resident has to confirm if there is a Significant Economic Presence (SEP) in India or not.

About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts